-

Q4 in review –

Out of Sync

Q4 2025 capped a year characterised by fragmentation rather than synchronisation. As the year drew to a close, central banks moved more out of step with policy easing in some economies, policy pauses in others and outright tightening in Japan. Equity markets reflected this divergence, with leadership broadening beyond the US large cap tech stocks into areas shaped by country-specific policy priorities, including re-industrialisation and supply-chain resilience. Against this backdrop, investors navigated elevated policy uncertainty, geopolitical risk and late-cycle dynamics, underscoring the importance of active allocation and selectivity when choosing where to invest.

1. Dissent and Divergence

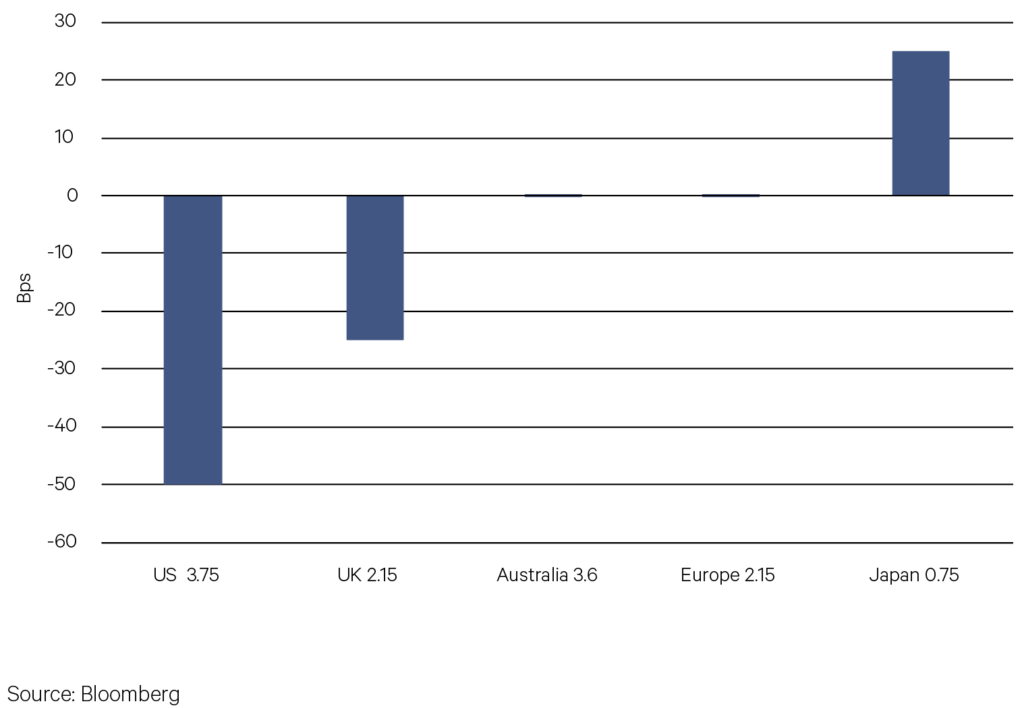

Across major economies, Q4 2025 was characterised by a widening of the divergence in central bank policy alongside growing internal dissent in some jurisdictions. The most contested decisions were in the US and UK, where monetary policy was eased further amid slowing job growth in the US and softer inflation alongside weakening economic momentum in the UK. By contrast, Canada’s rate cut was unanimous, reflecting a clearer consensus around deteriorating growth and trade-related headwinds.

In Europe and Australia, policy was left unchanged, with central banks pointing to inflation dynamics and labour-market conditions that did not yet justify additional easing. Japan stood apart as the only major economy to tighten policy during the quarter, reflecting persistent wage growth and inflation pressures. Taken together, Q4 underscored that monetary policy paths were no longer globally synchronised leaving the UK with the lowest interest rates in almost three years and Japan with the highest in 30 years. All of this elevates the importance of country allocation for investors in 2026.

