-

Q1 in review –

Fire Starter

In our annual publication, “Agenda 2026”, the argument was made that Trump is not the root cause of the pressures now surfacing across the global economy. Those forces have been building for decades in the aftermath of the Global Financial Crisis. He has, however, acted as an accelerant. And, like a child playing with matches, the situation now appears to have moved beyond his control – hence the turn to the very allies he denigrated only weeks ago.

Why should long-term investors care?

In truth, they shouldn’t – at least not about the daily stream of fiction coming out of Truth Social. What matters is what this episode reveals about the world we are now in – one that is more inflationary, more prone to bouts of event risk, and more national in orientation.

For disciplined investors, while the environment is more challenging, it is also richer. Dispersion across markets remains elevated by historical standards, creating more opportunities for diversification. While US companies continue to deliver double-digit earnings growth, technology stocks are now trading at their most attractive valuations in more than 7 years, relative to the broader US market.

1. More Inflationary

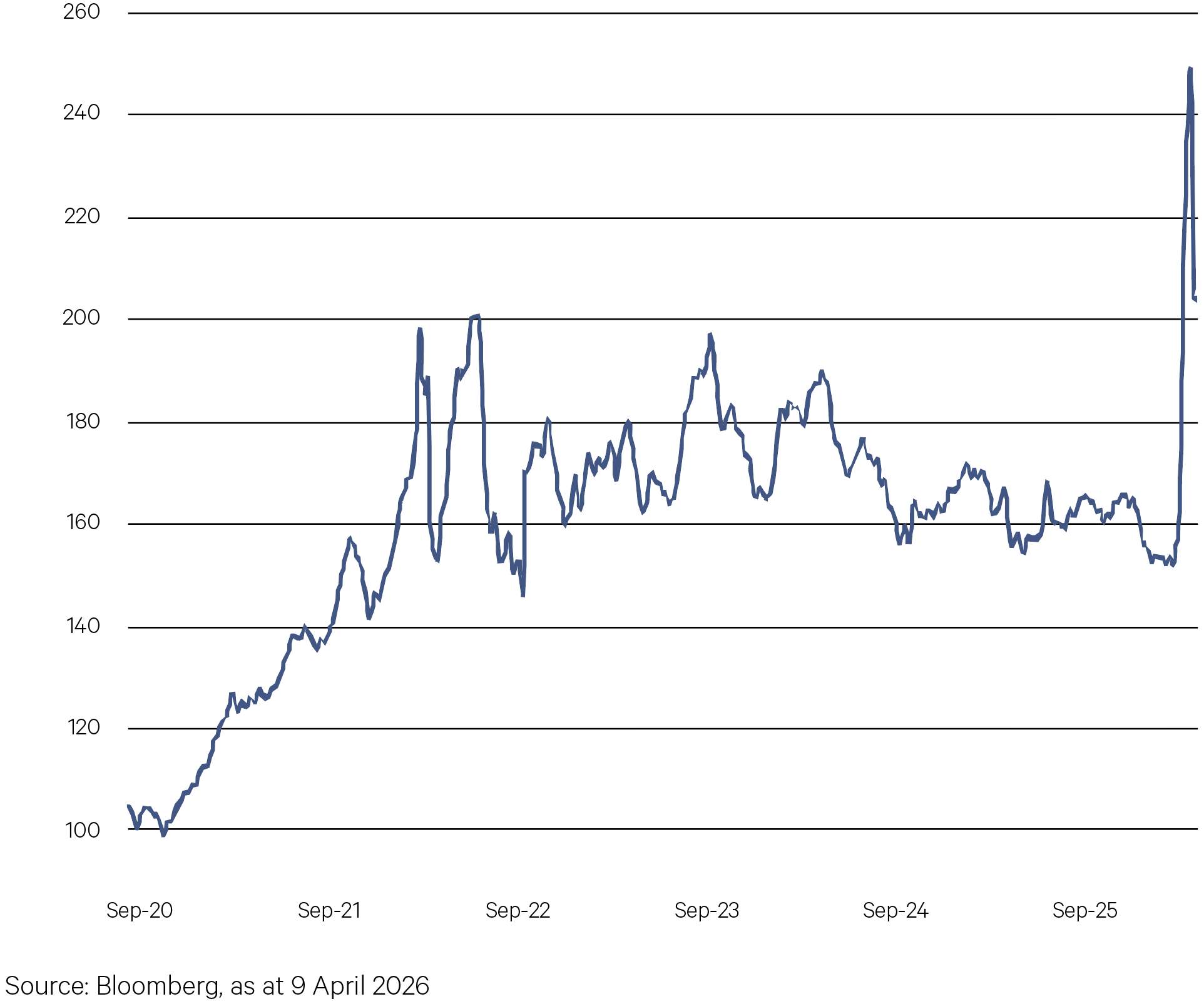

Like the pandemic, the war in Iran is an example of how exposed critical supply chains are in this new, more fragmented world order. And, just as the pandemic led to a rewiring of supply chains (onshoring, reshoring, near-shoring), the war in Iran is forcing a structural rerouting of oil flows. Efficiency is being substituted for resiliency. This means more tanker miles, longer transits, and higher insurance and freight costs. The baseline cost of energy is expected to be higher than the ultra‑lean, Hormuz‑centric system of the 2010s. That means inflation is more likely to be structurally elevated, even if the war itself eventually de‑escalates. Investors need to ensure portfolios contain some element of protection against such inflation.

Chart 1: Australia Terminal Gate Wholesale Petrol Price – National Average (cents per litre)

2. More Dispersion

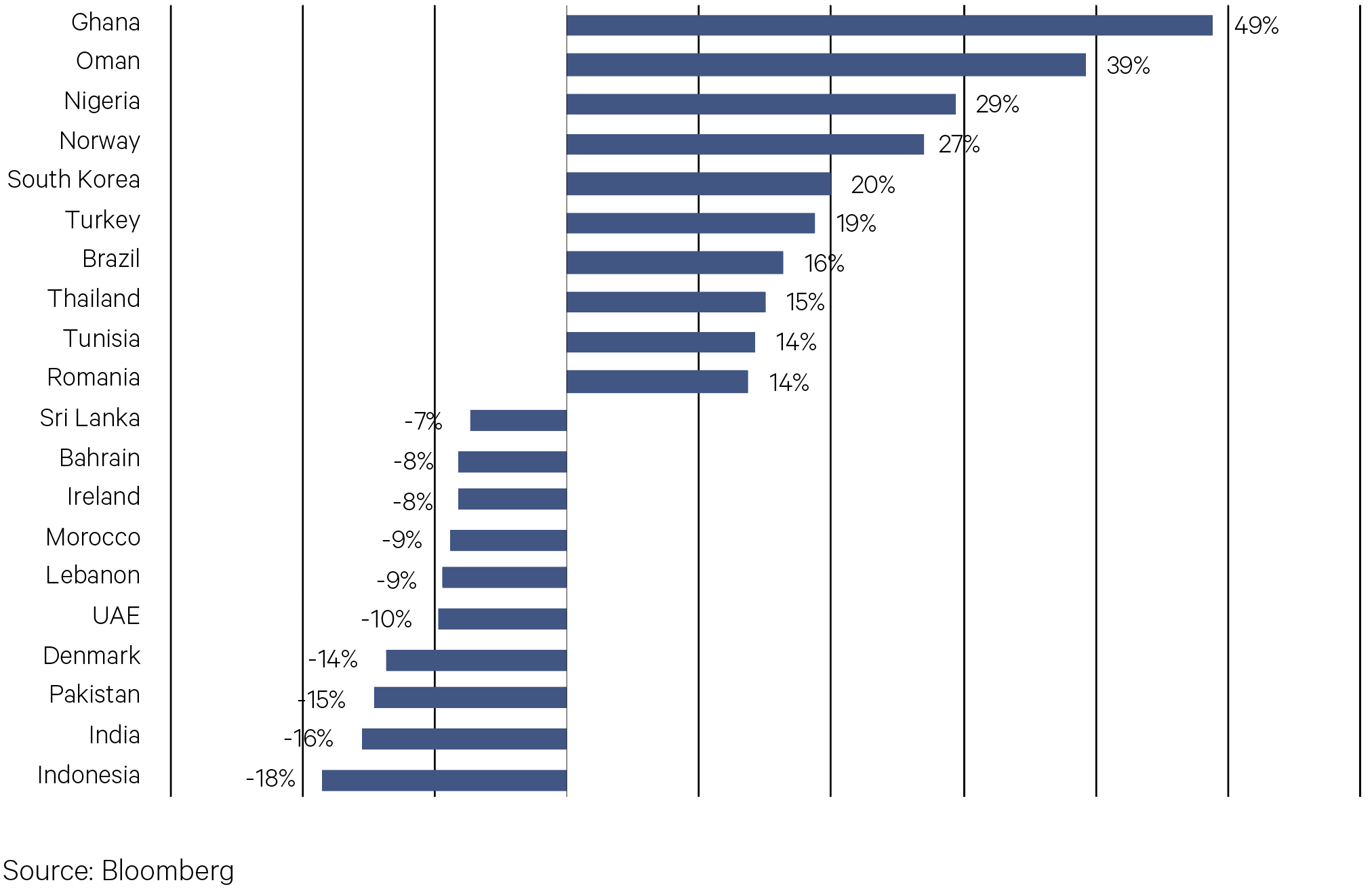

A single tail-risk event in any given decade would be significant; to experience several within a single quarter is something else entirely. The March quarter delivered an extraordinary clustering of extreme outcomes – from the US capture of Venezuelan President Nicolás Maduro, to escalating tensions over Greenland and the threat of tariffs on Europe and the UK, through to the outbreak of conflict between the US, Israel, and Iran. Tail‑risk events tend to trigger idiosyncratic responses from countries because nations differ in their fundamentals, policy space, and exposures – so the same shock hits each one in a distinct way. As the chart shows, Q1 wasn’t just volatile, it was dispersed.

