-

Overview

Globalisation was a key driver of economic growth over several decades post World War II. This was accelerated at the turn of the century as China joined the World Trade Organisation and countries became more connected due to advancements in technology. A combination of more open capital markets, increased trade and less regulation and government intervention helped to underpin a period of prolonged economic expansion and low and more stable inflation. Emerging market (EM) economies have been significant beneficiaries, with global poverty reduced materially.

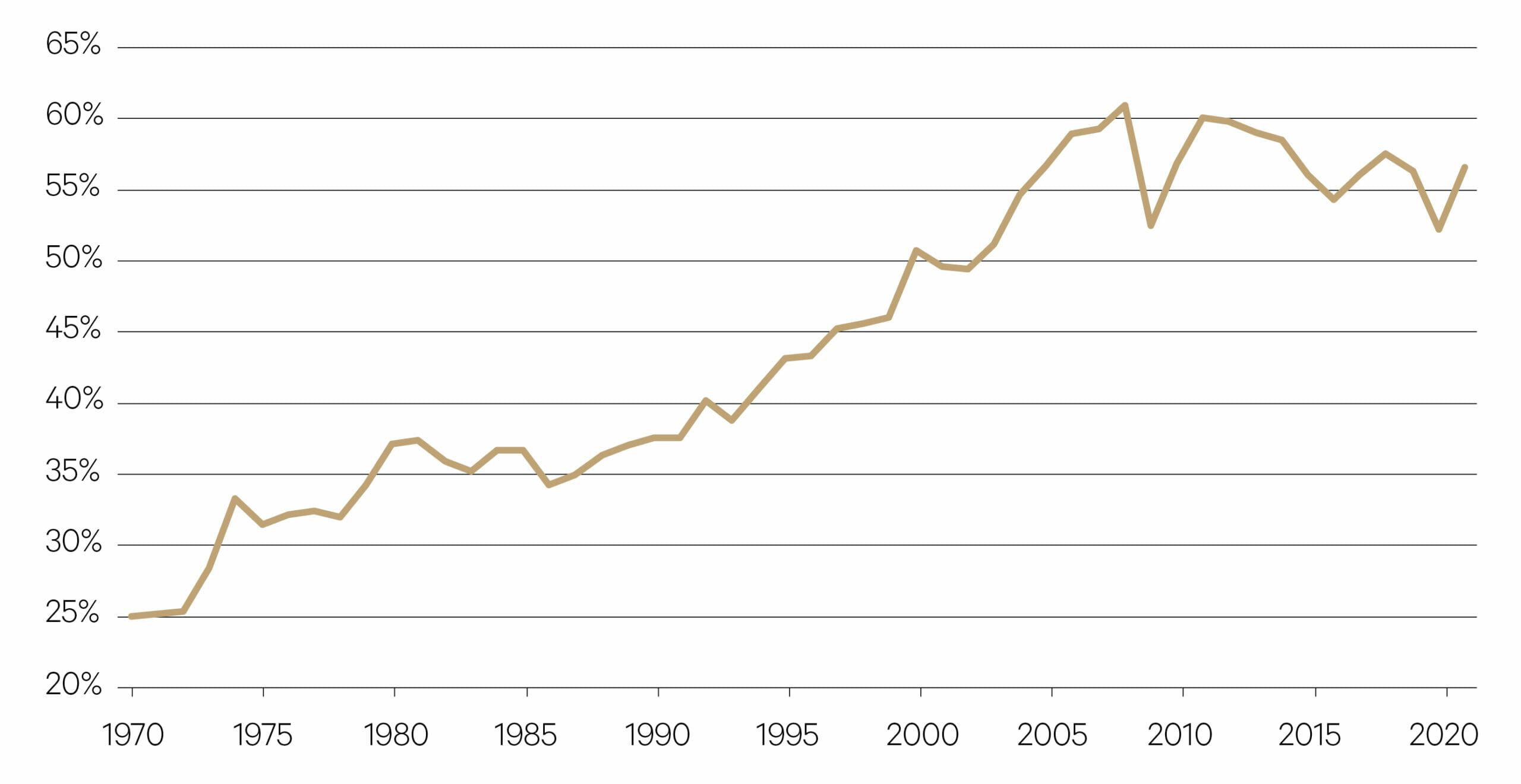

The wheel is slowly turning against this previously well-entrenched trend. Global trade as a percentage of GDP peaked at 61% just as the global financial crisis (GFC) of 2008 hit and has been on a gradual retreat since. There are several reasons for this.

Firstly, the rise of more populist politics due to rising inequality following the GFC has led to outcomes such as Brexit, instability across the European Union, and the election of leaders such as Donald Trump in the US. Countries have become more inward-looking and protectionist as a result.

As China has risen to become a global economic power, the trade conflict with the US has migrated into higher value-add industries, such as technology. While China’s growth has been transitioning from an export-led model to one more driven by consumption, the recent National Congress of the CCP also confirmed that maximising economic growth is falling in terms of the government’s priorities. Instead, security is key, including the aim to become more self-sufficient in areas in which it had previously relied on international markets, such as food, energy and technology.

Lastly, two specific events in the last two years have had a large impact on the likely evolution of trade over the next decade and more – the Ukraine war and the COVID crisis. In the last 12 months, the Ukraine war has heightened the importance of food and energy security for many countries, particularly across Europe. An acceleration of the green transition to domestic renewables and away from foreign energy sources is a likely outcome in the wake of the war.

The COVID crisis exposed many global supply chains, causing significant disruption to numerous industries. Lockdowns drastically slowed the flow of goods, COVID infections left many businesses short of staff, and a spike in spending on goods led to demand that was unable to be fulfilled by just-in time inventory management. The trade-off between minimising supply costs and optimising supply chain resilience and reliability had swung too far.