Chart 1: Change in interest rates over Q4 (current official rate below (%)

2. Dysfunction

US fiscal and political dysfunction resurfaced as a market risk in Q4. The prolonged US government shutdown and ongoing deficit concerns lifted risk premia and reinforced demand for assets perceived as independent of sovereign balance sheets.

As the US dollar softened, gold benefited, but silver amplified the move due to lighter positioning and a lower starting valuation. Crucially, silver also gained from its industrial demand exposure – particularly expectations of improving manufacturing activity and ongoing demand from solar, electronics, and electrification. Gold is driven almost entirely by monetary and safe-haven flows.

Chart 2: Gold and silver price (Index 01/01/2025=100)

3. Dispersion

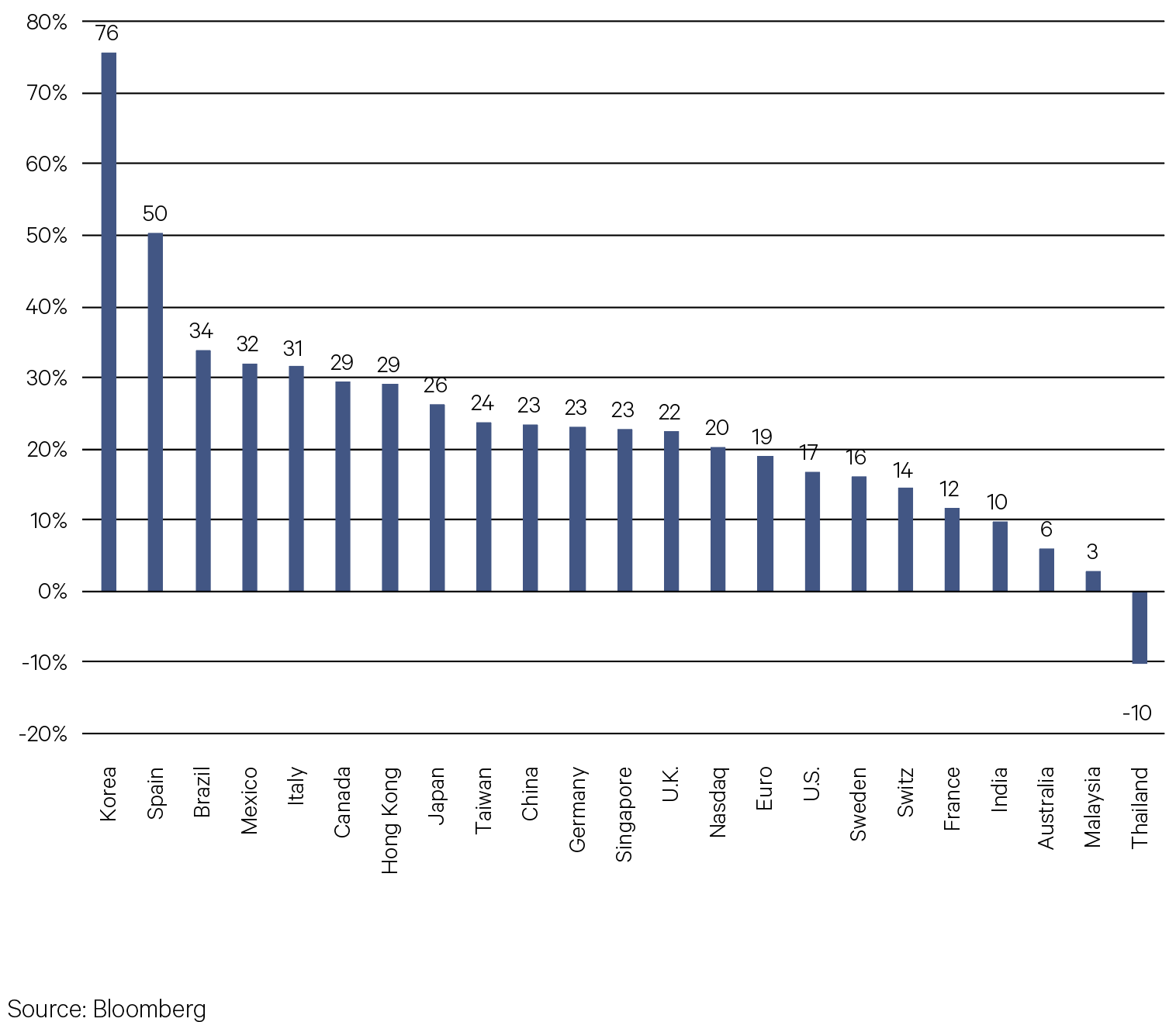

Return dispersion in 2025 reached its widest level since 2006, highlighting a market driven by structural and national differentiation rather than broad global factors.

Performance diverged sharply even within regions, with Korean equities up 76%, supported by a powerful semiconductor and AI-related earnings recovery and reinforced by targeted fiscal stimulus, including government support for technology investment, manufacturing capacity, and household income. In contrast, Thailand fell 10%, weighed down by weaker domestic growth, tourism sensitivity, and limited exposure to global technology cycles.

The scale of this divergence underscored how policy choices, sector composition, trade exposure and earnings leverage dominated returns, reinforcing the importance of active country allocation in 2025.

Chart 3: 2025 returns for the major equity markets (%)