Chart 2: The best and worst equity markets (March quarter returns (%))

3. More National

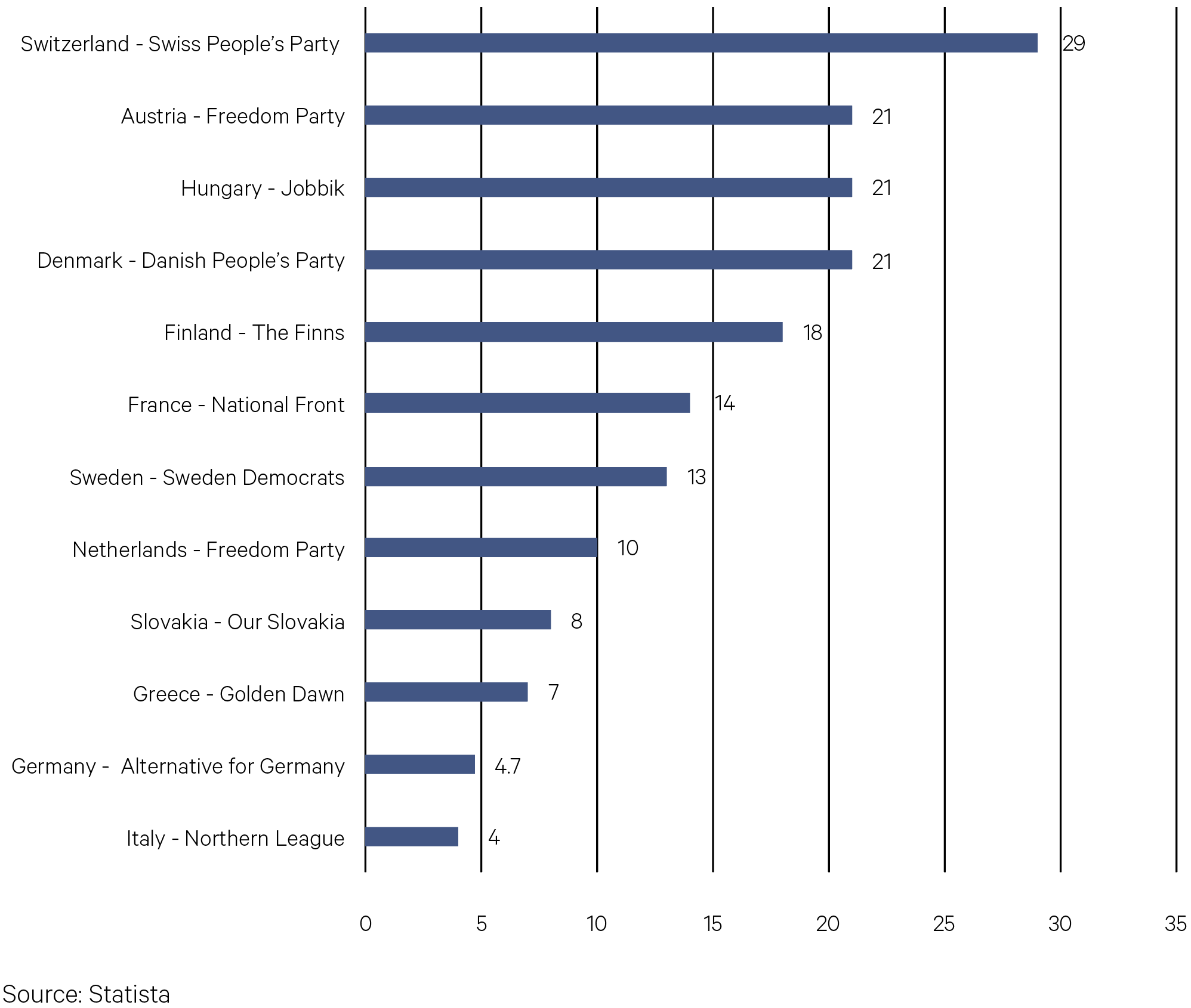

At the World Economic Forum in Davos in January, Rishi Sunak acknowledged that the old global order has given way to a more uncertain landscape, where nations must increasingly look inward to secure their own interests. Mark Carney went further, suggesting that the era of a rules-based global system has effectively ended. And Christine Lagarde observed that “we are seeing the curtain come up on a new world order,” calling for a fundamental rethink of how Europe structures its economy. Taken together, these perspectives point to a decisive shift away from globalism and toward a renewed emphasis on national resilience – where countries are prioritising sovereignty, self-reliance, and strategic autonomy as they respond to the demands of a more divided world. The chart shows how the popularity of nationalist parties has risen recently, particularly in Europe.

Chart 3: The rise of nationalism across Europe (% of votes won by nationalist parties in Europe’s most recent elections)