An emerging response for improved supply chain reliability is the reshoring or ‘nearshoring’ of manufacturing to countries that are closer geographically. In this fashion, trade would become less global and more regionalised. Adjacent countries to developed economies stand to benefit from this development, such as Mexico with the US.

—

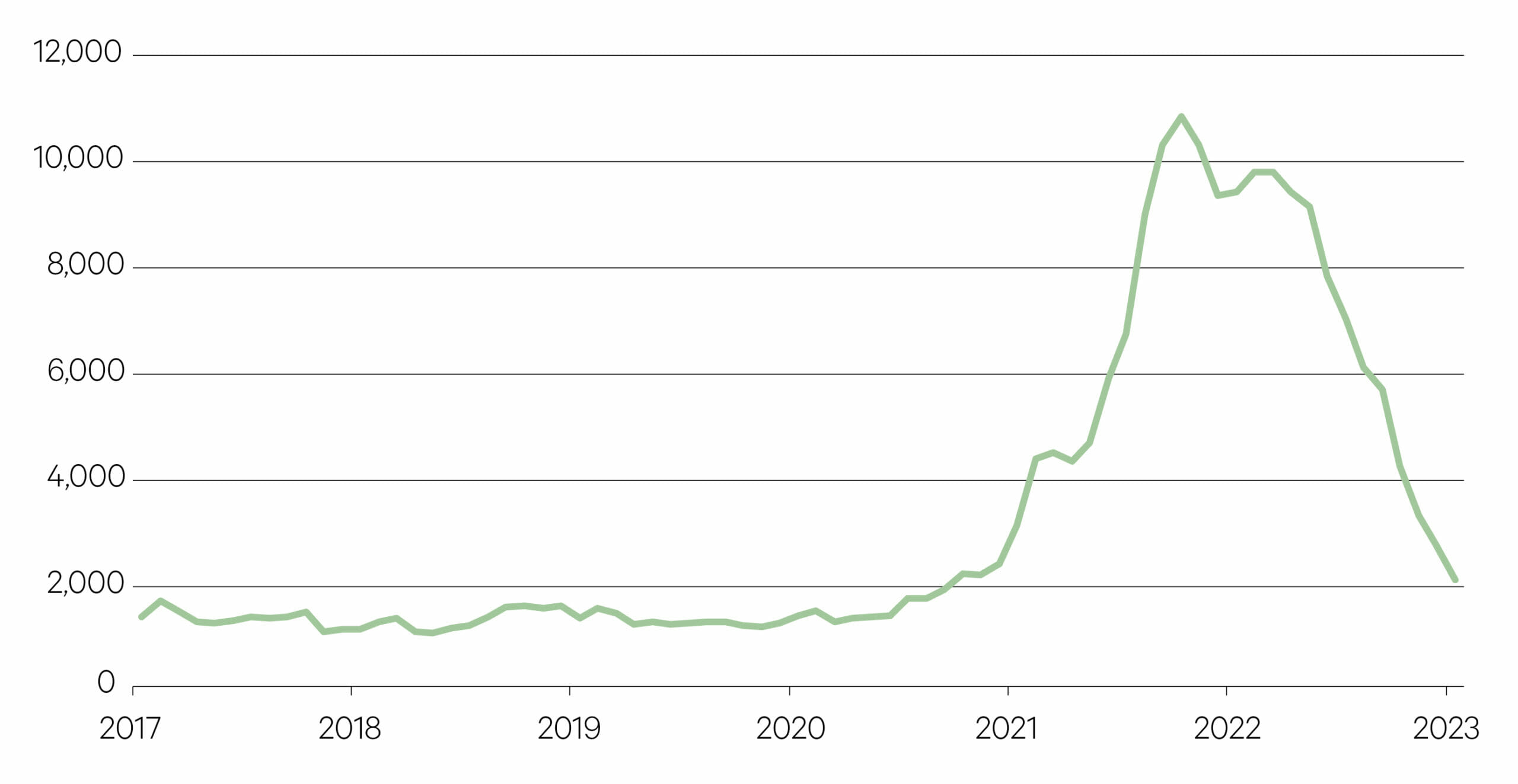

Global freight rates escalated through the COVID crisis, which has encouraged companies to either re-shore or near-shore their manufacturing base.

—

The investment implications of these developments

Deglobalisation inevitably leads to higher domestic production of goods, reduced profit margins for companies and higher competition for local employment, putting upward pressure on wages. In turn, this should result in higher inflation and hence higher central bank policy rates. Hence, the most important conclusion for investors is that globalisation can no longer be relied on as a permanent factor in helping to keep inflation (and consequently interest rates) low.

A second key takeaway is that China is becoming less attractive for allocating capital within a portfolio. The combination of increased geopolitical and regulatory risk, and a normalisation of long-term economic growth rates as social goals rise in priority for the CCP, all amount to a challenging outlook over the next decade. With China accounting for nearly a third of EM equity indices, portfolios should hence be constructed with particular regard to this growing risk.

Global trade as a percentage of GDP peaked in 2008 and has trended slightly down ever since

Source: The World Bank

—

Freightos Baltic Index (global container freight index)

Source: Bloomberg, Freightos Data

—

Stagnant wage growth in Mexico compared with China now means that manufacturing labour costs are now much lower in Mexico, giving further incentive for US companies to relocate or diversify their manufacturing base to their neighbour.

Manufacturing labour costs per hour – China and Mexico ($US)

Source: OECD, Bank of America