-

Q2 in review –

This is one of the big ones

AI remained the dominant investment theme in Q2 2026 but the market’s focus broadened beyond the software platforms and hyperscalers. Instead, investors rewarded the companies, industries and countries building the physical AI componentry required to deploy AI at scale. From semiconductor equipment and memory to networking, power management and advanced manufacturing, markets are recognising that AI is one of the largest industrial capital expenditure cycles in history.

As Sam Altman, CEO and co-founder of OpenAI says, “this is not even a technological shift that happens every generation. This is one of the big ones.” This shift was accompanied by broader geographic leadership and a supportive liquidity backdrop, as the Japanese yen once again emerged as an important funding currency for global risk assets.

1. Moving along the value chain

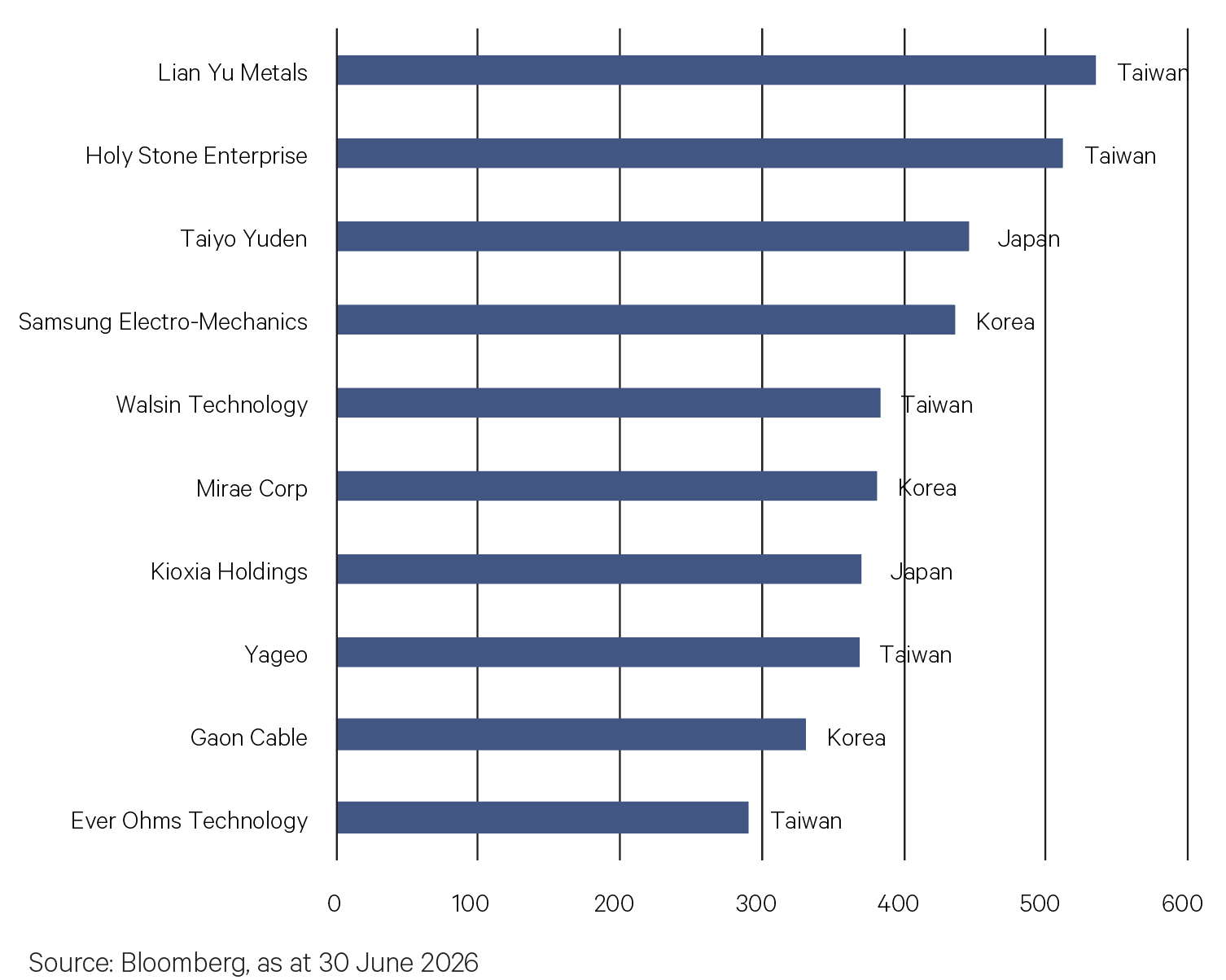

For much of the past two years, AI investing largely meant owning the Magnificent 7 – the companies developing and commercialising artificial intelligence. During the June quarter, markets shifted their focus towards the component makers of the AI revolution. This includes makers of memory chips, semiconductor equipment, electronic components, advanced packaging, printed circuit boards and optical networking. These businesses may be less well known than NVIDIA or Microsoft, but they occupy some of the most critical positions in the AI supply chain. As AI deployment accelerates, they are solving the engineering bottlenecks associated with compute, power, connectivity, and data movement. In many respects, the June quarter marked the point at which markets began recognising AI not simply as a software revolution, but as one of the largest industrial capital expenditure cycles in decades.

Chart 1: Q2 performance (%) for the top 10 global AI infrastructure companies

2. The AI build-out goes global

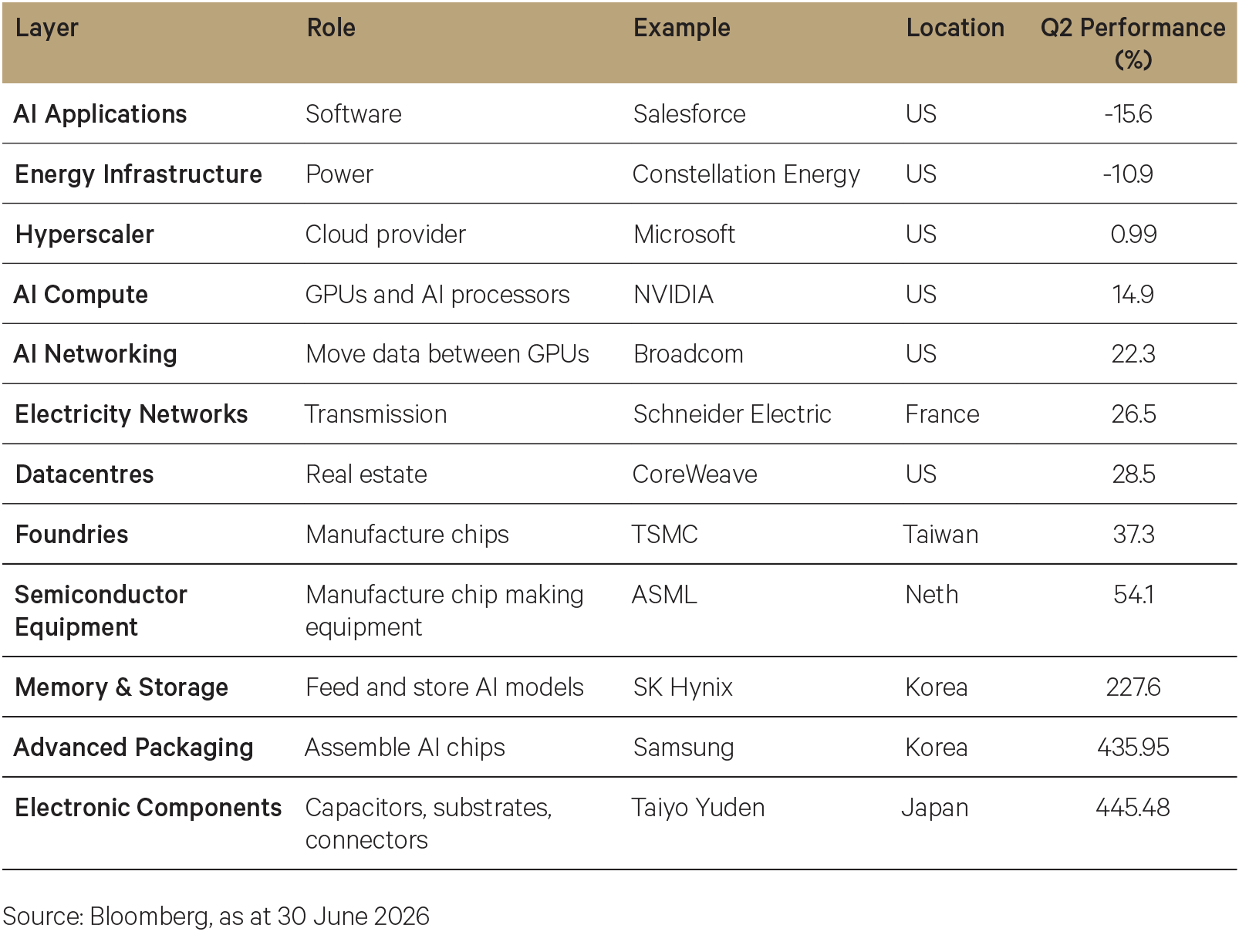

The broadening of market leadership in the quarter was not a sector story; it was a geographic story. The strongest performers were concentrated in the countries occupying critical positions within the global AI supply chain. Japan benefited through semiconductor equipment and advanced manufacturing; Korea through memory and packaging; Taiwan through substrates and chip fabrication; Europe through electrification and automation; and the United States through memory, storage, and networking. By contrast, many of the weakest performers remained concentrated in China’s domestic economy, Indonesian resources and traditional commodity sectors. Markets were not rewarding Asia indiscriminately – they were rewarding the economies building AI.