-

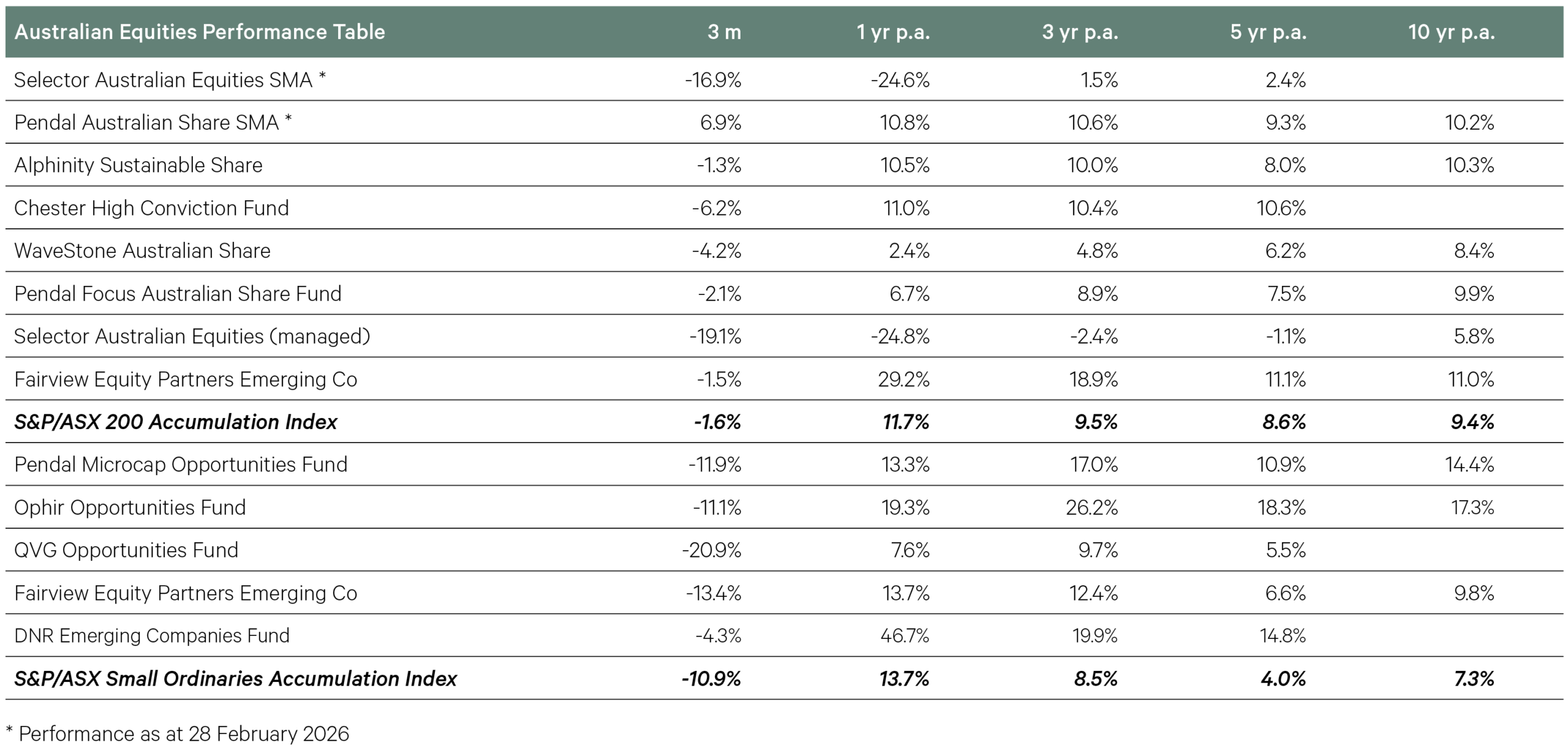

Australian Equities

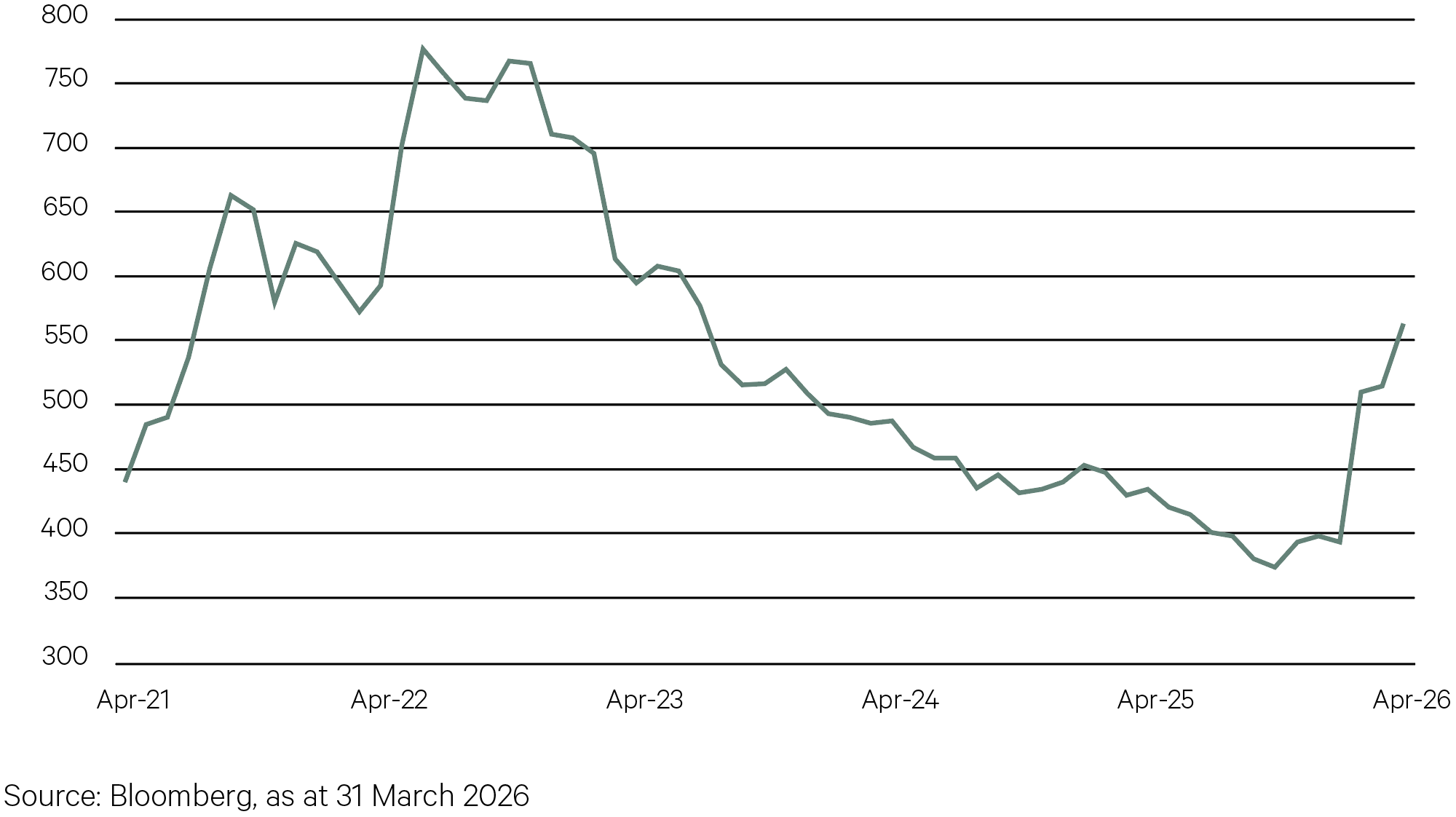

After commodity prices peaked following the Russian invasion of Ukraine in early 2022, a normalisation across most key commodities has been a headwind for the aggregate earnings of the Australian equity market. The last several months, however, have seen a sharp reversal of this downward trend, with resources again leading the earnings recovery. While iron ore has held more steady over the last year, gains across a broad suite of commodities, including gold, copper, oil, and coal, have all led to a 50% rise in forward earnings for the resources sector.

Chart 4: Resources lead rebound in earnings of Australian equities (Resources forward EPS)

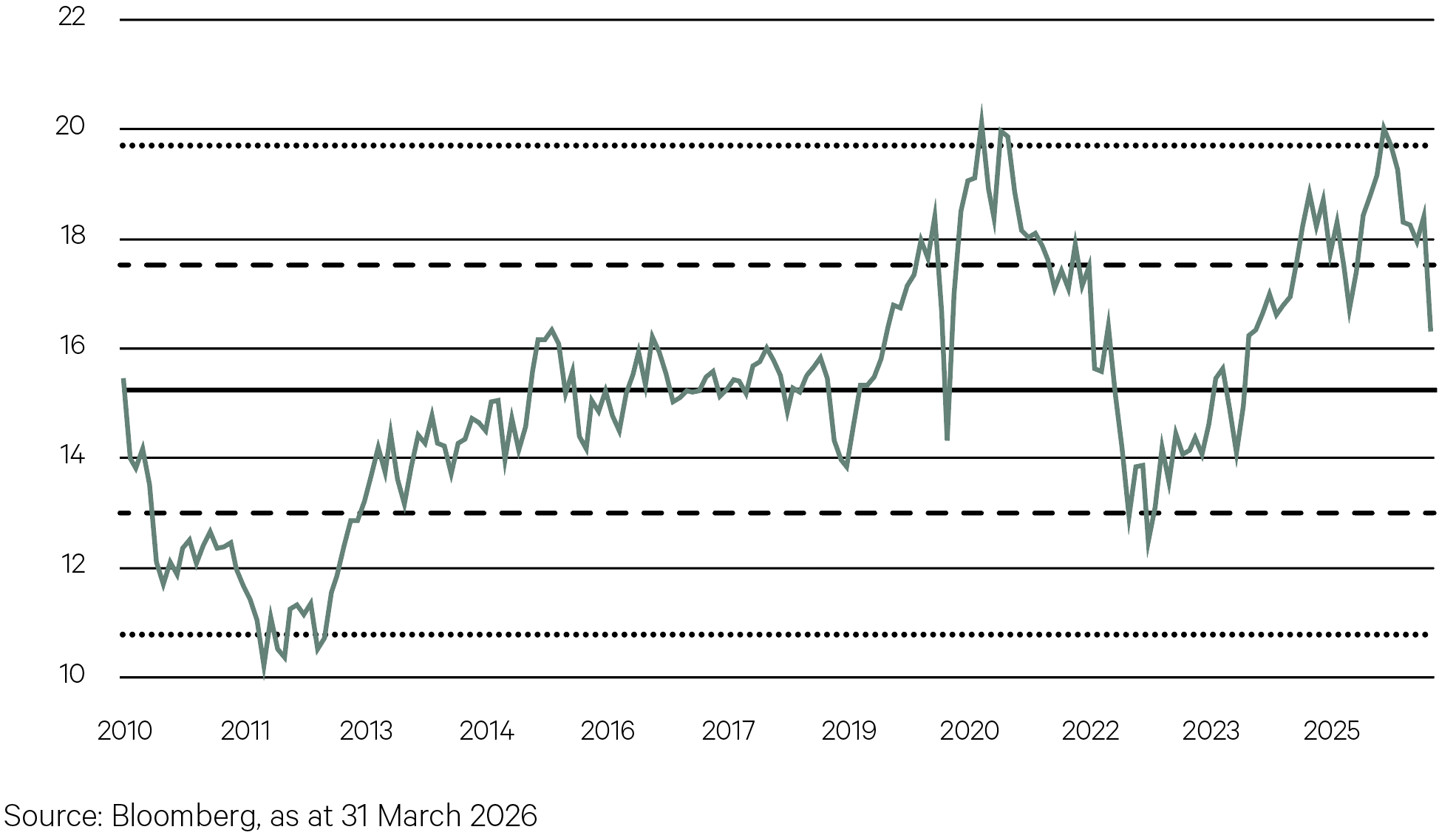

While earnings growth has been stronger in the Australian market in this financial year, returns have been weaker than the prior year amid a rise in geopolitical risk, a pickup in inflation, and bond yields which have pushed higher again. Over the last seven months, the forward P/E of the market has fallen from 20x to 16x – a large contraction which now sees the market trading at a ratio much closer to its longer-term average.

Chart 5: Australian market now no longer so expensive (ASX 200 forward P/E ratio)

Key Points

- The Australian equity market delivered a total return of -2.7% in the March quarter, with the decline across March attributed to the conflict in Iran and rising oil price more than offsetting gains across January and February. Despite the negative return, domestic equities managed to outpace the performance of international equities.

- The conflict in Iran was the focus of the market in March as oil spiked, leading to a large drawdown across most sectors of the market – energy being the key exception.

- This also fed through into domestic expectations for the cash rate and was sufficient for the RBA to follow up its first hike in the current cycle in February with another in March. Australia entered 2026 as one of the few developed market economies with a hawkish central bank (i.e. with a tightening bias), a stance which has been strengthened by higher inflation prints more recently, along with the challenges posed by an escalating oil price. With at least two further hikes now expected over the course of 2026, higher bond yields have followed, creating a headwind for longer-duration growth sectors of the market, particularly IT.

