-

Overview

2023 was all about the “Magnificent 7” (Mag7) group of mega cap stocks; Apple, Microsoft, Alphabet, Amazon, Nvidia, Meta and Tesla. With a weight in the S&P500 index of 29% (a level of concentration not seen since the 1970s), they accounted for two-thirds of the S&P 500’s total annual return.

Can the Mag7 remain Mag?

As we said in our introduction, anything is possible. These stocks, however, are not immune to the business cycle. Lest we forget the halving of the Nvidia share price in 2022.

Long-term, active investors need to look beyond these seven stocks. A soft-landing scenario should see international equities perform reasonably well – particularly in the absence of any exogenous or black swan event.

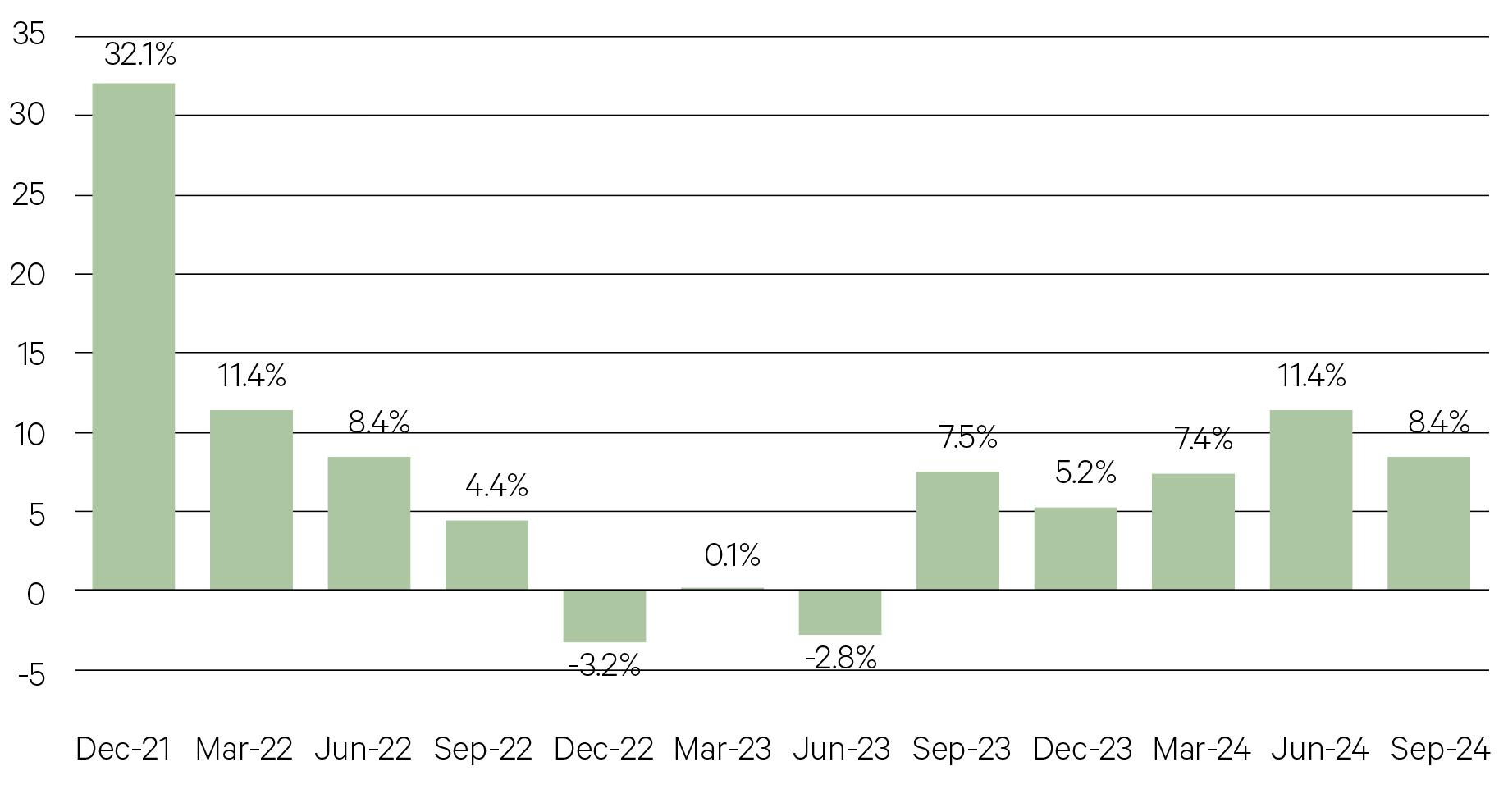

S&P500 earnings growth

Source: Reuters

—

10% – The share of humanity that will be 65 or older in 2024.