Table 1: The AI value chain

3. Yen carry trade is back

The weaker Japanese yen in Q2 was more than a currency story. It reflected Japan’s continuing role as a source of low-cost funding for global capital markets. As the Bank of Japan maintained a gradual approach to policy normalisation, the yen re-emerged as an attractive funding currency, supporting risk assets globally. A weaker yen also reinforced Japan’s competitiveness, providing an additional earnings tailwind for its globally competitive manufacturers. While AI capital expenditure remained the principal driver of Japan’s equity market, supportive liquidity conditions amplified investor appetite for Japanese and global risk assets.

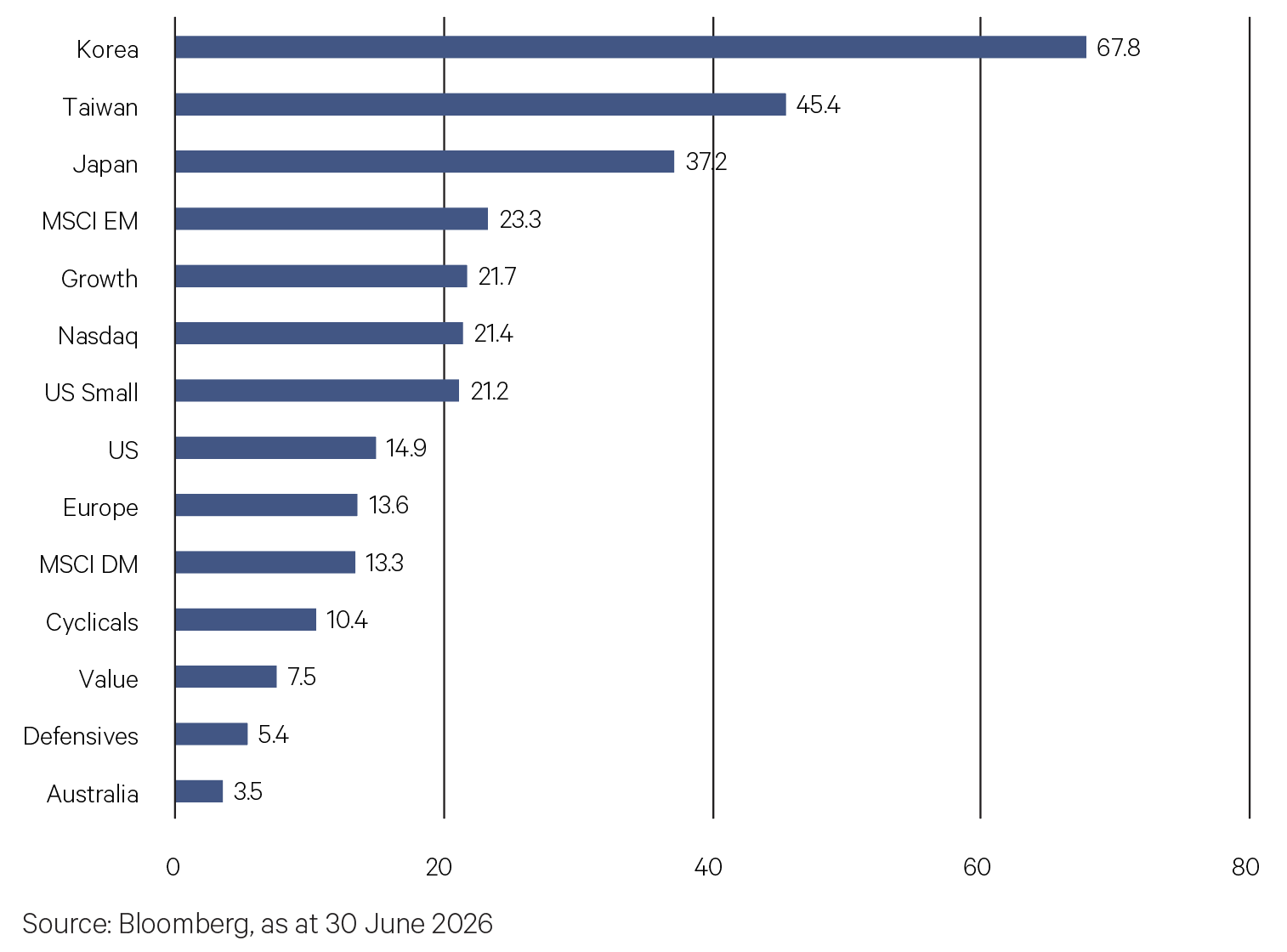

Chart 2: Q2 equity returns (%)