- IT and other capital-light sectors of the market were further challenged in the quarter on AI disruption fears, similar to their peers in international equity markets. This was reflected in a -28% return for the IT sector for the quarter.

- Across the quarter, the broader resources sector outperformed again, although the quarterly returns concealed significant volatility, particularly in the gold sector. After a parabolic rise in January, gold suffered a correction which picked up in March as higher bond yields, inflation expectations, and a stronger US dollar all outweighed the heightened geopolitical risk in markets.

- This news flow largely overshadowed what was a solid half-yearly reporting season for the Australian equity market. Results reflected a domestic economy that was strengthening over the six months to the end of 2025, and earnings growth across the key sectors of the market.

- Overall, the trends observed in the second half of 2025 were largely consistent with those of the March quarter, with relative fund performance primarily driven by two factors – on the positive side, the level of exposure to the resources sector, and on the negative side, the level of exposure to growth-orientated sectors of IT, health care, and consumer discretionary.

- Core funds performed better, particularly Alphinity Sustainable (despite the lack of fossil fuels in its portfolio), which had a productive reporting season in February on the back of good stock-picking across a number of sectors. The Selector strategy was the key laggard, given its predominant exposure to under-pressure growth stocks.

- In the March quarter, small caps faced the multiple headwinds of higher rates and inflation, along with the correction in the gold price – which is the dominant commodity exposure in the small resources sector. Further, small cap industrials suffered in the market’s drawdown across March. As we noted in the prior quarterly, DNR’s rotation into a broader resources exposure held it in good stead again in the March quarter. QVG’s growth-focused industrials portfolio lagged the most in this environment.

-

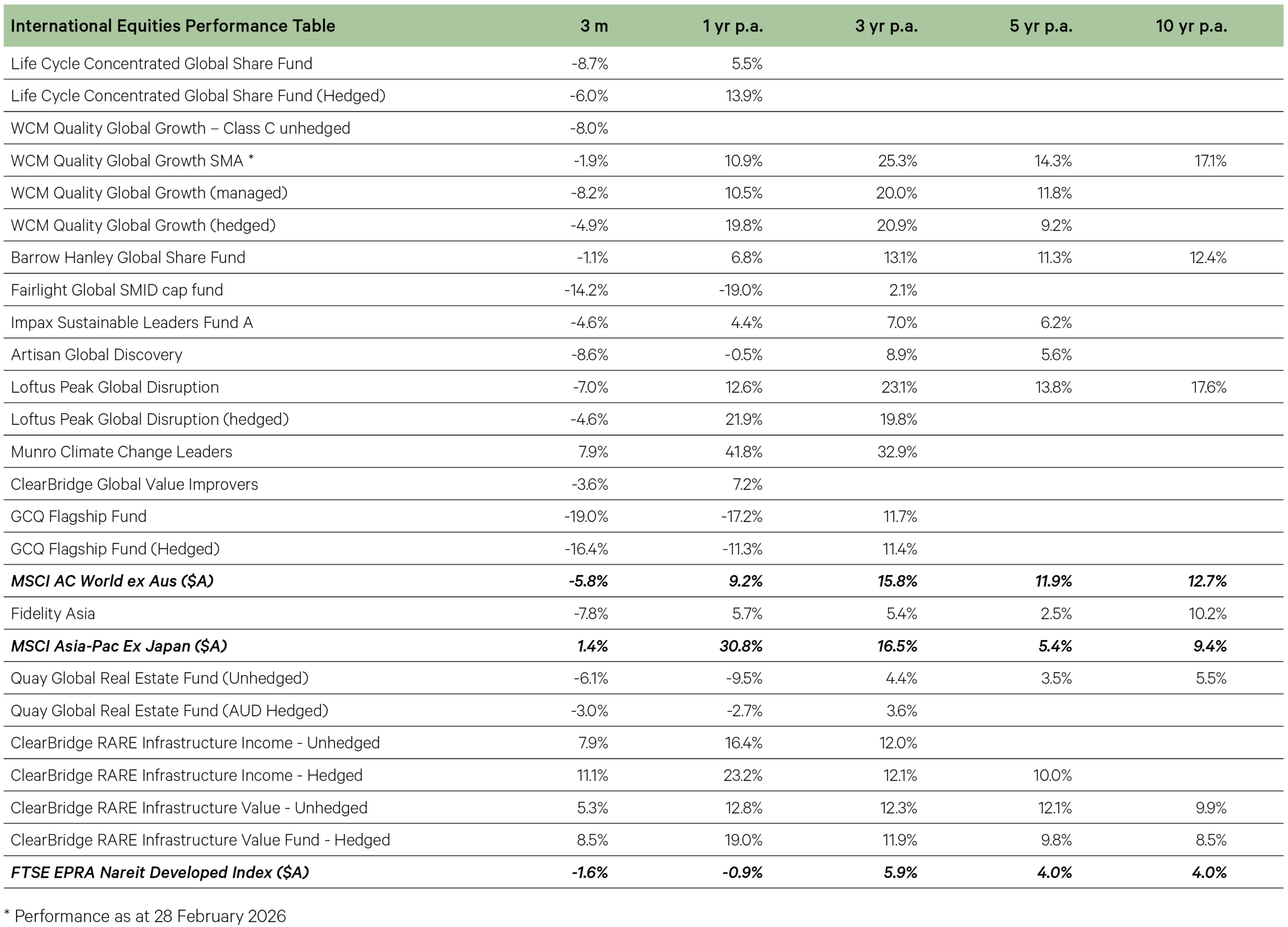

International Equities

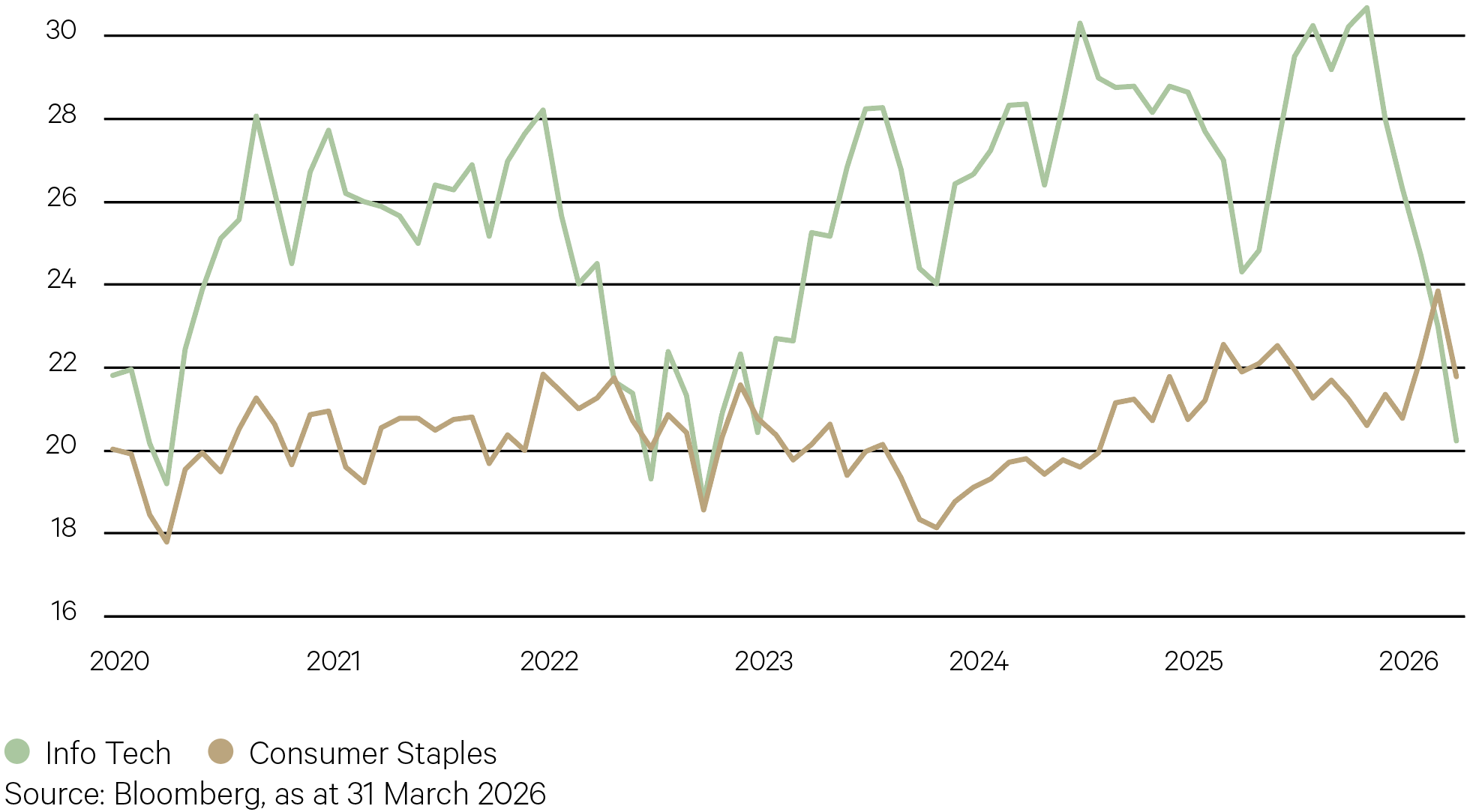

Exponential growth in hyperscaler data centre capex has been treated with a higher degree of scepticism over the last several months, with increased spending plans no longer met with an enthusiastic investor response. The release of more powerful agentic AI tools in the March quarter also led to a large compression in software valuations, as questions around the durability of business models rose. Both of these factors have led to a large de-rating of the US IT Index in a matter of months – from a forward P/E of >30x to just on 20x. The consumer staples sector now trades on a higher P/E than IT as investors seek greater short-term certainty amid a cloud of macro risks.

