-

The post-pan world

With the “event” that triggered the global recession now in the process of being addressed, it is time to think about the future. What does the world look like in the post-pan environment?

1. Re-opening

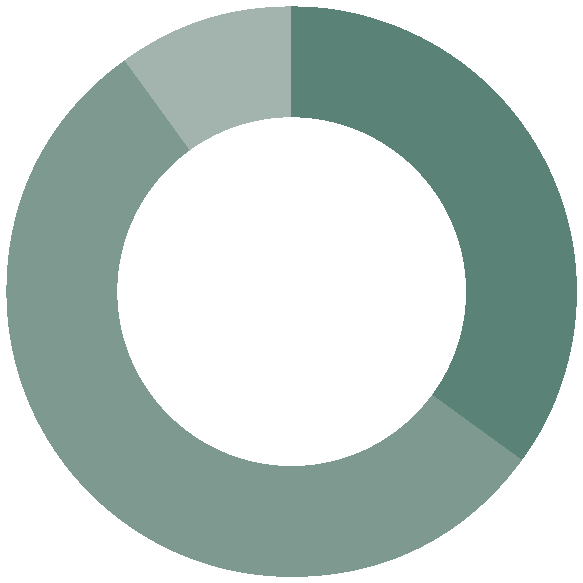

The biggest vaccination campaign in history is well underway – outside of Australia anyway. So far, more than 797 million doses have been administered across 154 countries at a rate of 18.0 million doses per day. A total of seven vaccines are now available for public use. Israel continues to lead the way in terms of the percentage of the population that has received at least one dose.

In the U.S., the latest vaccination rate is 3.1m doses per day. That number keeps rising. At this pace, it will take another 3 months to cover 75% of the population. This compares with 4 months for the UK, 7 months for France and 10 months for Germany. Given this, we would expect to see economies begin to fully open up by the third quarter of this year.

Chart 1: Percentage of the population received 1+ vaccine dose

Source: Bloomberg

2. Reflation

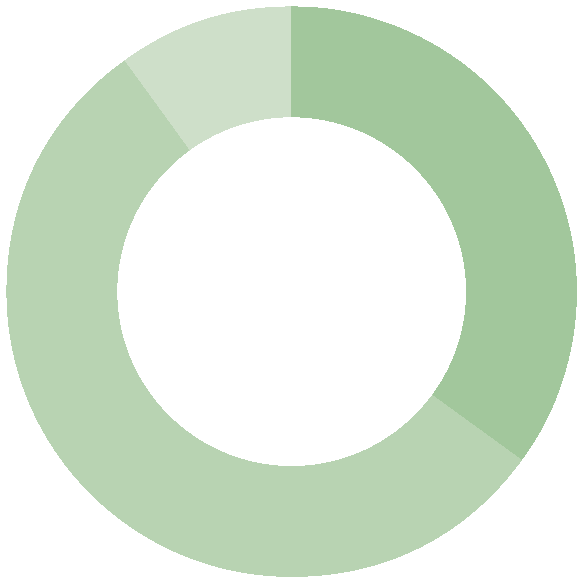

Reopening means the pent-up demand that has been so well supported by record fiscal and monetary stimulus can start to be released. The recession appears to be behind us in most countries, and the early stages of an economic expansion are taking shape. Some of that pent-up demand is already being spent on goods. We expect this spending to rotate into services as more restrictions are eased. Whilst household saving rates have declined, they are still very elevated suggesting consumers have room to continue to spend.

Chart 2: Household savings rates (% income)