-

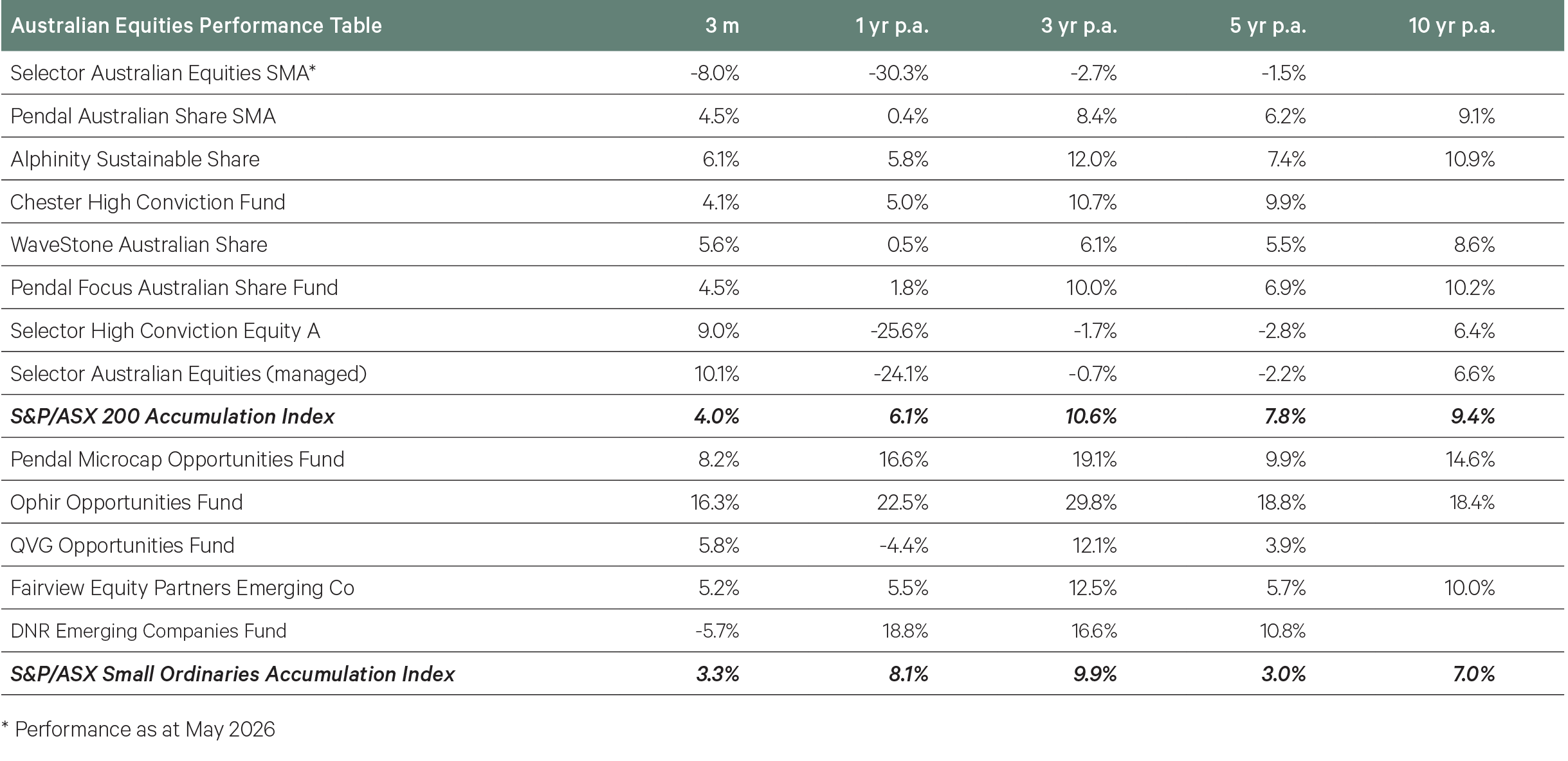

Australian Equities

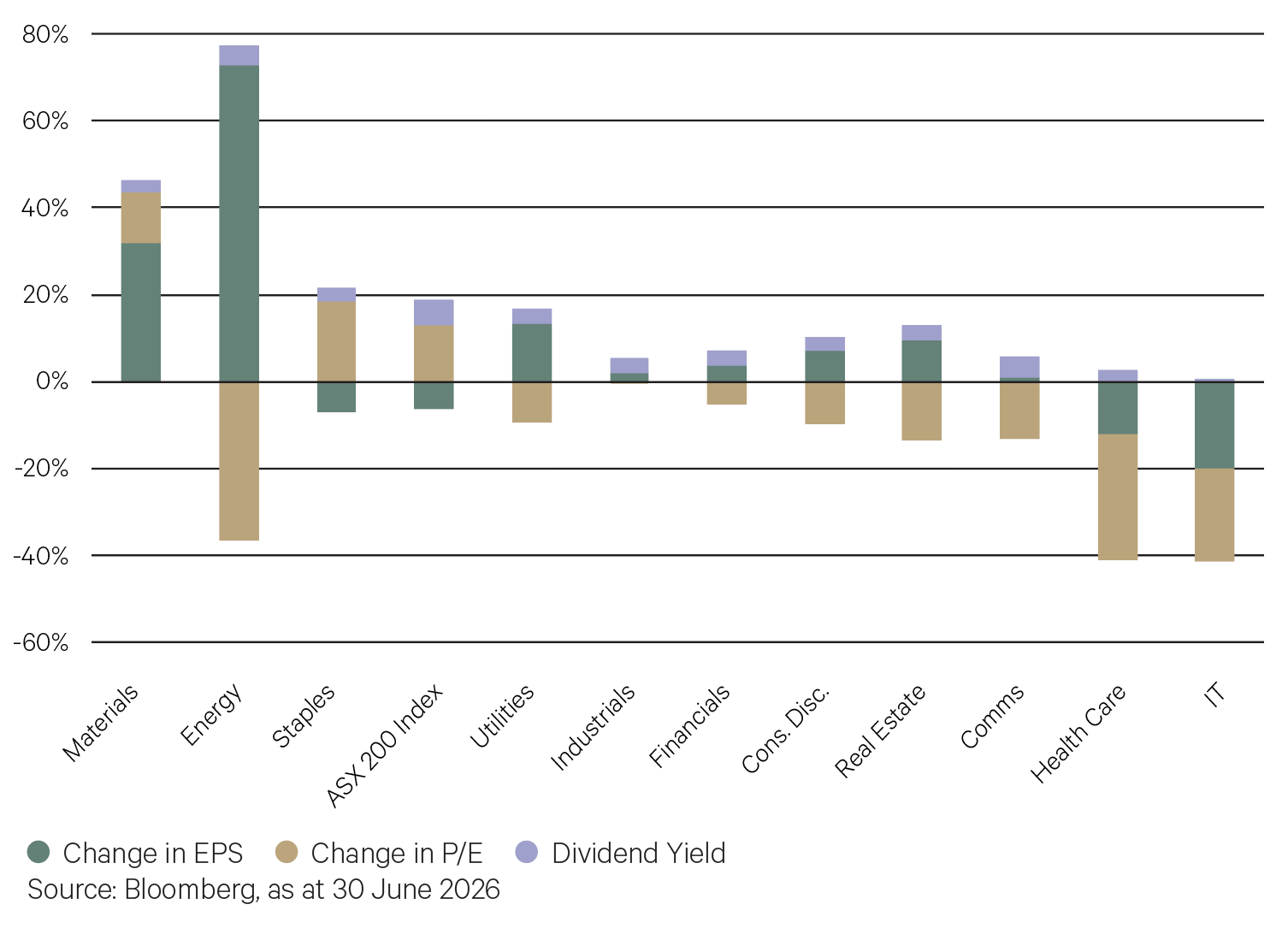

While the Australian equity market generated a modest 6.1% total return in FY26, overall returns were driven by earnings expansion, with the P/E of the benchmark index contracting over the year. Sector returns were a key driver of fund performance, with the resources sectors of materials and energy both leading the market as commodity prices strengthened. Meanwhile, high quality growth sectors of health care and IT endured a horror 12 months amid weak operational performance (particularly in health care) and AI disruption risk (in IT), dragging earnings and P/Es lower.

Chart 3: ASX 200 FY26 composition of returns

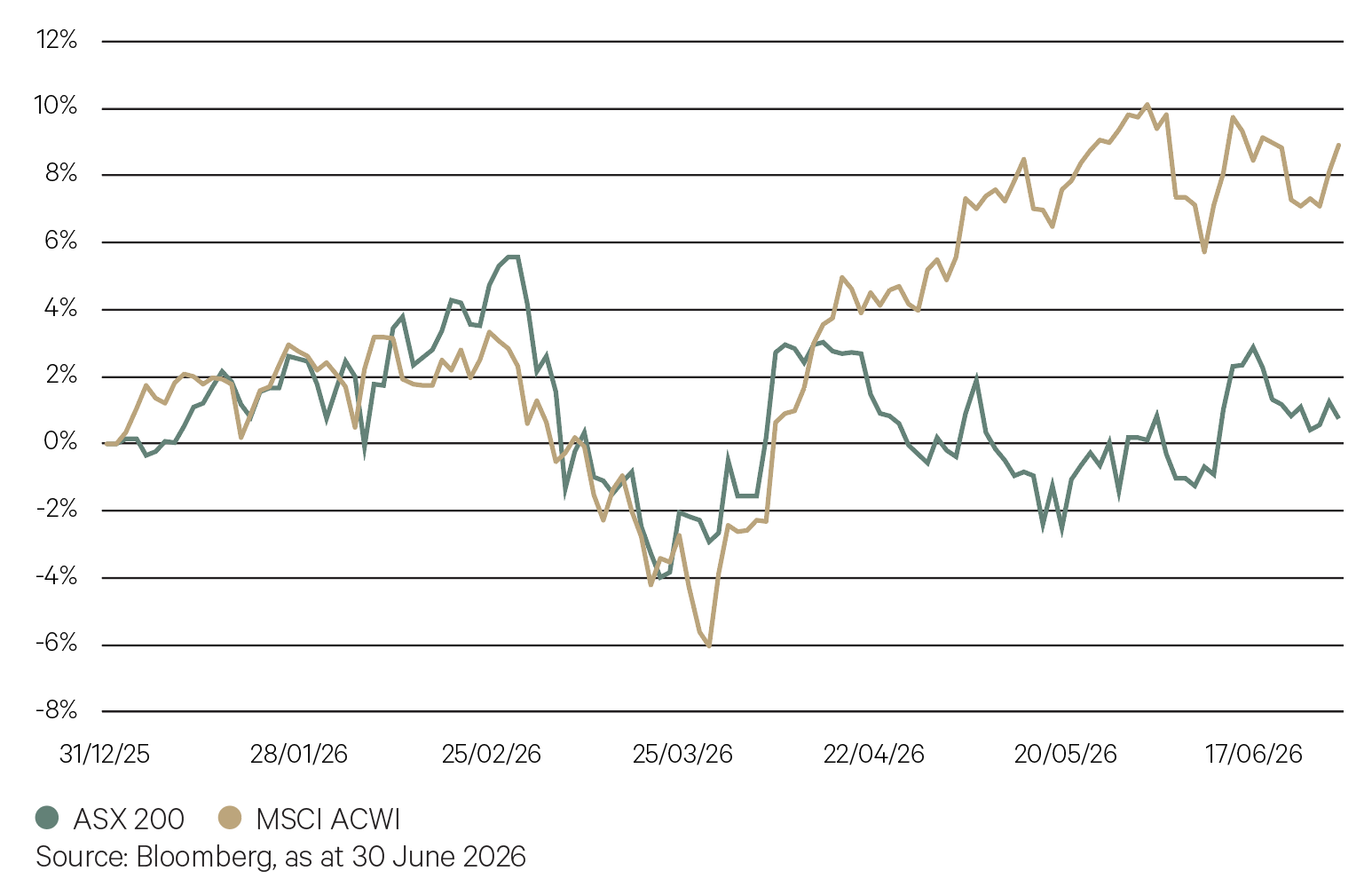

The Australian market tracked global equity markets across the first few months of the year, starting the year well before falling sharply on the commencement of the conflict in Iran. The initial recovery in late March was similar to that of the rest of the world until the local market lagged materially over the ensuing weeks as AI infrastructure names (which our market lacks) assumed market leadership.

Chart 4: ASX 200 lags recovery

Key Points

- The Australian equity market eked out a positive quarter to close out the financial year, with gains recorded in early April on the back of the initial recovery from the Iran conflict. Despite the initial rebound, the ASX 200 failed to recover to its pre-war levels, becoming more range-bound over the following three months. Overall, the quarter contributed to a modest 6.1% gain for the Australian equity market for the 2026 financial year.

- While domestic returns were positive, our market significantly lagged the robust returns in international equities due to several factors. The most significant of these was the Australian market’s lack of exposure to companies leveraged to the AI infrastructure capex cycle.

- Secondly, the inflationary impulse from the spike in the oil price in March added to the hawkish stance adopted by the Reserve Bank, with inflation already rising before the Iran conflict. The central bank delivered a third rate hike in May, with potentially further hikes to come in the short term. Longer term bond yields, however, moderated towards the end of the quarter.

- Thirdly, a number of earnings downgrades started to filter through the market over the quarter, with stocks issuing profit warnings sold off heavily by investors. Stock-specific issues drove downgrades in key healthcare stocks CSL and Cochlear.

