-

Overview

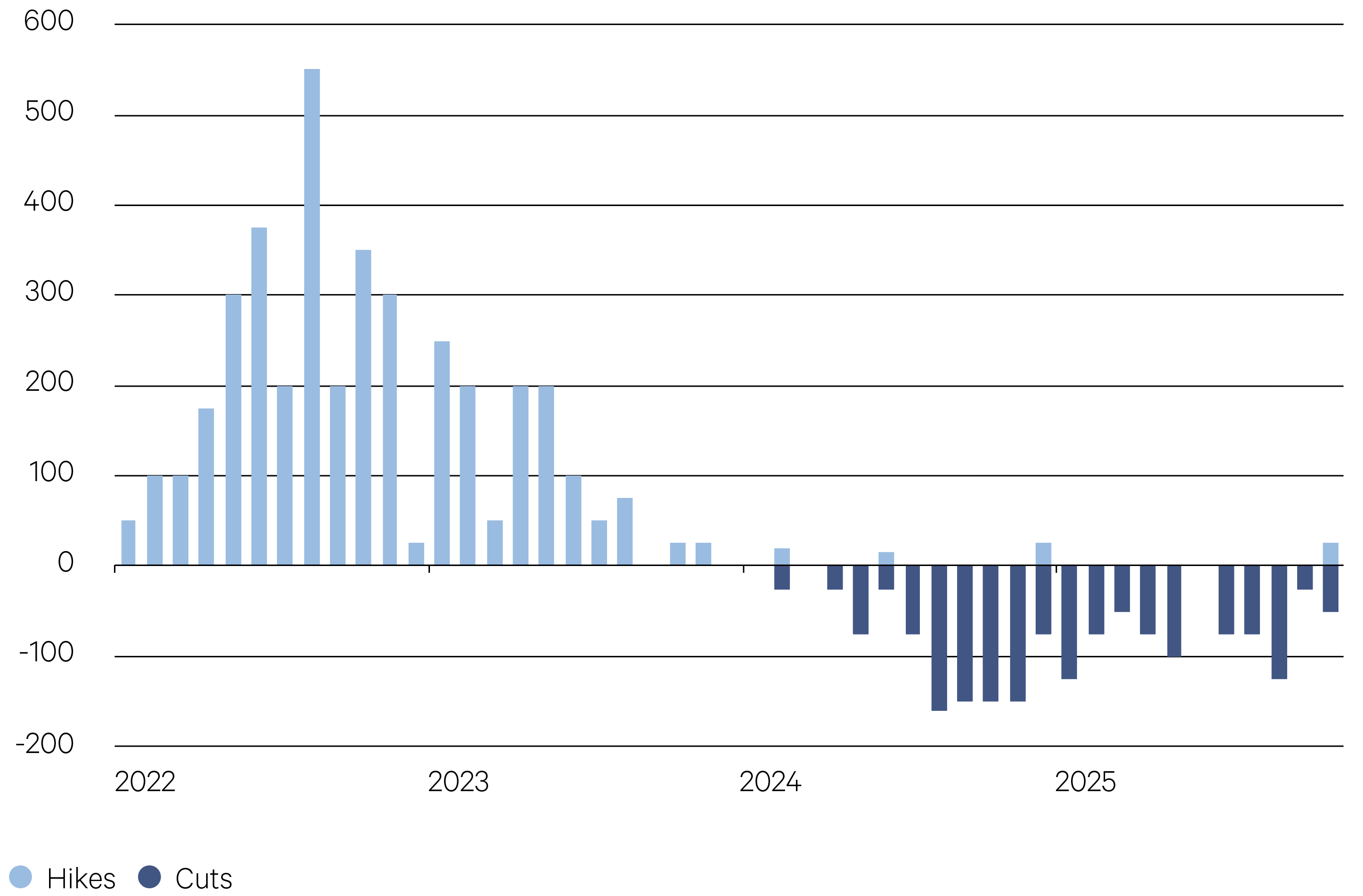

Fixed income in 2025 was characterised by shifting expectations. Liberation Day tariffs sparked volatility, with investors anticipating higher U.S. inflation and weaker global trade. Global rate cutting continued at the fastest pace and scale since the GFC, with 850bps of easing across the G10 in 2025. Weak U.S. labour markets forced the Fed to cut more aggressively despite above-target inflation. President Trump applied pressure to the Fed and chair Powell to lower rates. Powell’s term as chair ends in May amid concerns over political influence on his successor. However, with 12 voting members and little scope for the President to replace members, these concerns are relatively unfounded.