Source: Bloomberg

3. Inflation

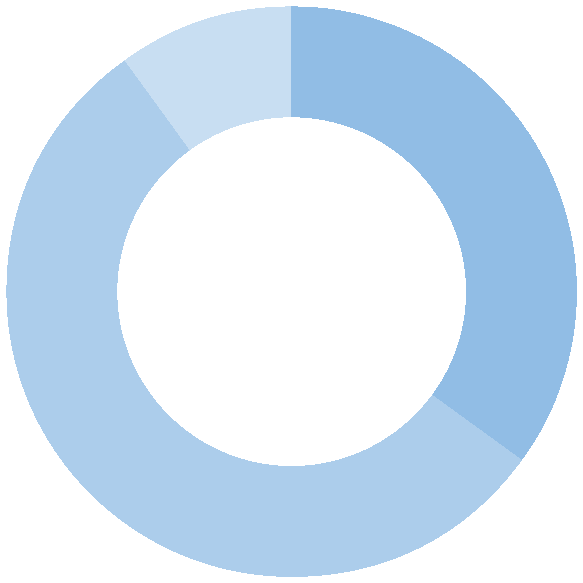

The reflation trade is powering assets tied to economic growth, including commodities. This is leading to expectations of higher inflation. Not withstanding a temporary spike in inflation driven by weak annual comparisons to a year ago, we expect inflation will remain reasonably contained. Whilst the global economy is, albeit very quickly, returning to the pre-pandemic world, there are a number of key differences to be mindful of. First, government debt levels are so much higher today than pre-pan. Second, the pace of technological innovation is greater. And third, millennials now outnumber the baby boomer generation (this occurred in 2019). In our view, this points to the same outcome but for different reasons – lower for longer. High productivity growth will keep inflation check and will allow fiscal policy to be tightened ensuring growth is capped but still very high debt levels means interest rates will need to remain low for some time.

Chart 3: A snapback in growth is not a trend – GDP growth (yoy%)

Source: Bloomberg

-

Australian Equities

– The Australian equity market generated a positive performance in each of the first three months of 2021, continuing its recovery that is now 12 months on from the height of the COVID crisis.

– The highlight of the quarter was the strongest domestic earnings season in several years, with companies beating profit expectations by a large margin and dividends also surprising to the upside. The cyclical recovery in earnings in recent months has been driven by two key sectors in particular – financials and resources.

– Commodity prices were broadly stronger again, with oil and base metals prices firmer. The iron ore price remained steady, though at an elevated level, ensuring robust cash generation for the big iron ore miners.

– The macro environment provided a mixed backdrop for the market. Domestic economic data was positive through the quarter and there were limited new COVID cases reported in Australia. However, Australia’s delays with the vaccine rollout was negative for sentiment, while a steepening yield curve provided a headwind to the valuation for growth and defensive sectors of the market.

– This latter factor was again a key determinant in the relative performance of our Australian equity strategies. Among large caps, Pendal and Martin Currie produced the best returns, with both tilted towards the more cyclical sectors of the market.

– Meanwhile, more growth-orientated strategies, particularly Selector, struggled in the face of higher bond yields. Bennelong Concentrated delivered a respectable return given this environment.

– Small caps underperformed large caps by 2.2% over the quarter, however, the small cap benchmark has still generated much stronger performance on a rolling year basis, as is often the case in the early stages of a market recovery.

– Most of our small cap managers generated solid outperformance of the benchmark over the quarter, with the standouts being Ophir, Spheria and Fairview, while Karara was the only fund to underperform.

-

International Equities

– Global equities were up 4.5% in the March quarter after recording a robust 13.6% in the final quarter of 2020.

– Breaking its two-quarter winning streak, emerging markets underperformed developed markets with the former rising by 1.9% over the first three months of the year. The outperformance was driven by solid gains in a number of European markets including Sweden (+17.0%), Italy (+10.9%) and Germany (+9.4%).

– For the second consecutive quarter value outperformed growth. The Russell 2000 Growth Index rose 1.9% while the Russell 2000 Value Index jumped 10.1%. It is no surprise then that the US market underperformed its major developed market peers rising just 5.8%.

– The outperformance of European equity markets was not reflected in the currency. The euro fell by 4.0% against the US dollar. The Australian dollar was weaker against the greenback (-1.2%) but stronger against the euro (+2.8%). This meant unhedged equity funds with a greater allocation to the US outperformed their hedged equivalent. Such was the case with Magellan. Those with a greater allocation to Europe saw the hedged returns outperform. Such was the case with Atlas Infrastructure.

– Pleasingly, most of our international equity managers generated positive returns in the quarter.

– In general, our large cap funds outperformed our small cap managers and our developed market funds outperformed our emerging market funds.

– The best performing fund was the Fidelity Asia fund which added 10.3% over the quarter. Much of this return came from a strong month of January where the funds’ holding in Taiwan Semiconductors rose by 11.6%. Over the whole quarter the stock was up 8.5%.