- Lastly, an unhelpful federal budget contributed to broad weakness across the market, particularly for companies exposed to the housing market. The major banks were identified as facing a more challenging environment going forward, with weaker credit growth and softening property prices adding to early indicators that the cycle has already turned.

- After driving returns for the broader market across prior quarters, returns in the resources sector were similar to that of industrials in the June quarter, with a number of key commodity prices weakening over June. The most significant of these was the oil price, which retreated towards levels prior to the Iran conflict, while the gold price continued to unwind from the sharp rally experienced across late 2025 and early 2026. The latter weighed in particular on the small resources index.

- Our large-cap, core funds were able to generate positive alpha across the quarter. Those with more of a growth bias, such as WaveStone, benefited from the rebound in both consumer discretionary and IT stocks for the three months. An underweight to the banking sector was also helpful for large-cap strategies in Pendal, WaveStone, and Alphinity Sustainable. Among mid-caps, Chester was a laggard, with the fund’s gold holdings a drag on the fund’s performance.

- After delivering vast outperformance over prior quarters, a retreat in small resources in June was a significant headwind for DNR Emerging Companies, with a pullback in gold, energy and lithium stocks. A recovery in industrial stocks provided a more conducive environment for funds such as QVG Opportunities. Pendal Microcaps was another strong performer in the quarter on the back of solid stock-picking, with the fund well ahead of benchmark across all key timeframes.

-

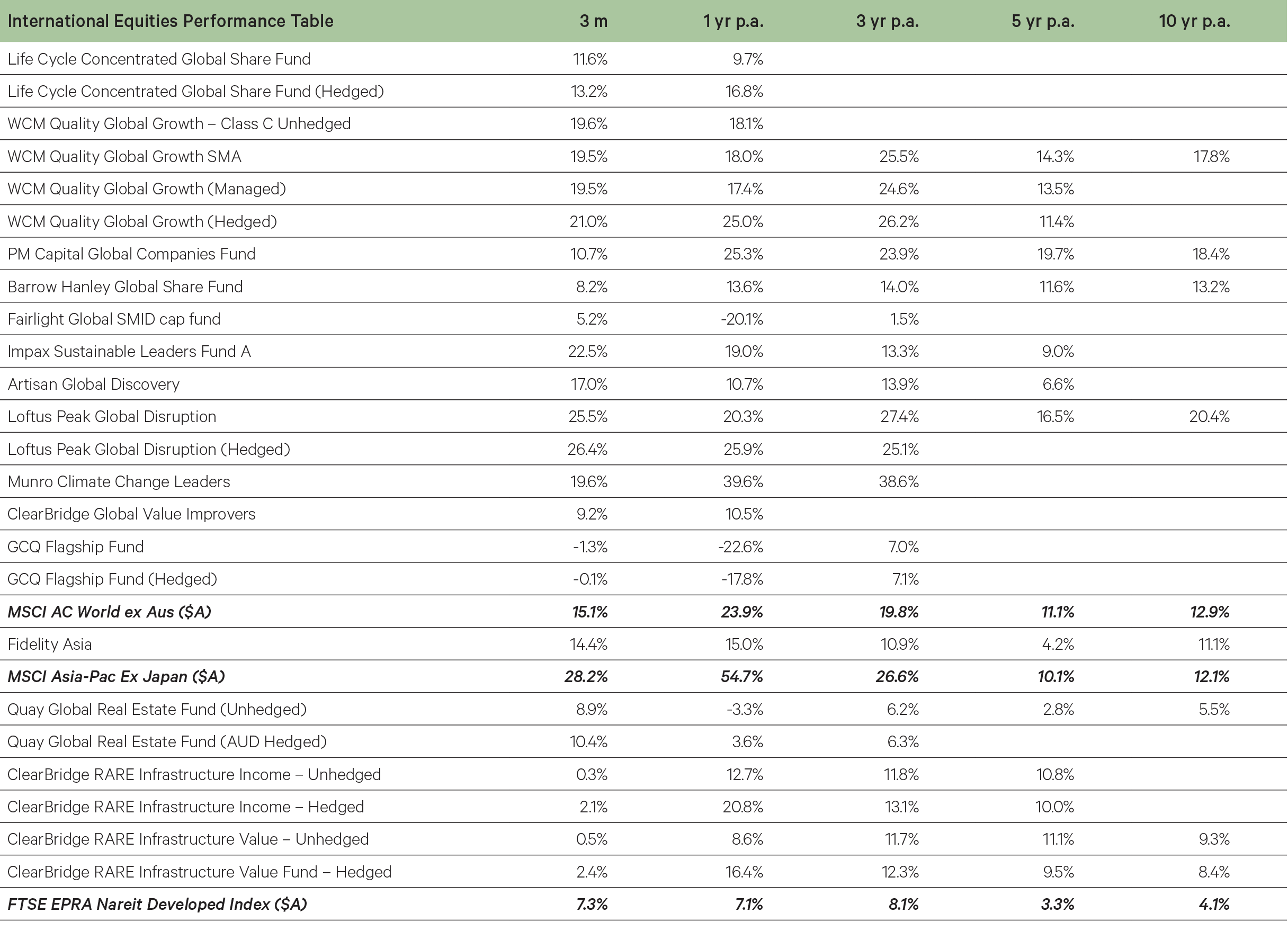

International Equities

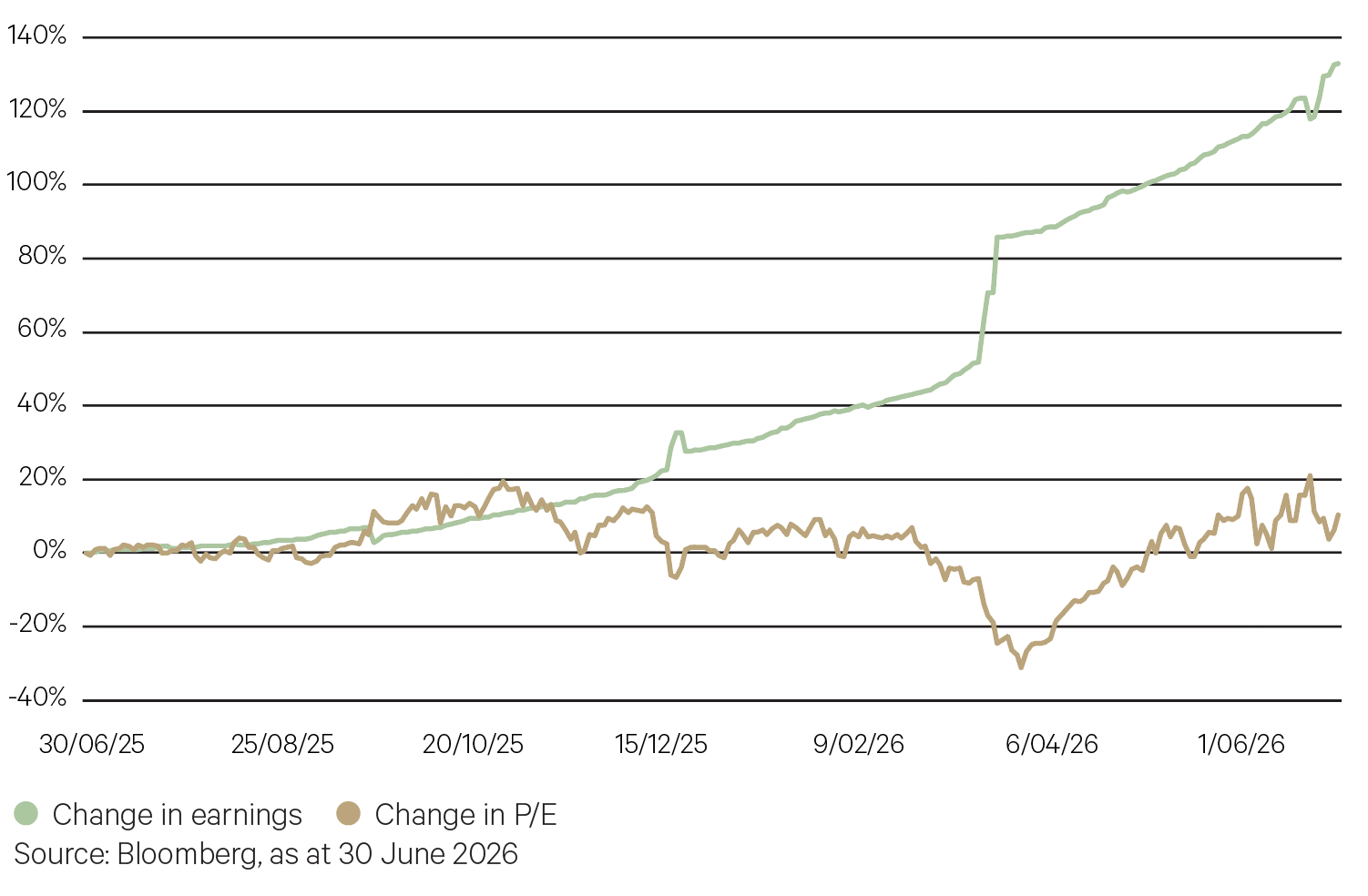

While the AI infrastructure thematic broadened in the June quarter, it was semiconductor stocks in the US that were responsible for powering the US equity market higher over the course of the last 12 months. The PHLX Semiconductor Index represents the 30 largest US-traded companies that are involved in the design, distribution, manufacture and sale of chips and includes such names as Nvidia, TSMC, ASML, Broadcom, AMD, Intel and Micron Technology. Over the past 12 months earnings have more than doubled across this group which now account for close to 20% of the benchmark S&P 500 Index.