G10 hikes and cuts since 2022 (bps)

Source: Bloomberg

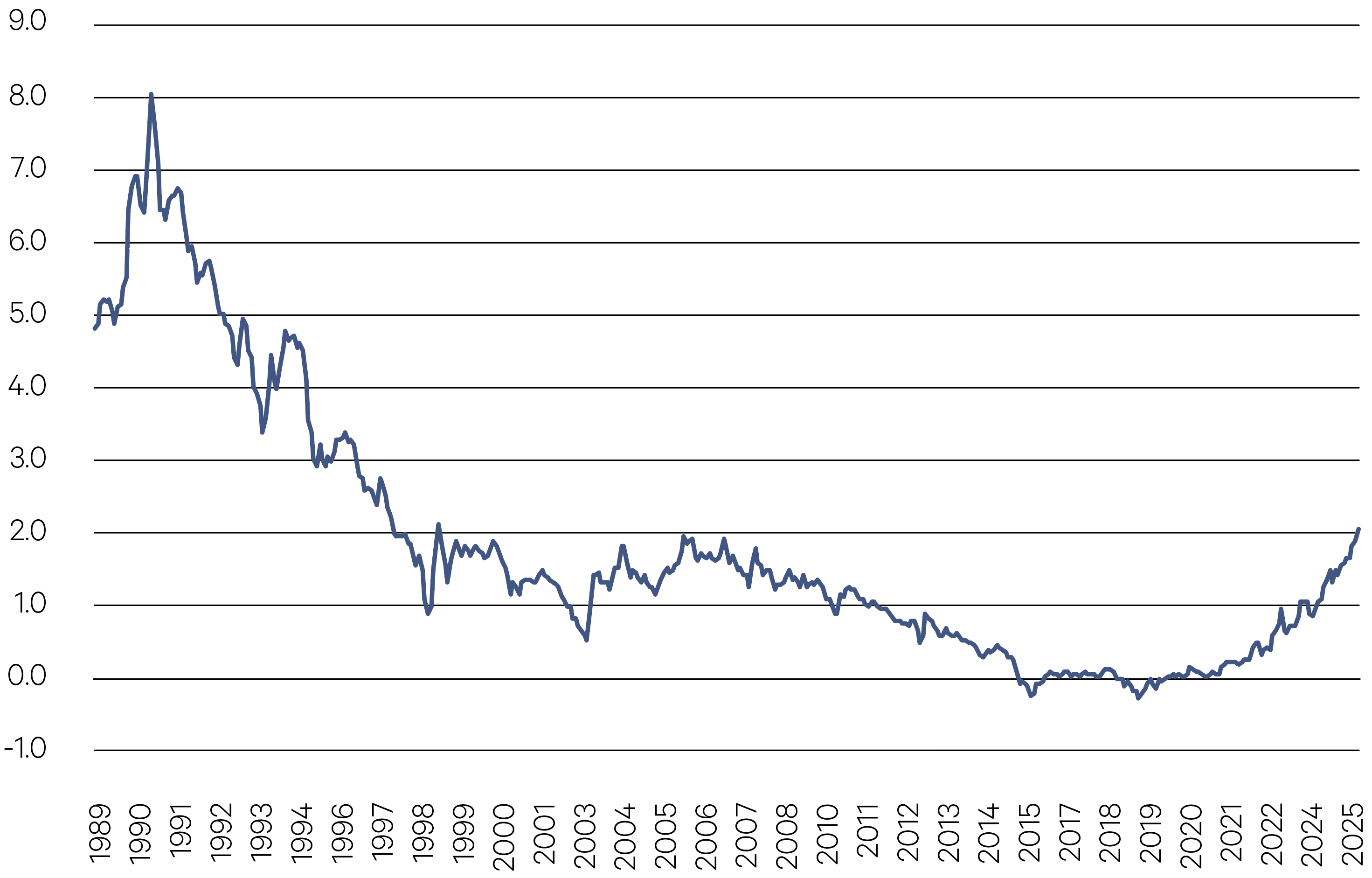

The Bank of Japan, however, is more politically influenced. In December, the BOJ lifted rates to 0.75%, a 30–year high, to curb persistent inflation. The announcement by Japan’s new Prime Minister of fiscal stimulus funded by new bonds pushed 10–year yields above 2%, the highest since 1999. Rising Japanese yields threaten the carry trade, where investors borrow at low rates in Japan and invest in higher yielding securities, potentially triggering U.S. capital outflows.

Yield on 10yr Japanese Government Bonds (%)

Source: Bloomberg

—

2.1% – the peak of 10yr Japanese bonds in 2025, the highest since 1999

Source: Bloomberg

—

Australia’s cutting cycle likely ended at 3.6% amid persistent inflation and low unemployment, with hikes priced for early 2026. New Zealand, Canada, and Europe may follow, though falling oil prices could promote disinflation and delay moves.

Europe faced sluggish growth prospects, allowing the European Central Bank (ECB) to cut rates to 2%. Political uncertainty drove French yields higher as the nation appointed its fifth Prime Minister in two years. The UK narrowly avoided a repeat of the 2022 bond crisis; however new and incoming taxes are weighing on already weak growth.