Chart 6: IT now cheaper than Consumer Staples (forward P/E ratio)

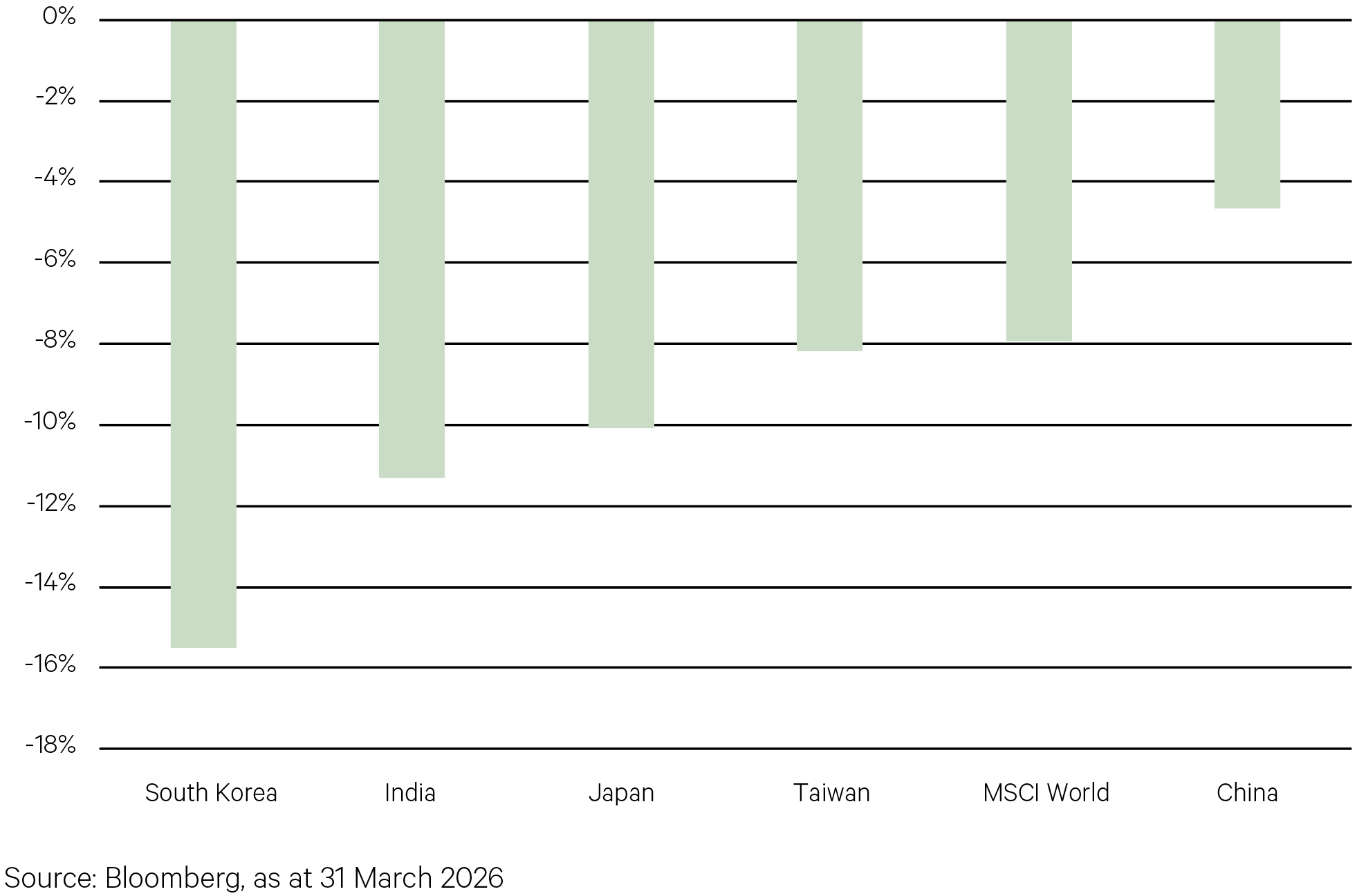

Several emerging equity markets enjoyed a stellar run over 2025 and into the early part of this year. For the 12 months to 28 February, South Korea was up 147%, Taiwan 54%, and Japan 47%. While many of these markets unsurprisingly sold off heavily in March as investors switched to ‘risk-off’, a bigger driver was more likely the high dependence on energy (both LNG and oil) from the Middle East that had effectively been cut off by Iran at the Strait of Hormuz. China similarly has a high energy dependence from the region; however its significant petroleum reserve saw it less impacted than others.

Chart 7: Asian markets suffer the most from Iran war (March returns)

Key points

- Global equity markets made further gains in early 2026 before pulling back in March on the Iran war and subsequent escalation in the oil price. For the quarter, developed markets fell 3.9% and emerging markets by 0.5%, though unhedged returns were greater as the Australian dollar strengthened further across January and February.

- Across January and February, markets followed a similar pattern of leadership from late last year. With earnings growth broadening, markets that are more cyclical in nature led the way, with strong returns in particular in emerging markets.

- Technology and other capital light sectors and companies faced greater challenges on the release of more sophisticated agentic artificial intelligence tools, which threatened to undermine the strength of businesses previously thought to have minimal disruption risk. This weighed on the Nasdaq and the US market more broadly.

- Among developed markets, Japan outperformed again and received a boost on the re-election of prime minister Sanae Takaichi.

- The Iran war saw oil spike, raising concerns around higher inflation and interest rates, while crowded trades in gold and emerging markets became sources of liquidity. Higher beta areas of the market, such as small caps and emerging markets sold off heavily.

- With equity returns showing high dispersion, fund returns showed a similar wide range of outcomes, with defensive and value-orientated funds faring better.

- The better performers included Clearbridge RARE Infrastructure and Munro Climate Change Leaders. Clearbridge RARE’s positive structural thematics and defensive qualities held it in good stead, while Munro’s outperformance was driven by solid stockpicking, particularly in February.

- Barrow Hanley also performed well, with its value style helped by the initial cyclical rotation in markets while similarly avoiding many stocks and sectors exposed to AI disruption risk. More growth-orientated funds such as WCM and Loftus Peak lagged in this environment.

- Funds that implement a high ‘quality’ overlay to their stock selection were among the biggest laggards in the March quarter and were the most impacted by the peak ‘AI disruption’ fears – this was a drag on the performance of GCQ and Fairlight.