Chart 5: PHLX Semiconductor Sector (SOX) driven by escalating earnings

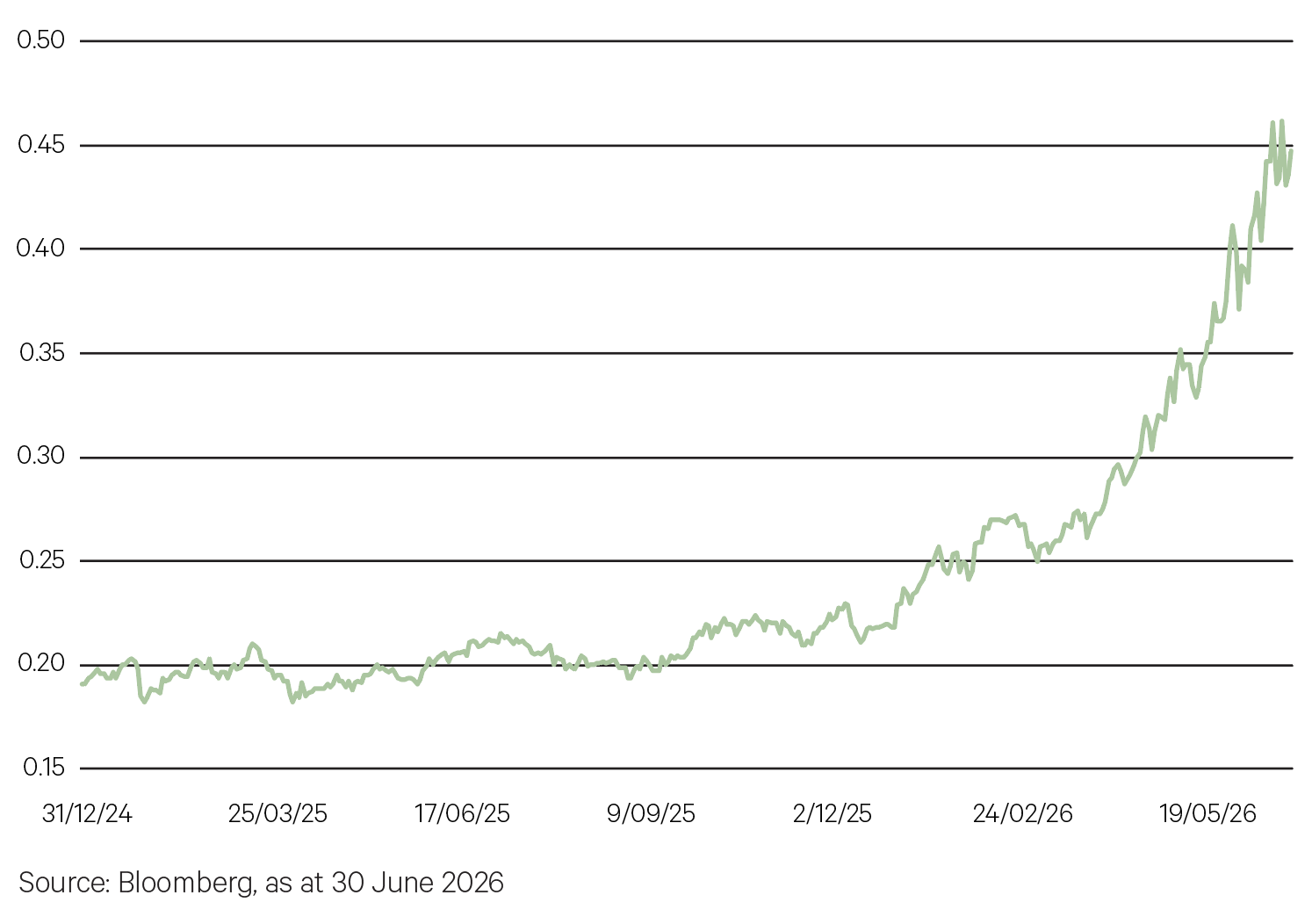

Further illustrating this change in leadership is the relative performance of the SOX index compared with the Mag7 (which includes all of the major cloud hyperscalers). While the hyperscalers continue to commit escalating capital to the datacentre buildout, their equity market returns have slowed as free cash flow dries up and return on investment is challenged. Instead, equity market returns and profits have flowed to semiconductors and other associated hardware – the ‘picks and shovels’ layer of the capital expenditure.

Chart 6: SOX/Mag7 Indices: Equity gains accrue to picks and shovels

Key points

- Global equities rallied in the June quarter, as markets moved back into ‘risk on’ following the initial drawdown from the Iran conflict. Markets were particularly strong across April and May with investors anticipating a ceasefire agreement, before softening somewhat in June. Developed markets gained 13.3% for the quarter while emerging markets rose 23.3%. The Australian dollar weakened towards the end of the quarter, leaving hedged and unhedged returns similar for the three months.

- Index returns masked a narrow rally driven by companies leveraged to AI infrastructure. This was best represented by the extraordinary returns across semiconductors, driving returns not only in the US but in Asian markets such as Taiwan and Korea. Software stocks, which had previously sold off heavily in the March quarter, stabilised, though the gap between hardware and software expanded further.

- Adding to the positive backdrop was another strong quarterly earnings season in the US, with growth out- pacing expectations again and further signs that growth was broadening beyond the technology sector.

- Emerging markets, which had sold off more heavily on the Iran conflict, rebounded to a greater degree over the quarter as the oil price receded along with gains made in AI-related stocks. Japan also built on momentum from early in the year on fiscal stimulus and a weaker yen.

- Overall, growth outpaced value by a wide margin, and cyclical industries and stocks outperformed defensives. This was similarly reflected in our fund returns.

- Loftus Peak was the standout performer for the quarter and is most exposed to the AI infrastructure rally among our large-cap strategies. Munro Climate’s performance was similarly driven by the broadening of AI infrastructure winners.

- Other growth-oriented funds also performed well, including WCM and Artisan Global Discovery.

- Value strategies in Barrow Hanley and PM Capital Global Companies lagged the growth-led rally, though again produced consistent returns across the quarter, while defensive strategies, including Clearbridge RARE Infrastructure similarly underperformed. GCQ’s lack of exposure to the AI infrastructure theme also led to it posting disappointing performance for the quarter.