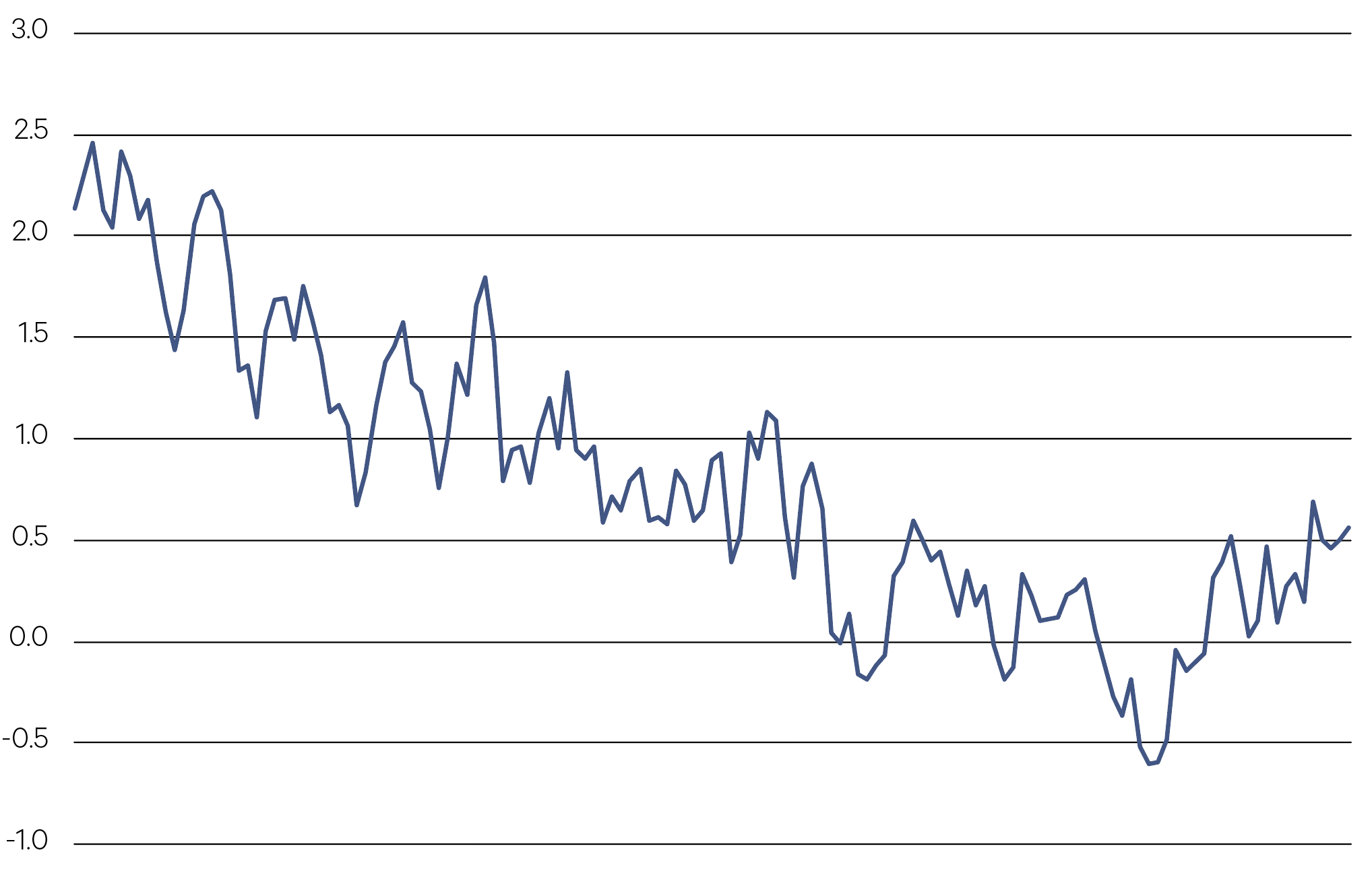

Term premia, the reward for holding longer dated bonds, has risen after decades near zero, steepening the long end of the yield curve as fiscal deficits grow and investors price in the risk of higher sovereign debts. Fiscal responsibility was a key discussion in 2025 amid the passing of the U.S.’s One Big Beautiful Bill Act. The act is forecast to cost over US$4 trillion in the next decade, as well as almost double the nation’s debt to GDP ratio to 190% by 2054.

Credit spreads tightened despite brief periods of volatility. Australian credit offers better risk–adjusted value compared to the U.S. and Europe, though the prospect of higher yields in 2026 could attract further capital and compress spreads. Increased local and offshore issuance into the domestic market has helped absorb recent demand for AUD denominated debt.

U.S. auto–lending insolvencies briefly spiked volatility and spread widening but proved idiosyncratic. Defaults stayed low, though increased downgrades and rising arrears in some U.S. consumer credits signal mild stress. Limited 2026 high-yield maturities eases refinancing risk for lower quality borrowers.

Term premium on a 10yr zero coupon bond (%)

Source: Bloomberg

Despite no major risks on the horizon for 2026, high valuations and low risk premia skew risk to the downside. We continue to recommend shorter-dated, high–quality investments, with opportunistic addition of rewarded risk, to capture higher yields while minimising downside risk.

—

US$4tr – estimated 10yr cost of OBBBA

Source: CBO

—