-

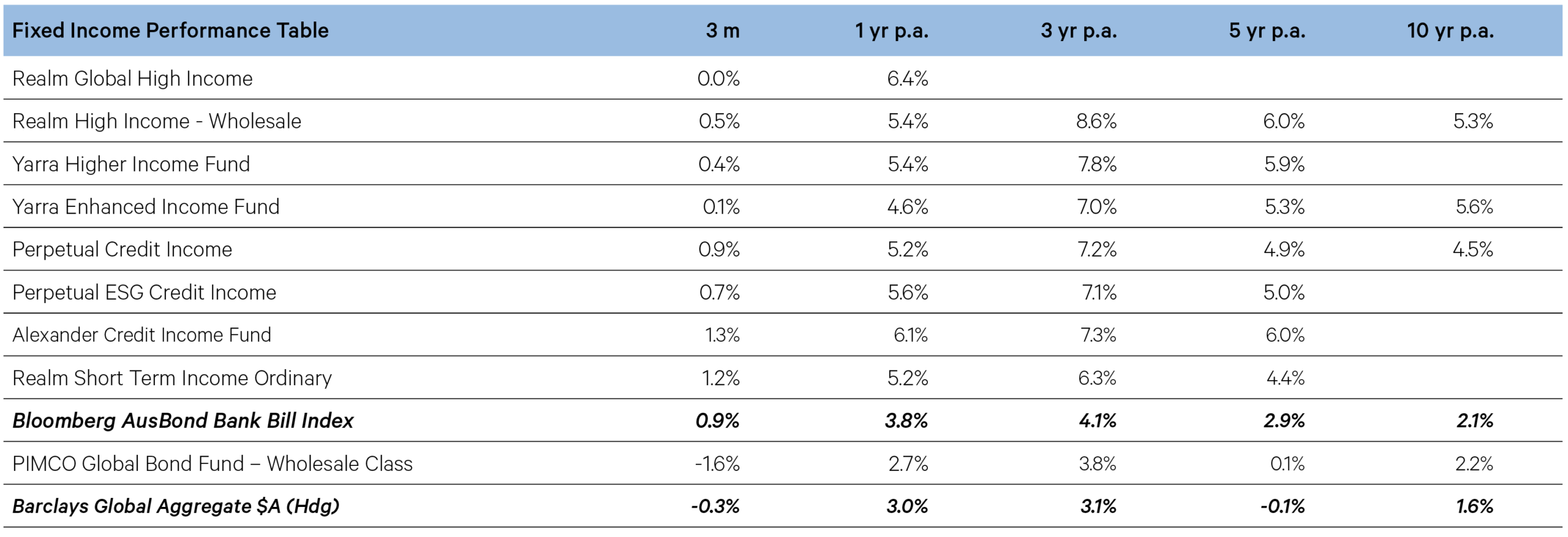

Fixed Income

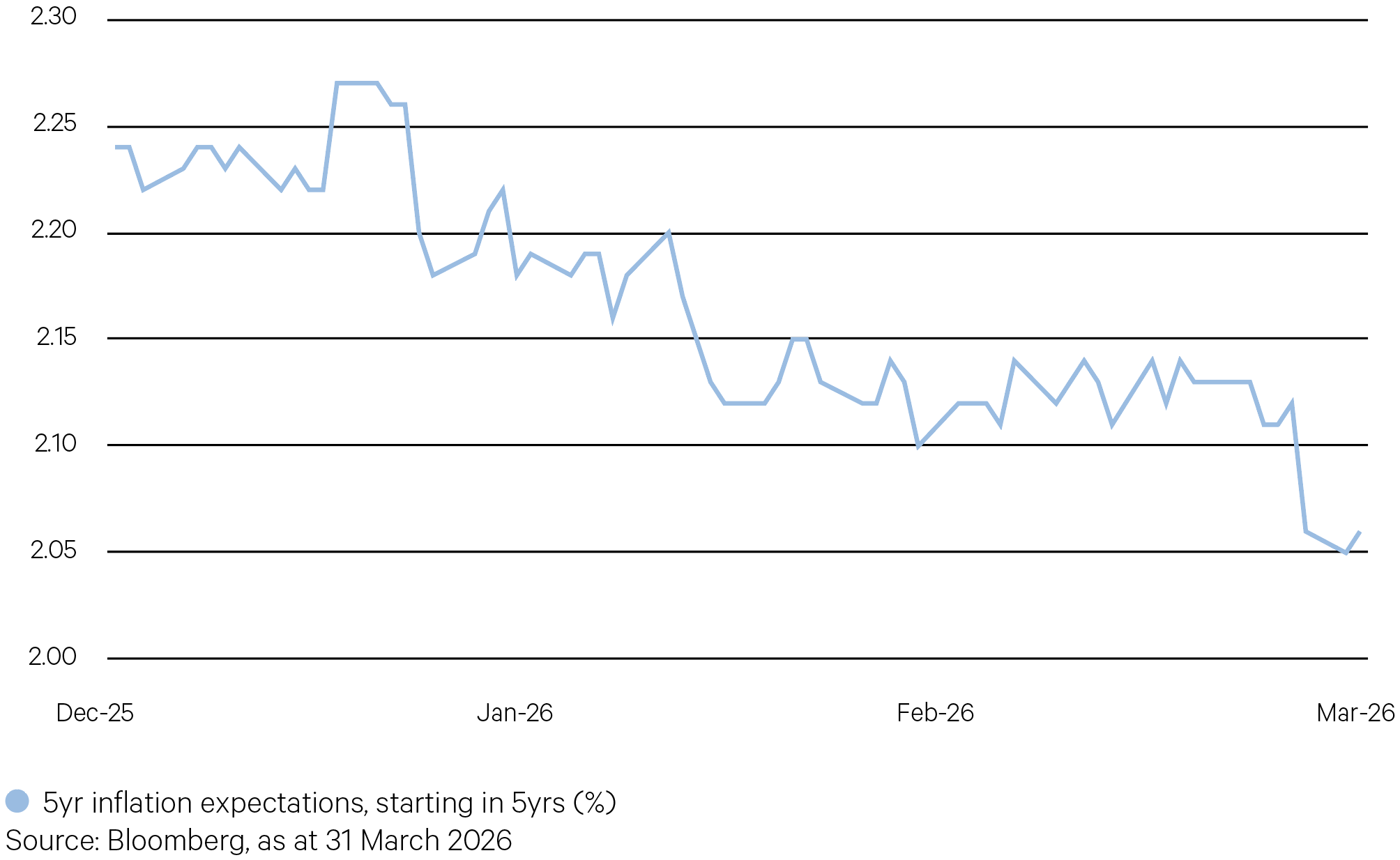

While the oil shock is expected to lead to elevated short-term prices in the US, markets aren’t pricing an acceleration in long-run inflation. In fact, expectations for average inflation over the 5 years beginning in 2031 have reduced over the quarter by approximately 20bps. This is because supply shocks typically weigh on economic growth, slowing business activity and reducing the ability of firms to pass on costs to consumers – putting a ceiling on potential inflation.

Chart 8: US Still Pricing for Controlled Long-Run Inflation

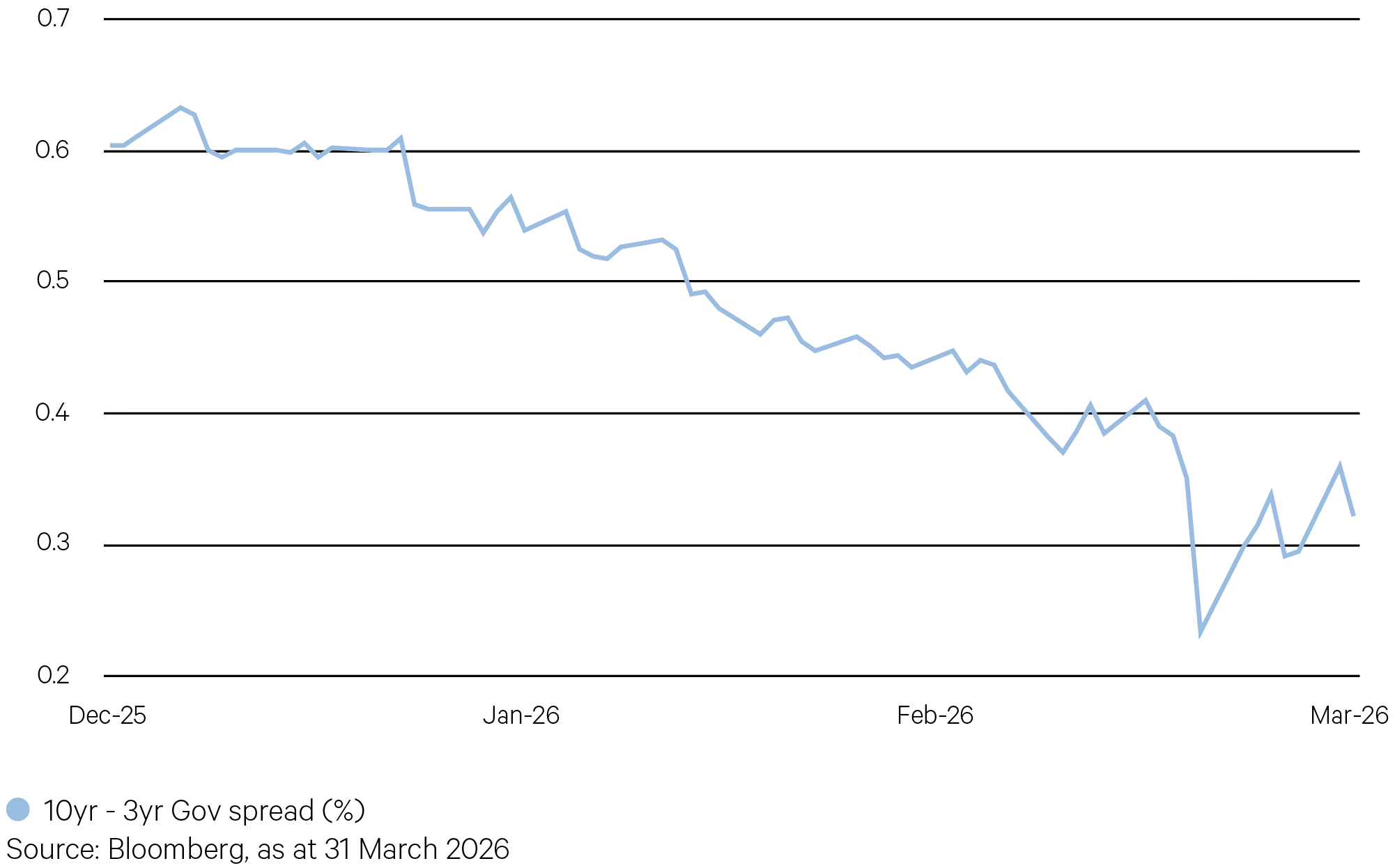

The Australian yield curve experienced a bear flattening over Q1 as short-term yields rose more than long-term yields. The 3-year government yield rose by around 50bps as markets priced for higher inflation in the near-term and additional rate hikes by the RBA. The 10-year yield also rose, but only around half as much, as the market balanced long-run inflation and fiscal expectations with the potential for an economic slowdown. If the yield curve inverts, with the spread between long- and short-term yields turning negative, this is typically indicative of a pending recession.

Chart 9: Australian Yield Curve flattening

Key points

- The March quarter was the perfect storm for fixed income as conflict in the Middle East derailed disinflationary measures globally. Yields rose in anticipation of higher inflation as oil prices spiked, while credit spreads widened over broader concerns about AI disruption and credit stress. Fears of stagflation, a tricky combination of low economic growth and sustained inflation, began to rise.