-

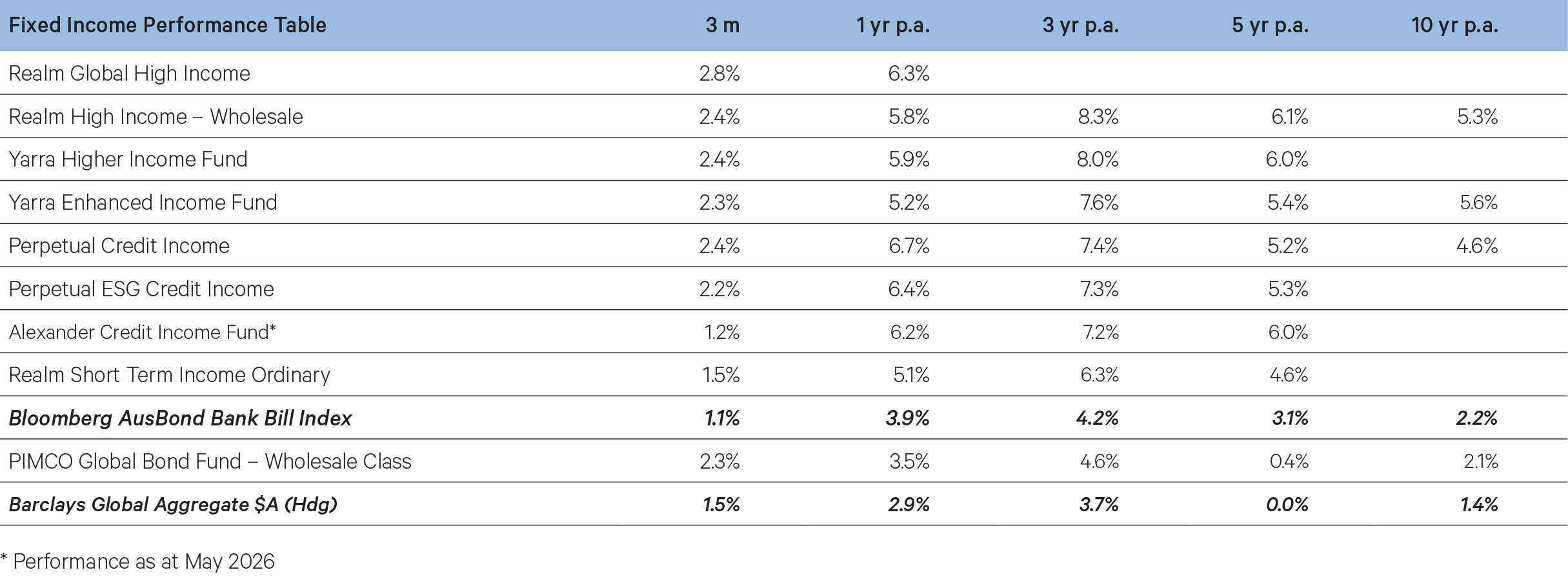

Fixed Income

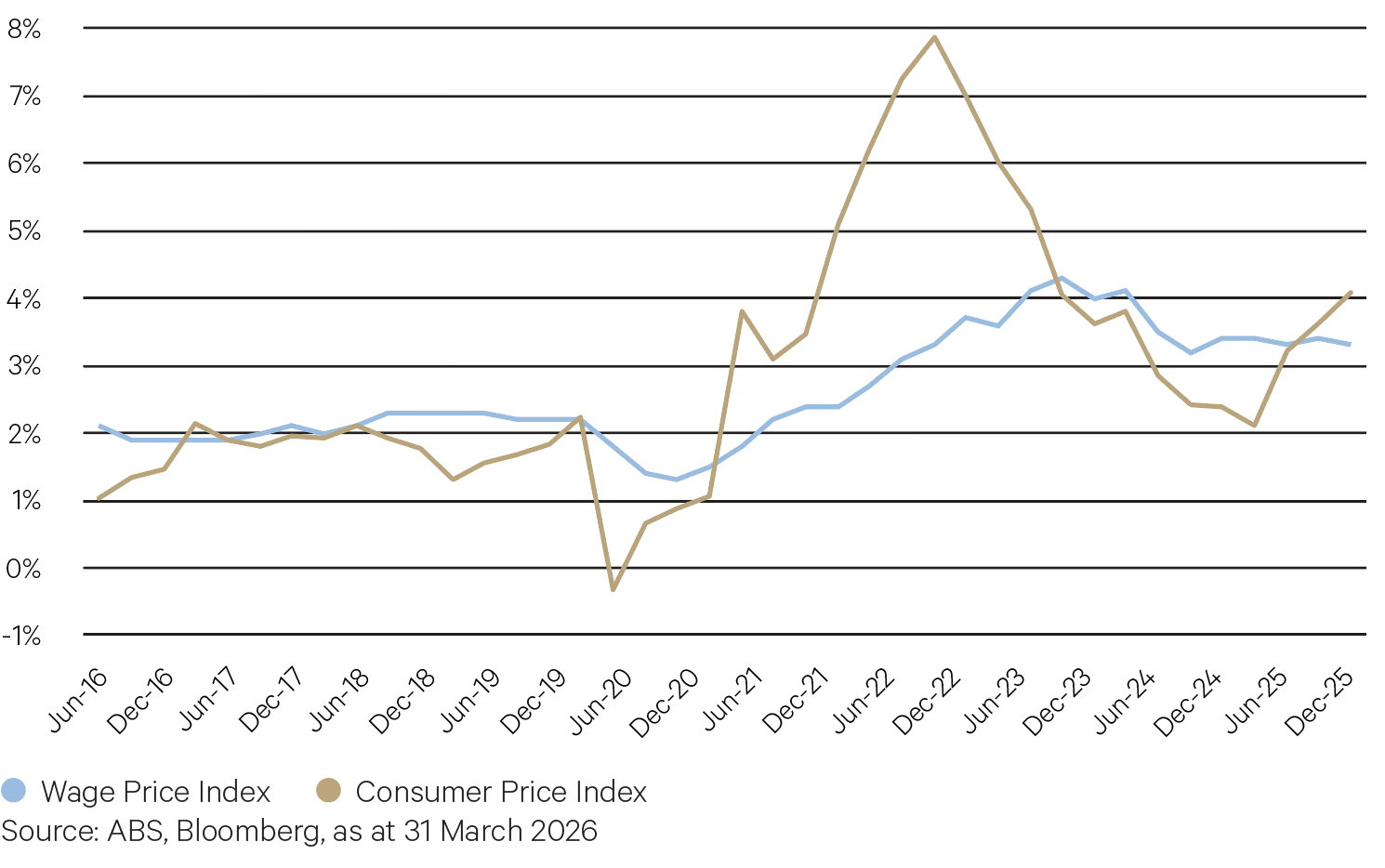

Over the past decade, wages in Australia have grown by around 30%, while consumer prices have increased by approximately 35%. As a result, wage growth has generally lagged inflation, contributing to ongoing cost-of-living pressures for households. The Fair Work Commission’s decision to increase modern award wages by 4.75% from 1 July should provide some relief for lower-income workers and may help narrow the gap between wages and prices. However, there are concerns that stronger wage outcomes could place upward pressure on inflation if businesses respond to higher labour costs by lifting prices, particularly in labour-intensive sectors.

Chart 7: Wage growth lags CPI over the decade

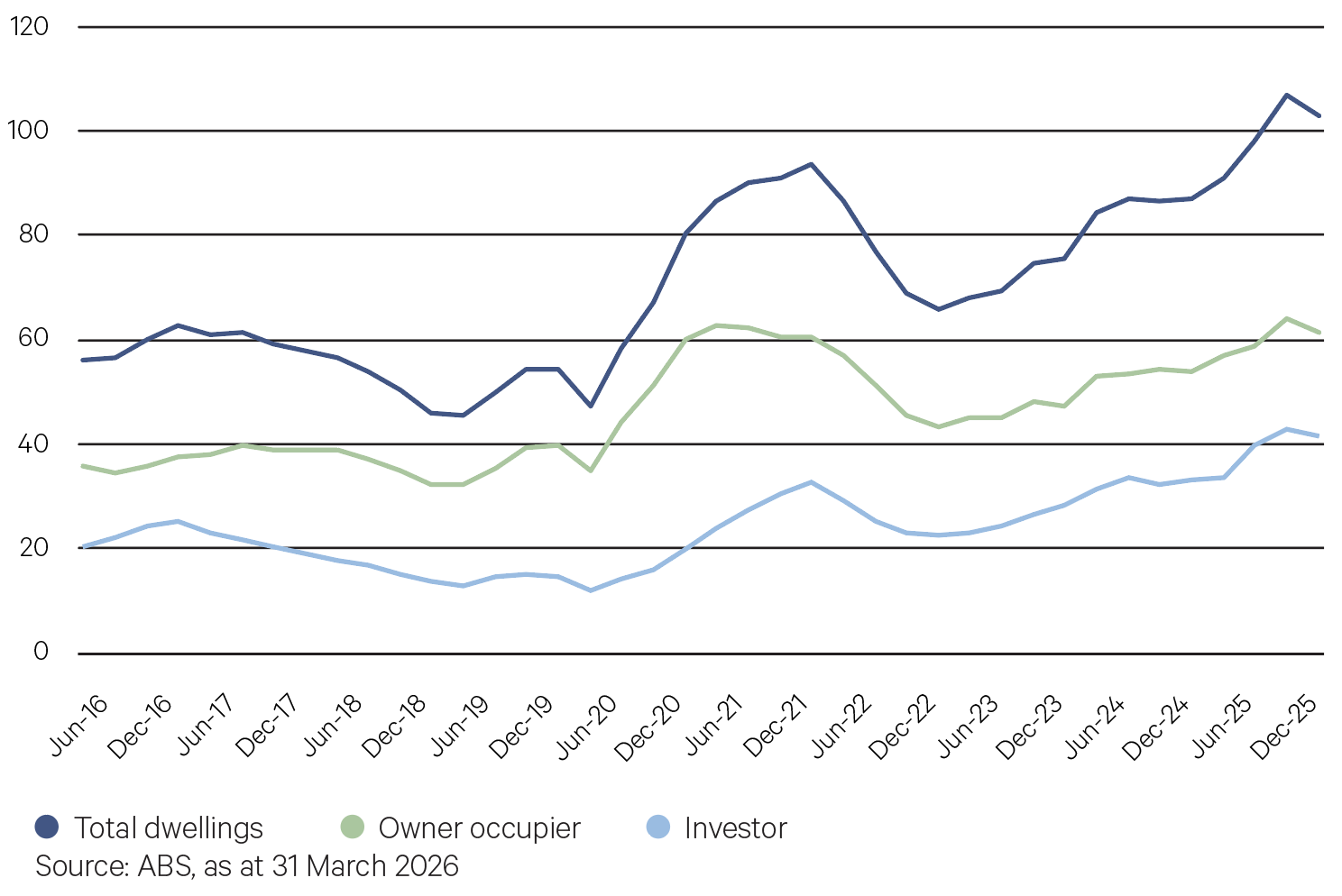

Demand for housing credit has remained strong in the post-COVID period, supported by population growth, rising housing prices and limited supply, although lending activity softened during the March quarter on a seasonally adjusted basis. Looking ahead, proposed changes to negative gearing are expected to tighten financial conditions by reducing the attractiveness of leveraged property investment and curbing investor demand for credit. This should contribute to slower housing credit growth and a moderation in housing market activity, removing an important source of momentum from the residential lending market.

Chart 8: New housing loans continue to grow ($b, seasonally adjusted)

Key points

- The June quarter provided some relief for fixed income investors after March’s challenging conditions. The de-escalation of the Middle East conflict reduced some of the uncertainty surrounding global inflation, although earlier increases in oil prices and supply chain disruptions may continue to filter through to consumer prices over coming quarters.