– Another significant holding in the Fidelity Asia Fund was Hangzhou Hikvision Digital Technology, a manufacturer and supplier of video surveillance equipment. It was up 17.7% over the quarter. The state-owned company is expected to benefit from China’s 83 smart city projects under construction focusing on transport and security system upgrades. The company’s market share has increased due to expansion into smart home applications and cloud computing services. Hikvision’s China sales are more than double those of Dahua, its closest competitor. It had more than 36% of the global video surveillance market last year. Fidelity sold into the strength in the quarter and since the company was listed on the US sanctions list will need to exit the name completely by November this year.

-

Fixed Income

– Positive news on the vaccine front and better-than-expected economic data saw bond yields in general rise in the quarter. This was particularly the case for Australia and US 10-year yields which rose by 82 and 83 basis points respectively. This move up in yield capped the performance of government bond funds such as the Legg Mason Western Asset Bond Fund.

– Credit-oriented funds performed better as credit spreads continued to retrace lower although investment grade credit was particularly affected by the rise in long term bond yields. Bentham with its large allocation to bank loans and high yield was again a standout in this regard.

– The allocation to investment grade credit was the largest contributor to negative performance for Macquarie. Investment grade credit spreads narrowed over the quarter but bond yields rose.

– Our low risk liquidity managers Ardea and Realm performed as expected with Ardea adding 0.6% net while the Realm Short-Term Income Fund added 0.8%. Positive fund flows continue into this Realm fund with its size now sitting at $183m. The Realm High Income Fund added 0.3% over the quarter.

– The PIMCO Global Bond Fund was impacted by the rise in bond yields while the Global Credit Fund was impacted by its 92% allocation to investment grade credit which recorded a negative 4.3% return over the quarter.

-

Alternatives

– The first quarter of 2021 proved to be volatile for hedge funds globally as retail induced short squeezes and substantial deleveraging events left some hedge fund managers with significant losses. Short selling was particularly tough in Q1, an index tracking the 50 most shorted stocks in the Russell 3000 rose by 34% over the quarter. Sharp factor rotations also detracted for many as growth, momentum and quality all underperformed whilst cyclicals and value outperformed.

– Market neutral hedge fund Bennelong Long Short was the worst affected by this rotation as the funds bias for long positions in quality companies with low leverage and adjacent short positions in companies with high balance sheet leverage and greater cyclical exposure hurt as the catch up trade in some of the most beaten down names in the ASX 200 accelerated during the quarter.

– Long only hedge fund Platinum Unhedged continued to benefit from this rotation as the fund added 11.3% for the quarter bringing its 6 month performance to 29%. Attribution came from overweight positions in financials and materials.

– Private equity fund raising and deal flow continued its recent strong momentum from Q4 ’20 into 2021 as total deal value exceeded $200bn in the US for the first quarter, up 21% on the same period a year ago according to Pitchbook data. The rise in special purpose acquisition companies (SPAC) further accelerated as over $90bn has been raised by SPACs in Q1 ’21 already surpassing the $77bn raised throughout 2020. SPACs have become a viable exit route for PE managers looking to take advantage of high market valuations and faster deal execution.

– Our private equity managers posted positive returns for the three month period ending February ’21 as Partners Group (+2.4%) and Hamilton Lane (+2.2%) both gained from direct equity and secondaries positions in the healthcare and technology industries.

– Emerging companies fund Alium Alpha benefitted from a listing in the quarter for Banxa, a Canadian based payments service provider operating in the digital assets space, which listed in early January and finished the quarter up 188% from its listing price. Positive attribution also came from private company AcademyXi after the company completed a follow on round of funding at an uplift to previous valuations.

– In direct property, the Barwon Healthcare Property Fund added 1.7% for the quarter with rolling 12 month returns sitting at 10.7%. The fund continues to benefit from its exposure to high quality tenants with long term leases in the defensive healthcare property sector. Capitalisation rates continue to tighten in the sector acting as a tailwind for valuations.

– In the private debt space, Merricks Partners Fund added 2% for the first quarter as loans in the residential, industrial and office space were fully repaid during the quarter. Additional funds were deployed in the office and agriculture industries during the quarter. Agriculture continues to see strong tailwinds from high production levels and elevated commodity prices.