-

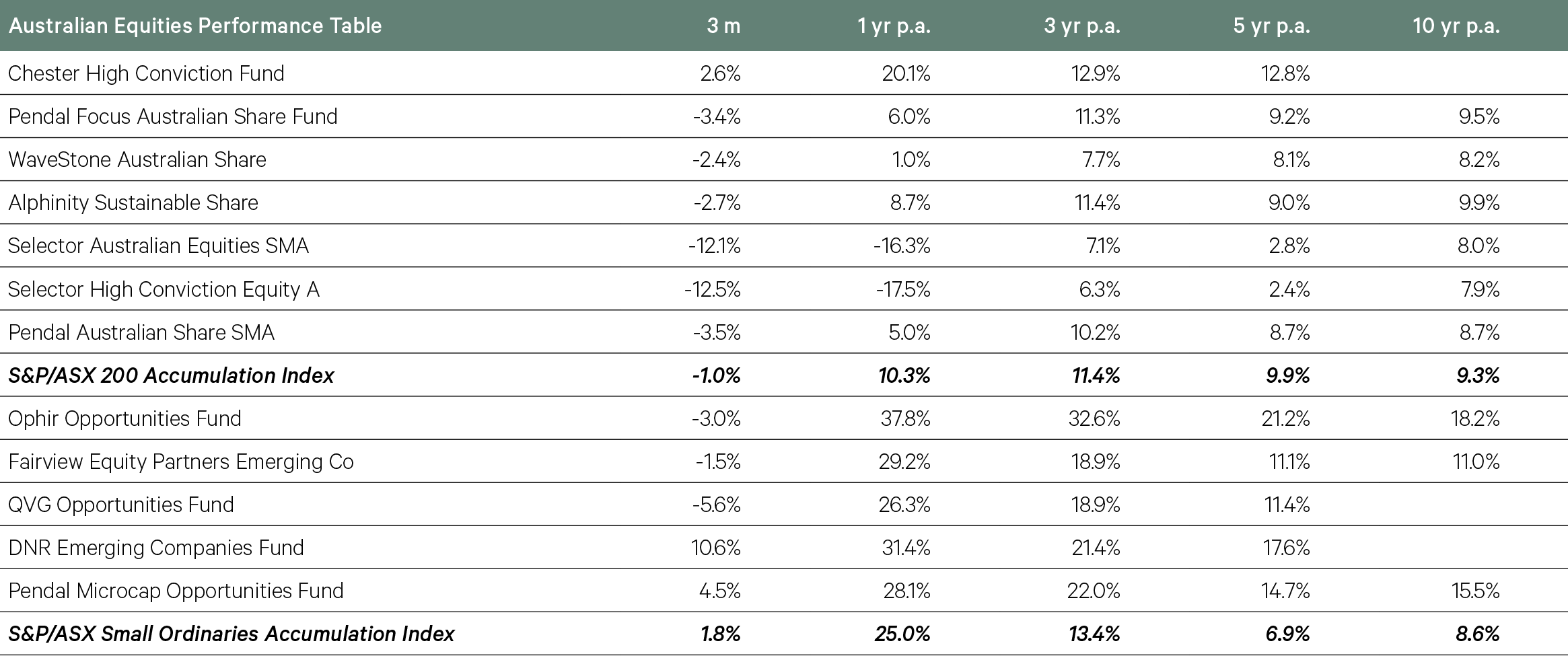

Australian Equities

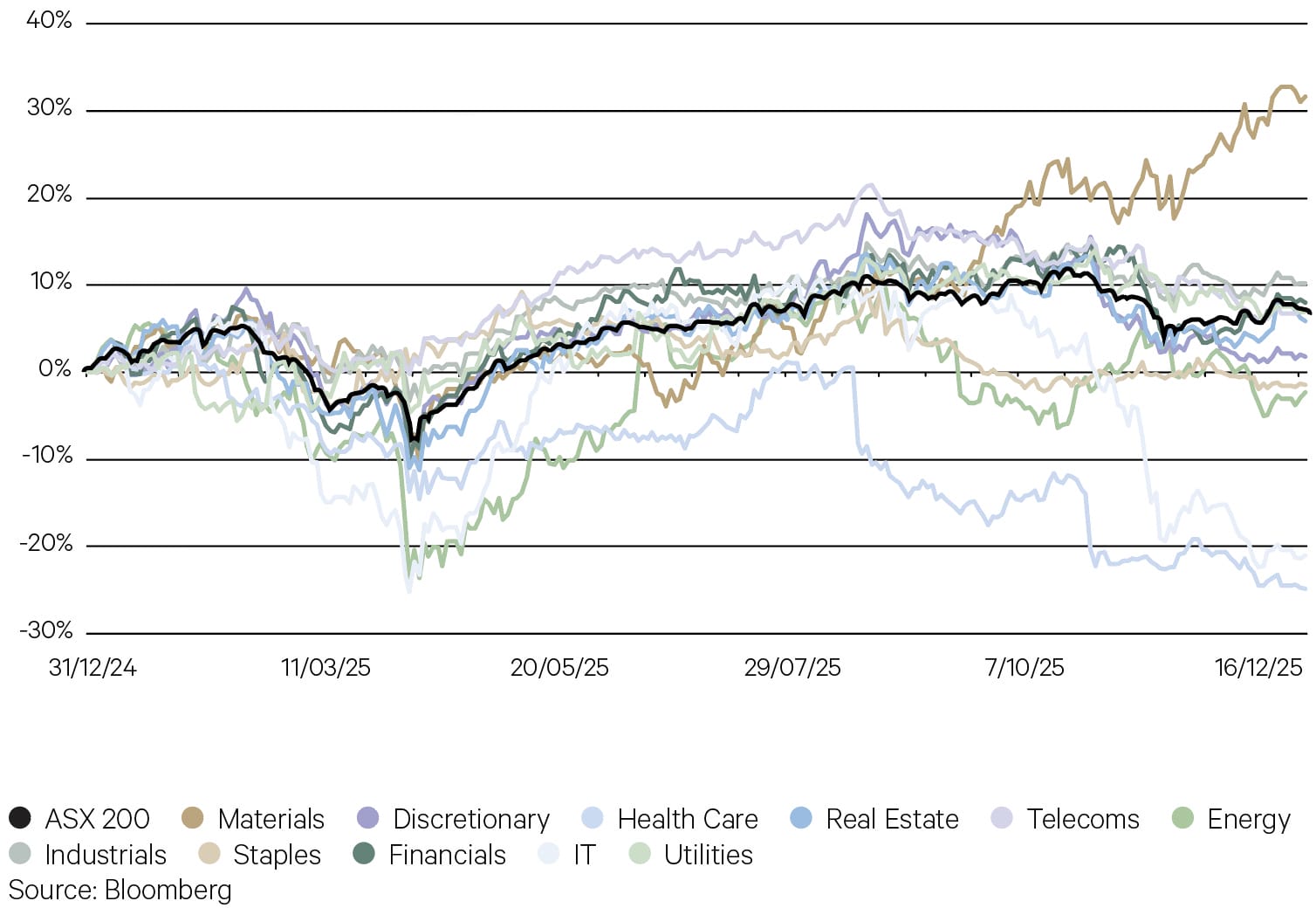

While the ASX 200 eked out a double-digit total return over 2025, there was a wide gap between the best and worst performed sectors for the year. Materials was the standout, driven by record high gold prices and a broadening of gains in commodities in the second half of the year. In contrast, the key growth sectors of health care and IT both fell around 20%, as P/Es on growth stocks suffered a derate late in the year.