- The RBA delivered back-to-back hikes on stubborn CPI prints, despite the uncertainty caused by the Iran conflict. The March decision was far from unanimous, with the board split 5-4 in favour of a hike. Oil price shocks historically have had a mixed impact on the Australian economy, but generally have led to higher inflation, rate hikes, and a collapse in GDP growth. Conservative estimates show the increase in petrol prices since the beginning of the Iran war having the same impact as a rate hike on a household with a $700k mortgage.

- Central Banks in other developed markets held steady, citing increased uncertainty over the impact of the oil shock. Monetary policy is less effective when inflation is supply-driven, as the pressure of higher rates risks slowing growth to the point of recession.

- Credit spreads widened over the quarter, and while they remain close to historic tights, this was a headwind for funds with exposure to credit risk. Concerns around private credit stress were reflected in their public counterparts; a sign that the line between public and private is not as clear cut as believed. This was particularly evident in the CLO and BDC markets, which have significant exposure to software issuers – a key area of concern in private markets.

- Our liquidity funds fared best in the quarter, owing to their low exposure to both credit and interest rate risk. Realm Short Term and Alexander Credit posted positive returns in March. Although part of our credit allocation, Perpetual Credit Income’s conservative positioning benefitted returns, as it avoided most of the pain over the quarter.

- Interest rate duration detracted in the quarter as yields rose, particularly in March. A slight overweight to duration led to PIMCO Global Bond underperforming its benchmark in the quarter. Even small exposures to duration were punished, a headwind for both Yarra funds and Realm High Income funds in March.

- While this quarter was challenging for fixed income, it’s important to focus on the primary return driver of the asset class: income. Our funds are primarily invested floating rate instruments, which increase their income payments with the RBA cash rate. Higher running yields provide a cushion for funds to absorb short-term volatility and still generate positive annual returns.

-

Alternatives

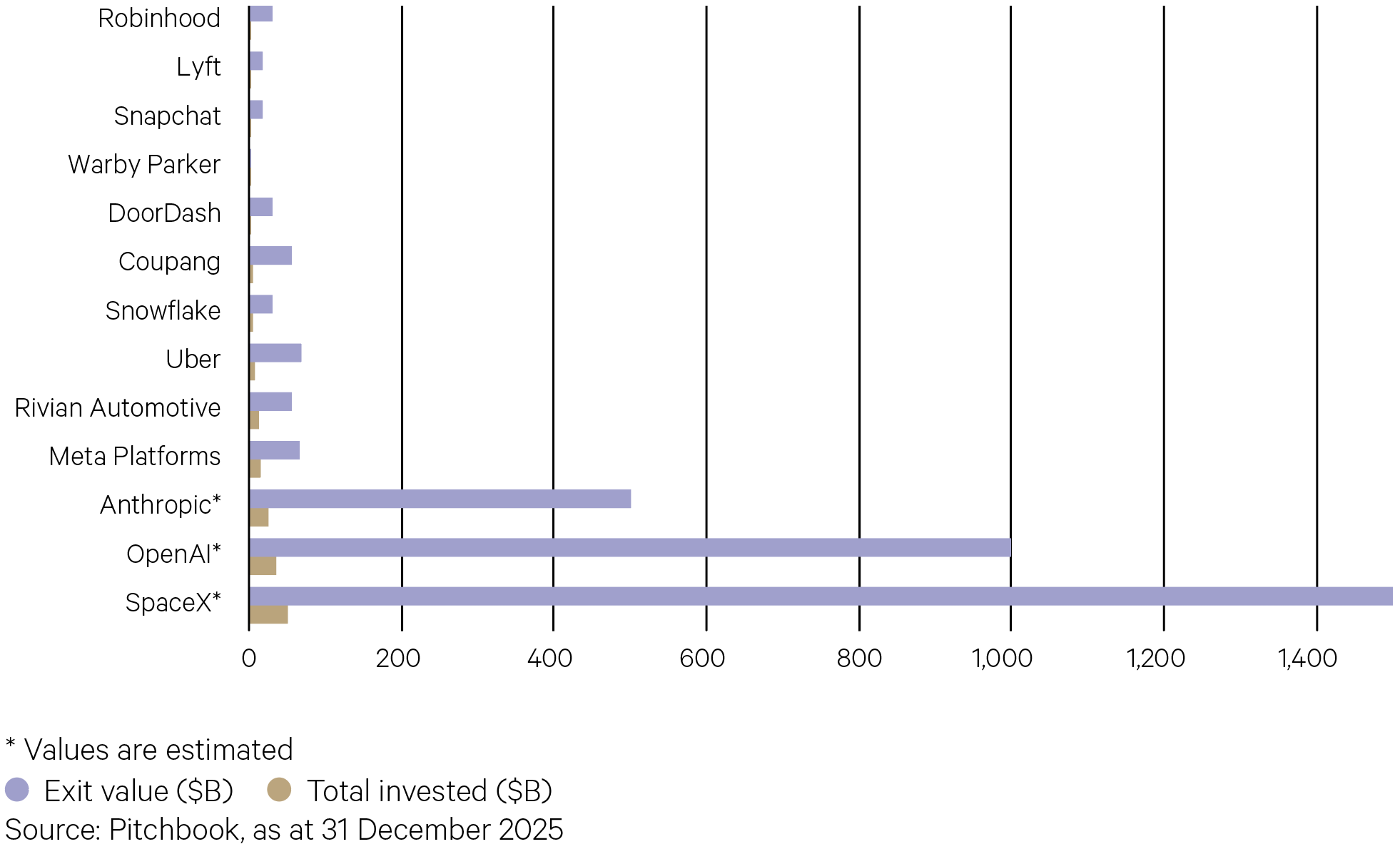

Following increased IPO activity in 2025, expectations were high for similar momentum in 2026. Companies like SpaceX, OpenAI, and Anthropic are rumoured to go public this year. Meta (formerly Facebook) went public at a $104 billion valuation, however SpaceX, OpenAI, and Anthropic now all have much higher values. According to Pitchbook, if they proceed with IPOs, they could become the largest VC-backed public offerings ever, creating more value than all VC-backed IPOs since 2000 combined. As key players in the AI market, successful listings from OpenAI and Anthropic would substantiate the significant amounts of capital investment pouring into the sector.