United Nations World Population Prospects

—

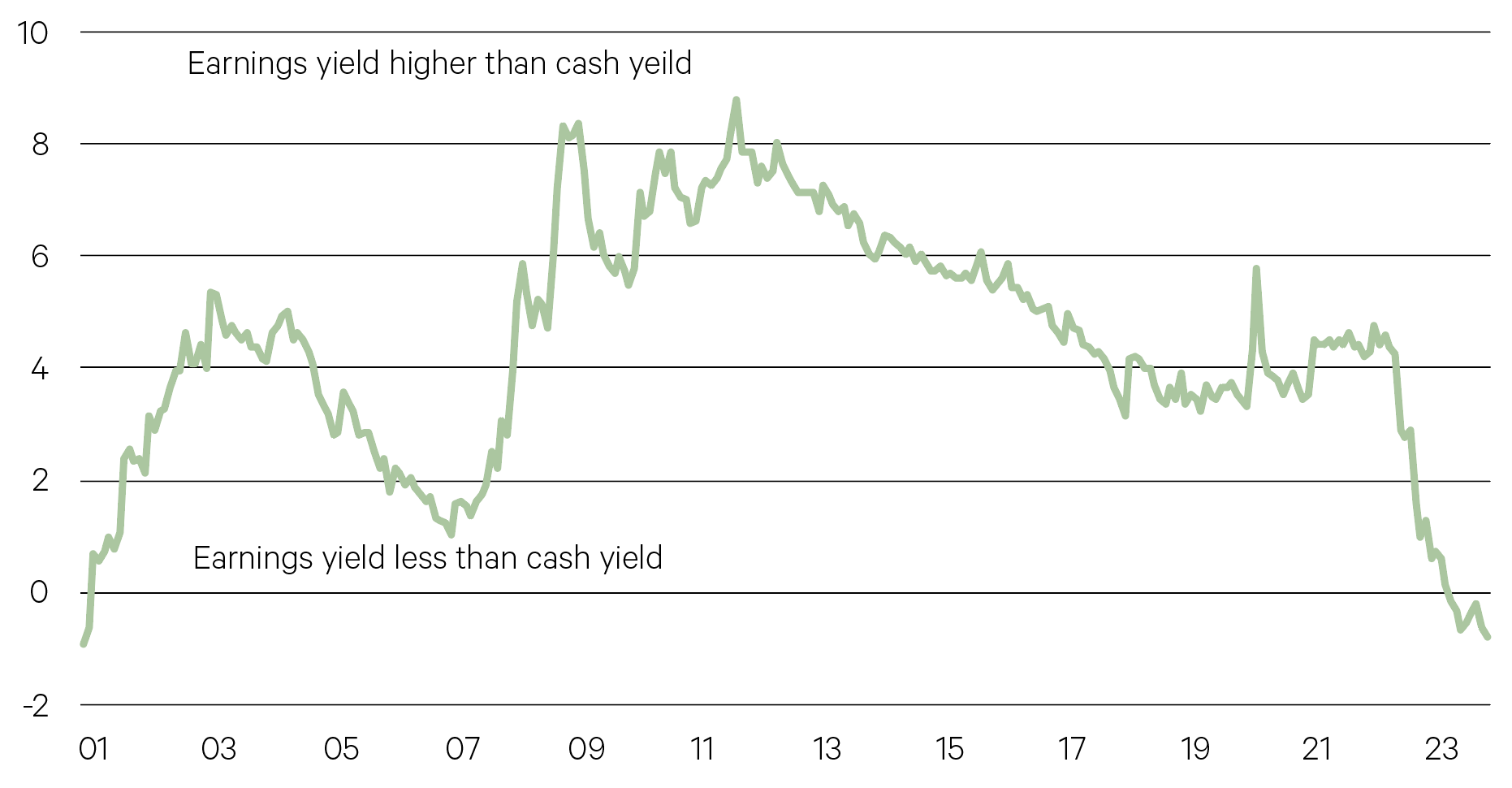

Some caution is warranted, however. Higher bond yields start to bring corporate debt levels into focus. This is especially important for those companies that either didn’t term out their debt when rates were low or have debt coming due in the next year. Historically, there is about an 18-month lag between a move in bond yields and companies’ effective interest rates.

Higher rates are also important for market valuations, like price/earnings (P/E) ratios. This is the price investors are willing to pay for a dollar of earnings – it is the inverse of the earnings yield (E/P). Periods of higher inflation and interest rates tend to coincide with lower P/Es, or higher earnings yields. This makes sense since the earnings yield for equities is the sum of the cash yield plus a premium for taking equity risk.