- Domestically, the RBA delivered a third rate hike, reversing all of 2025’s rate cuts in response to signs that inflation had been reaccelerating before the oil shock began. However, a softer May CPI reading and an unexpected rise in unemployment eased concerns about further tightening this year. Australian government bond yields subsequently declined as markets pared back expectations for additional rate hikes, providing a tailwind for funds with interest rate exposure.

- Globally, inflation pressures remained elevated despite the easing in geopolitical tensions. New Federal Reserve Chair Kevin Warsh began his tenure signalling a shift away from extensive forward guidance, while ongoing inflation driven by oil prices, AI-related investment demand, and tariffs limited the Fed’s flexibility. Markets increasingly questioned whether the next move in US rates may ultimately need to be higher rather than lower.

- The shift towards tighter monetary policy broadened during the quarter. The European Central Bank resumed rate hikes as higher energy costs continued to pressure inflation, while the Bank of Japan raised rates again amid persistent inflation and ongoing weakness in the yen. Loose fiscal policy and rising government debt levels in Japan remain a concern, increasing the risk that monetary policy will need to do more of the heavy lifting to contain price pressures.

- The Federal Budget’s housing tax reforms have the potential to cool investor demand for residential property. While softer housing conditions may create headwinds for activity, mortgage-backed securities continue to benefit from diversification across large pools of loans and structural credit enhancements designed to absorb losses, supporting the resilience of these assets.

- Credit markets recovered strongly from March’s volatility. Credit spreads tightened further as investors remained attracted by elevated running yields and an improving risk backdrop. This spread compression provided a capital uplift for many credit strategies and supported a recovery in funds that had been impacted by widening spreads earlier in the year.

- Falling Australian bond yields were particularly beneficial for funds with interest rate exposure. Yarra Enhanced Income and Yarra Higher Income both benefited from declining yields over the quarter, with duration contributing positively to returns after acting as a headwind in March. Elevated income levels remain the primary driver of returns, providing investors with a meaningful buffer against periods of market volatility.

-

Alternatives

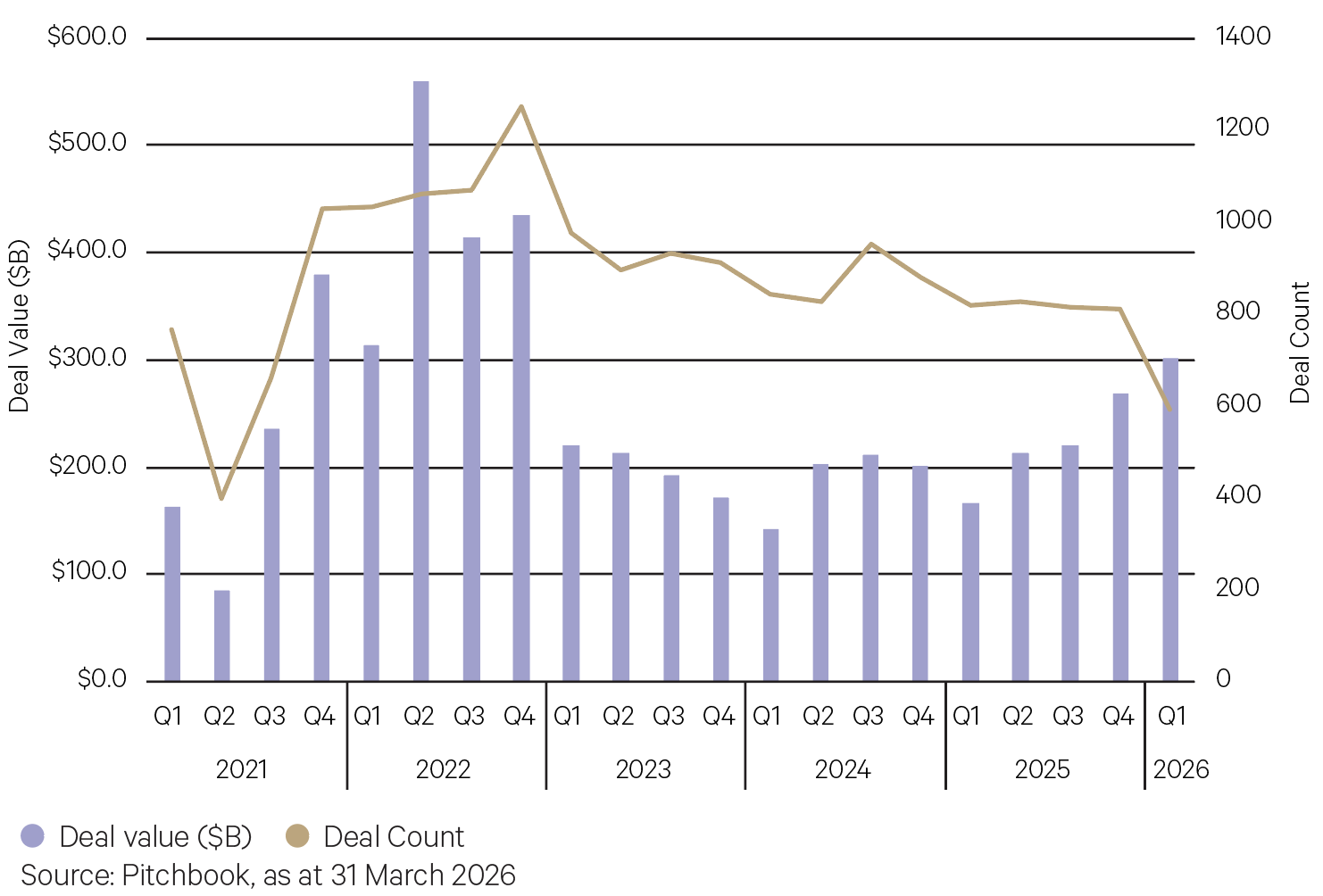

Private equity investment in the aerospace and defence sector remains robust, underpinned by heightened geopolitical uncertainty and sustained increases in military spending worldwide. Europe is becoming an increasingly important source of sector growth, as governments across the region commit to significantly higher defence expenditure. Recent policy initiatives highlight this trend, including Germany’s decision to exempt defence spending from its constitutional debt restrictions, the UK’s commitment to increase defence spending, and France’s ongoing expansion of military procurement under its multiyear defence program.