Chart 4: Wide sector dispersion in the Australian market in 2025

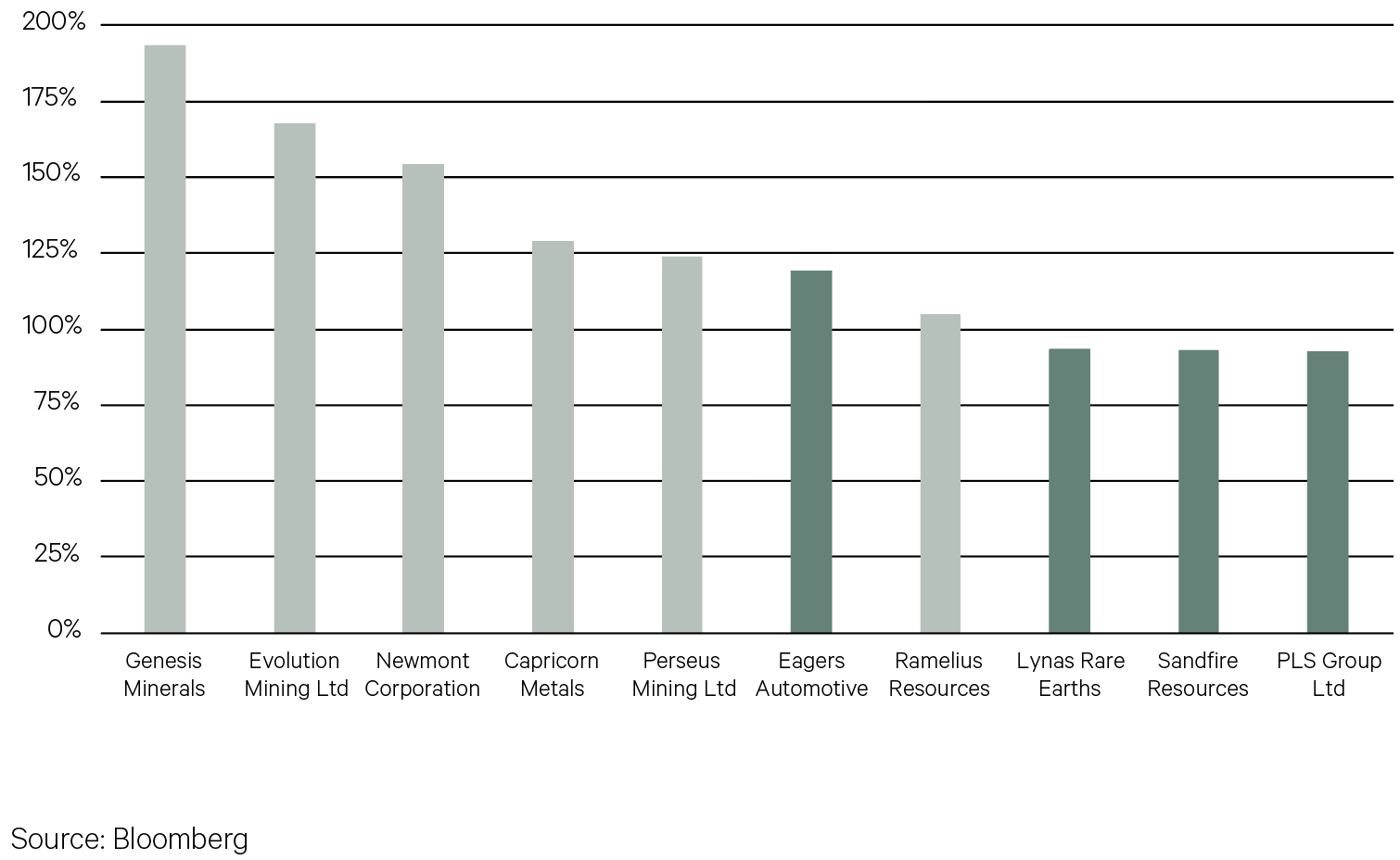

Underscoring the strength of the gold sector in 2025, the top 5 performing stocks (and 6 of the top 10) in the ASX 100 were all gold mining companies. All up, resource stocks comprised 9 of the top 10, with Eagers Automotive the lone industrial company among top performers.

Chart 5: Gold stocks shine in 2025

Key Points

-

The Australian equity market edged lower in the final quarter of 2025, losing 1% and underperforming international equity markets. After tracking or outperforming many overseas markets for much of 2025, the Australian market lost momentum in a relative sense over the second half of the calendar year.

-

The composition of the market’s returns revealed an exceptionally high level of dispersion across the different sectors of the market and the narrowness of market leadership, extending the trend of the prior quarter.

-

The resources sector underpinned the returns of the benchmark, gaining 10.6% for the quarter. While the gold sector continued to extend its exceptional rise, miners across base metals, iron ore and lithium added to a strong thematic for the half; the latter rebounded sharply off the prior drawdown experienced across the industry.

-

In comparison, industrial stocks were much weaker. This was particularly evident in the higher growth sectors of the domestic market, such as IT, health care and consumer discretionary. In a number of cases, these were driven by trading updates or results that were somewhat weaker than expected, though the market reaction to several of these was more driven by a more significant valuation de-rate.

-