—

The current PE for the US equity market is around 25, implying a 4% earnings yield. With a 5% cash yield currently, the market is implying a negative premium for taking equity risk. No wonder money market funds continue to attract investment flows! For equity prices to move higher from here, a positive premium for taking equity risk needs to be built in. This means a lower PE (higher earnings yield) – achieved either through lower equity prices or higher earnings.

The yield from cash now exceed that of equities (S&P500 earnings yield less the 3 month Treasury bill rate (%))

Source: Bloomberg, data as at 31/12/23

—

US$100trn – The size of the world economy in 2022.

IMF

—

Overall, the equity market can still produce a positive return this year but the heavy lifting will need to come from earnings. That outcome could be met if the consensus is correct in expecting double-digit earnings growth – a significant improvement relative to 2023. Some skepticism is warranted here in a slowing nominal growth environment.

We expect the market will oscillate between expecting a recession and expecting a soft landing. This will create volatility just as it did in 2023 when bond yields moved in a wide range.

More specifically, 2024 will be less about AI’s “creators” and more about its “adopters” – across the spectrum of industries and sectors – as companies increasingly focus their capital spending on productivity-enhancing investments. Health care innovation is another area that could also offer opportunities, as could the energy sector, thanks to capital investment in both traditional and renewable energy sources.

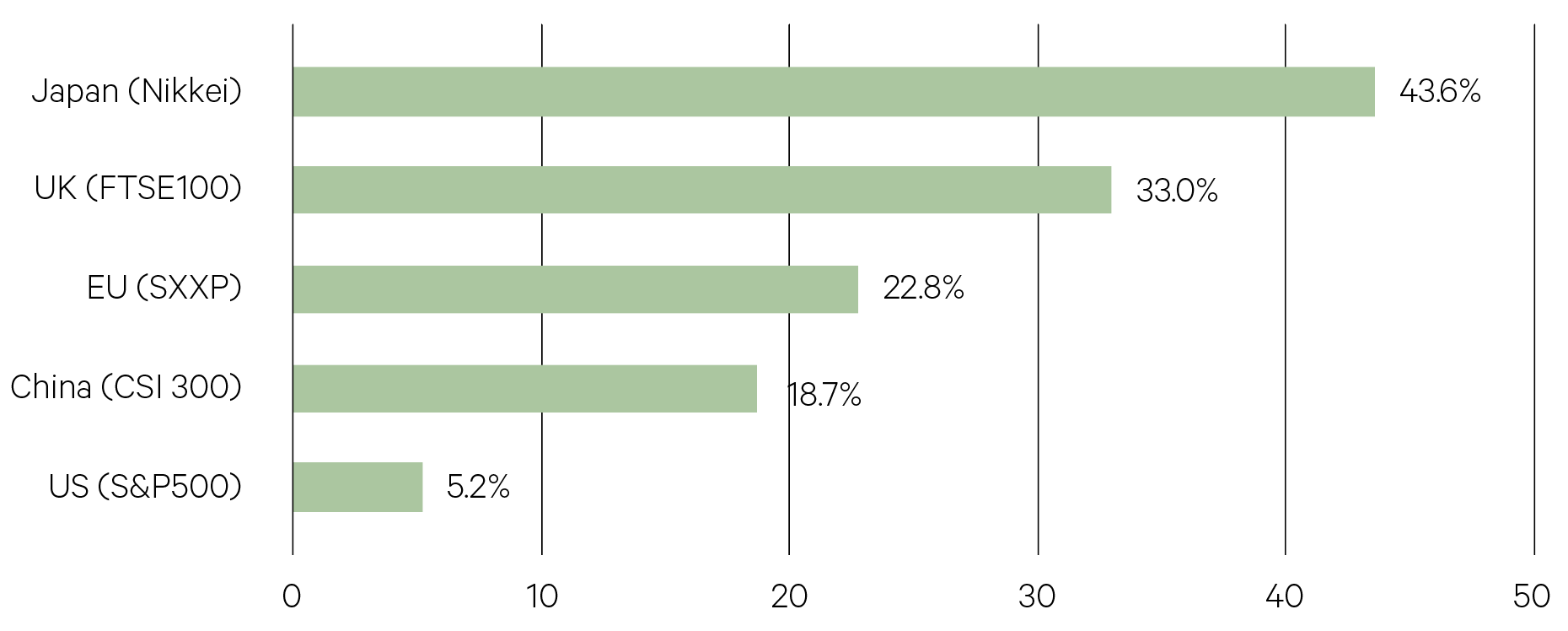

Overall, U.S. equities are likely to have better outcomes than European equities. Japanese equities are also expected to do well. Our focus for emerging markets is outside of China where we see opportunities in markets like India.

UK and Japan have the cheapest equity markets (% cos trading below book value)

Source: Bloomberg

—

80% – The percentage of firms that plan to increase their investment in AI by over 50% in 2024.

KPMG