Chart 9: Aerospace & defence PE deal activity by quarter

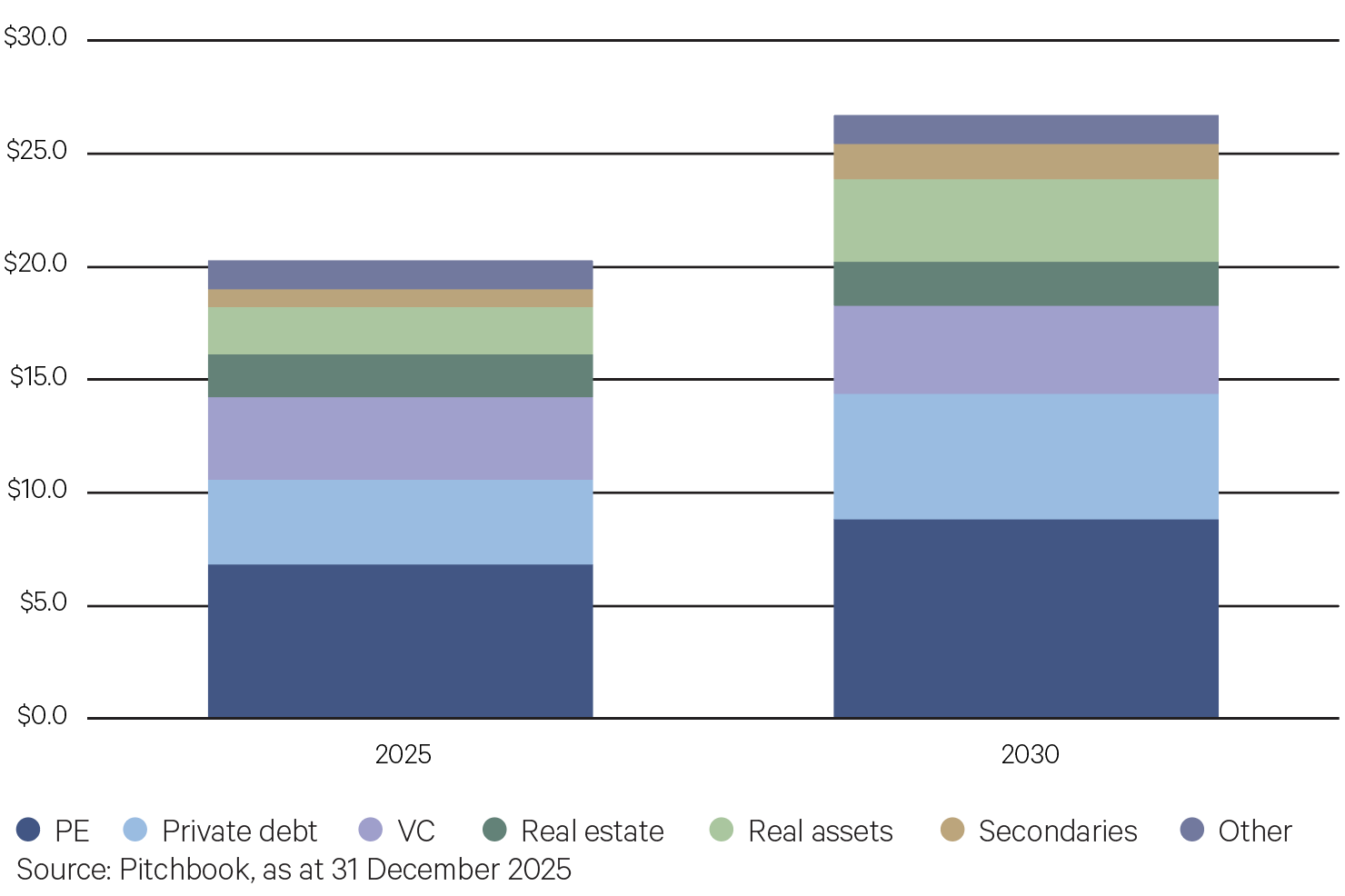

Pitchbook forecasts private market assets under management managed by General Partners (GPs) to expand significantly over the remainder of the decade, increasing from around $20 trillion today to approximately $26.7 trillion by 2030. Growth is expected to be supported by a broader range of investors, increased participation from private wealth channels, and the continued evolution of investment structures. A notable trend shaping the market is the growing adoption of evergreen strategies, which are making private markets more accessible. Among private market segments, real assets are anticipated to see the strongest growth, benefiting from long-term investment themes such as energy security, digital infrastructure development, and supply chain resilience.

Chart 10: Private Capital AUM Forecast ($T) by fund strategy

Key points

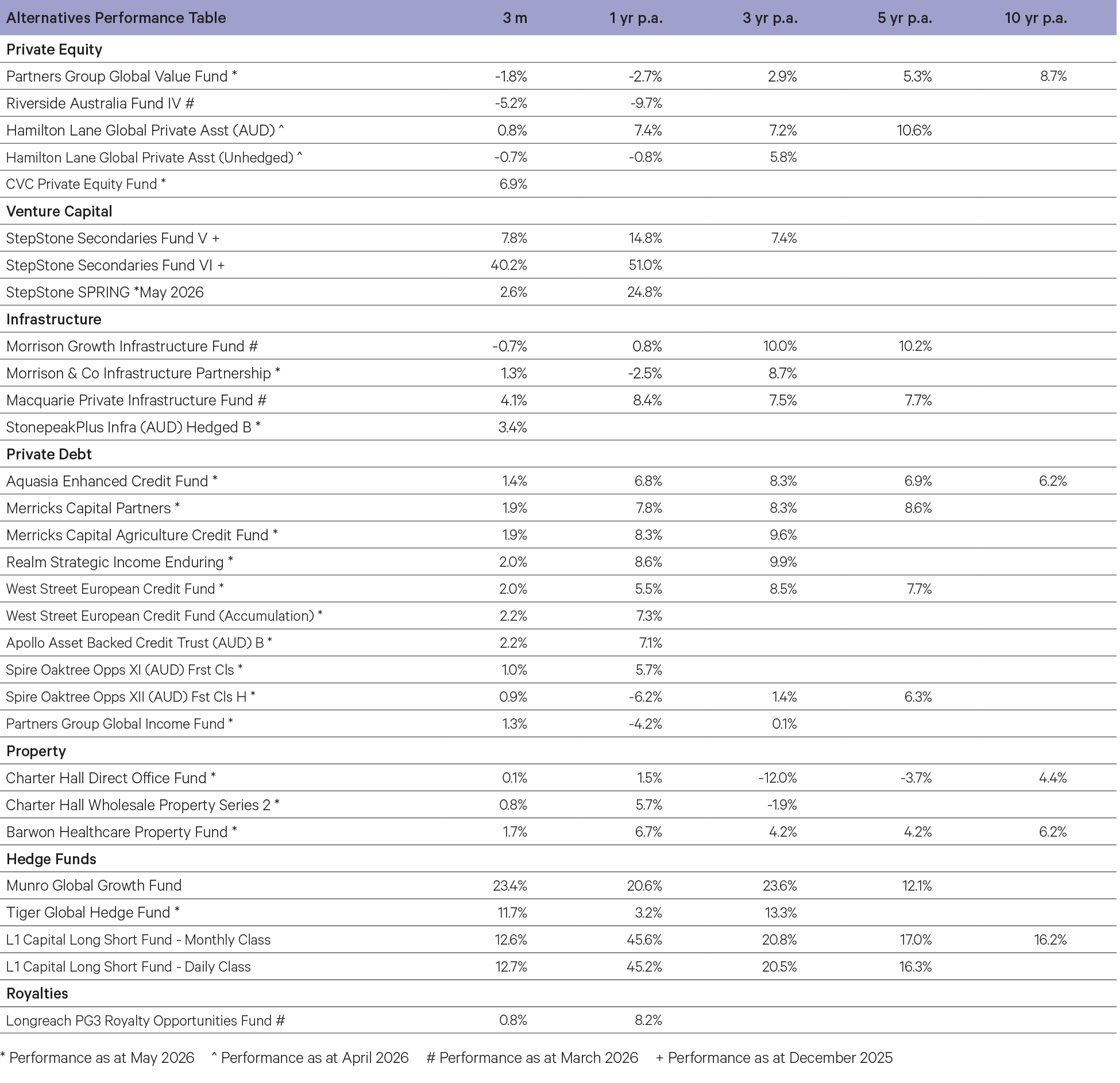

Private Equity

- CVC Private Equity Fund returned +6.9% for the three months ending May 2026. Across the period, returns were well-diversified across sectors, driven by strong earnings growth and value creation. Notable drivers of performance have come from positions in Dream Games, Bamboo Insurance, M Group (all have benefitted from improved earnings and a reduction in net debt) and Project Selene (LP-led secondary).

- Hamilton Lane Private Assets Fund (Unhedged) returned -0.66% for the three months ending April 2026. The depreciation of the US dollar against the Australian dollar had a negative impact on performance across the period. The underlying portfolio delivered positive returns throughout the period, driven by gains in secondaries and co-investments. Bad Boy Mowers, a leading manufacturer of commercial lawn mowers and accessories that Hamilton Lane invested in alongside TorQuest Partners in 2023, was a top contributor during the period, supported by strong operating momentum, healthy revenue growth, and EBITDA generation tracking ahead of budget.

Private Debt- West Street European Private Credit Fund returned +2.2% for the three months ending May 2026. Underlying loan income was strong during the period, with the fund predominantly invested in directly originated, floating-rate first lien loans. The portfolio spans eleven sub-sectors across twelve countries. During the period, major new positions were established in Janes, a leading provider of open-source intelligence on military equipment, and Global Gruppe, a leading insurance broker across the DACH region (Germany, Austria, and Switzerland).

- Partners Group Global Income Fund returned +2.5% for the three months ending May 2026. Performance was driven mainly by recovery in secondary market prices. Positions in software, materials, and health care were the leading contributors. During the period, the fund increased direct credit exposure through investments in a U.S.-based legal services platform. In syndicated credit, the fund invested in a U.S.-based producer of resins and surface overlay products, as well as a packaging solutions provider focused on food safety.

- Merricks Partners added +1.9% for the three months ending May 2026. During the period, the fund received full repayment across several commercial real estate facilities.

This included the full repayment of a Williamstown residential construction facility following completion of its staged townhouse development. The fund also reached contractual close on a senior project finance facility for the Sorby Hills silver-lead project in Western Australia. The fund remains fully deployed and diversified across real estate, agriculture, infrastructure, and resources sectors.

Hedge Funds- L1 Capital Long Short returned +12.7% (Daily class) for the three months ending June 2026. Portfolio performance was strong, supported by materials, industrials and copper stocks. Key positive contributors across the period included Mineral Resources, James Hardie, Goodman Group and Qantas.

- Equity long short manager Munro Global Growth returned +23.4% for the three months ending June 2026. During the period, strong earnings from companies exposed to the AI capex buildout benefitted the fund. Key contributors across the quarter included Micron Technology, ARM Holdings, Applied Materials, ASML, TSMC, and GE Vernova.

- Tiger Global Investors returned +11.7% for the three months ending May 2026. Gains were driven by the fund’s long book including positions in Broadcom, Lam Research, Amazon, Alphabet and TSMC.

Venture Capital-

StepStone Private Venture and Growth Fund (SPRING) added +2.6% for the three months ending May 2026. Performance was driven principally by valuation increases related to GP marks and fundraising rounds. During the period, Cyera, a leading AI-native data security platform, raised US$600 million at a US$12 billion valuation. The company has been one of the standout beneficiaries of accelerating enterprise AI adoption, with its valuation increasing from US$1.4 billion in 2024 to US$12 billion in just over two years as organisations invest heavily in securing data and AI workloads.

Infrastructure-

The Macquarie Private Infrastructure fund returned +4.1% over the March quarter. During the quarter, the fund benefited from positive performance across the majority of its investments, with notable positive performance for a number of the recent co-investment positions including Diamond Infrastructure Solutions (U.S.), VIRTUS Data Centres (U.K.) and Southern Water (U.K.). The fund’s listed infrastructure holdings were also a strong positive contributor, and the FX hedging program also insulated the fund from broader FX volatility during the quarter.