Chart 10: Largest VC-backed IPOs by proceeds raised

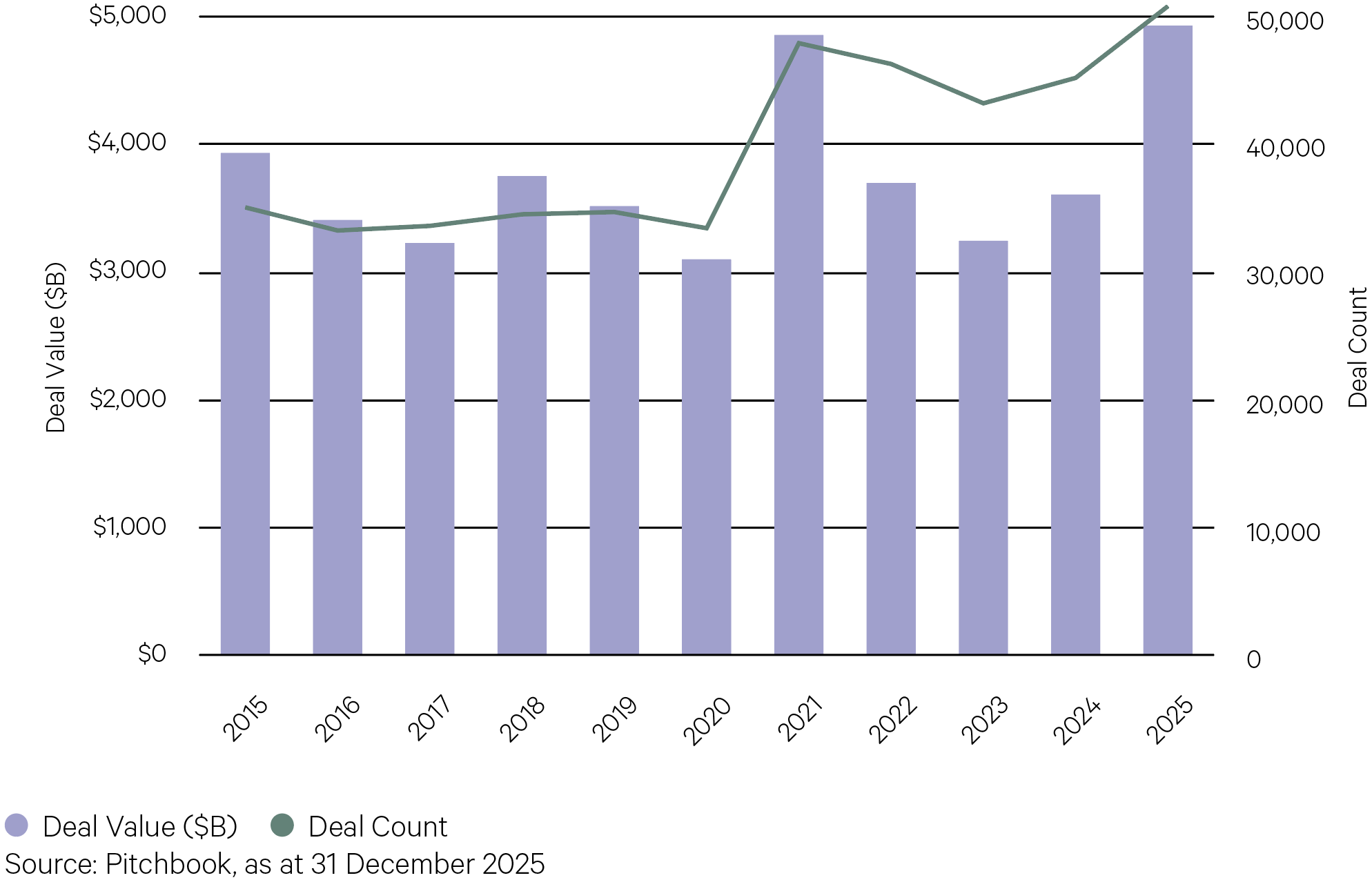

In 2025, global mergers and acquisitions (M&A) reached record levels, with both the number and value of deals surpassing those in 2021. For the first time, M&A activity exceeded 50,000 deals – the total value just below $5 trillion. Compared to the previous year, deal count rose by 12.4%, while the value of deals increased by 37%. One major factor behind this growth was the rise in megadeals—transactions worth $1 billion or more—which contributed $2.6 trillion, making up 56.6% of the total global M&A value. Lower interest rates from the US Federal Reserve and European central banks boosted financing options and encouraged greater risk-taking for substantial acquisitions.

Chart 11: Global M&A activity

Key points

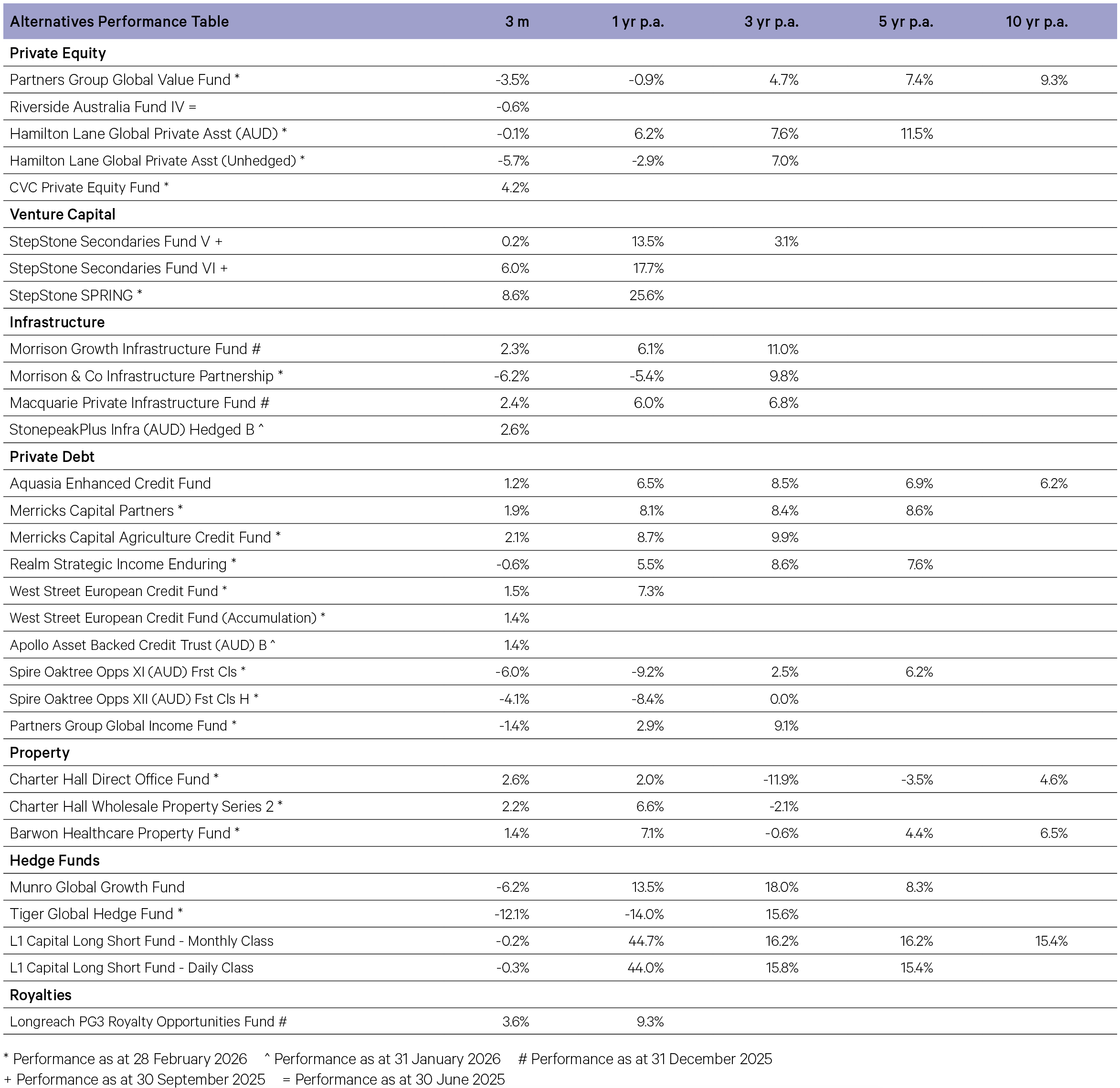

Private Equity

- Partners Group Global Value Fund declined -3.5% for the three months ending February 2026. Assets exited via public listing and held in escrow impacted performance negatively during the period, reflecting broader public market volatility. Public exposures in positions such as Galderma, Zabka Group, KinderCare Learning, and Vishal Mega Mart, were notable detractors – all of which have otherwise continued to perform well operationally. In contrast, private assets continued to create value in the portfolio through the period. Positions in Rosen Group and St. Croix Hospice were solid contributors.

- Hamilton Lane Private Assets Fund (Unhedged) returned -5.7% for the three months ending February 2026. The depreciation of the US dollar against the Australian dollar drove negative performance across the period. The underlying portfolio delivered positive returns through the period, driven by gains in secondaries and co-investments, with secondaries being the primary contributor. One of the top contributors was Project Minerva, a GP-led, single-asset continuation vehicle into Multiversity — the leading online higher education platform in Italy. Other notable positive contributors included TradingView, a global charting and analytics platform.

Private Debt- West Street European Private Credit Fund returned +1.5% for the three months ending February 2026. Underlying loan income was strong during the period, with the fund predominantly invested in directly originated, floating-rate first lien loans. The portfolio spans eleven sub-sectors across twelve countries. During the period major new positions were established in Innovad, Sapiens, and Key Group.

- Partners Group Global Income Fund returned -1.4% for the three months ending February 2026. The portfolio generated consistent income across the period however this was more than offset by the drop in loan prices in the technology and professional services related sectors, reflecting AI-related market volatility rather than any fundamental deterioration in underlying portfolio asset quality. Syndicated loans in the portfolio caught by the AI-related market volatility experienced higher volatility given the daily mark-to-market of such loans. During the period, the fund increased its direct credit exposure.

- Merricks Partners added +1.9% for the three months ending February 2026 supported by income from senior secured, asset-backed loans and a modest performance uplift from the fund’s credit default swap protection. During the period, several maturing loans progressed toward repayment following contracted asset sales, including the York Street Sydney office facility. The fund has a solid pipeline of redeployment opportunities, with its current focus on senior exposures across residential, retail, agriculture, and selective resources.

Hedge Funds- L1 Capital Long Short returned -0.3% (Daily class) for the three months ending March 2026. Performance across the period was volatile with strong gains in January broadly offset by losses in March. Key positive contributors across the period included Alcoa, Finning, and NewGen. On the downside, positions in Flight Centre, Light and Wonder, and James Hardie detracted.

- Equity long short manager Munro Global Growth returned -6.2% for the three months ending March 2026. Long equities drove negative returns whilst short positions were additive. Key contributors across the quarter included Ciena Corp, CATL, GE Vernova and TSMC. Detractors included positions in Amazon, CRH, Alphabet, and Rheinmetall.

Venture Capital- StepStone Private Venture and Growth Fund (SPRING) added +8.6% for the three months ending February 2026. Performance of the fund was driven by valuation changes to several portfolio companies, as a result of fundraising rounds, GP marks, and employee tender rounds. During the period, SpaceX saw a valuation increase following its merger with xAI. SpaceX’s acquisition of xAI creates a vertically integrated platform combining AI models with physical infrastructure. OpenAI contributed following its latest fundraising round that saw the company’s valuation increase. The funding round includes investment from SoftBank, Nvidia, and Amazon.

Infrastructure- The Macquarie Private Infrastructure fund returned +2.4% over the December quarter. The fund benefitted from positive performance across most of its underlying investments with notable positive contributors including the Port of Newcastle, Aligned Data Centers, Vocus Group, and Diamond Infrastructure Solutions. Portfolio activity during the quarter included the fund securing co-investment positions in Bristol, Birmingham, and London City Airports; as well as the divestments of Aligned Data Centers, ElectraNet, and North Queensland Airports.