A pause in the ‘AI trade’ during the quarter also provided a challenging backdrop for the IT sector. The Australian IT sector, while small in nature, is largely comprised of software companies. In 2025, these were sold off across the board, primarily on fears that AI will disrupt rather than augment their business models.

-

The macroeconomic environment also added a further headwind for the growth sectors of the Australian market. With recent inflation prints trending higher again, this triggered a recasting of expectations for monetary policy for the year ahead, a point recognised by the RBA. After three 25bp cuts to the cash rate over the course of 2025, the consensus view is that we have reached the end of the easing cycle domestically and will possibly see one or two hikes in 2026. Bond yields rose sharply from mid-October, climbing around 70bp.

-

Among our large and mid cap managers, the relative performance of funds was primarily driven by their relative weightings across these two segments of the market – resources and growth stocks. The Chester High Conviction Fund was thus a standout, lifted by gold and broader resources exposure, while supported by a more value-oriented approach in industrials. Selector was the clear laggard, with the fund’s portfolio largely comprised of the sectors of the market that have come under the most pressure.

-

Small caps outperformed large caps in the December quarter. Fund performance was similarly driven by the themes outlined above and momentum faltered across many of the significant industrials winners of the first half of the year.

-

DNR Capital’s rotation back into the resources sector in the second quarter of 2025 paid off materially, leading to outperformance of almost 10% for the quarter. This lack of resources similarly led to a drag on the returns from QVG.

-

-

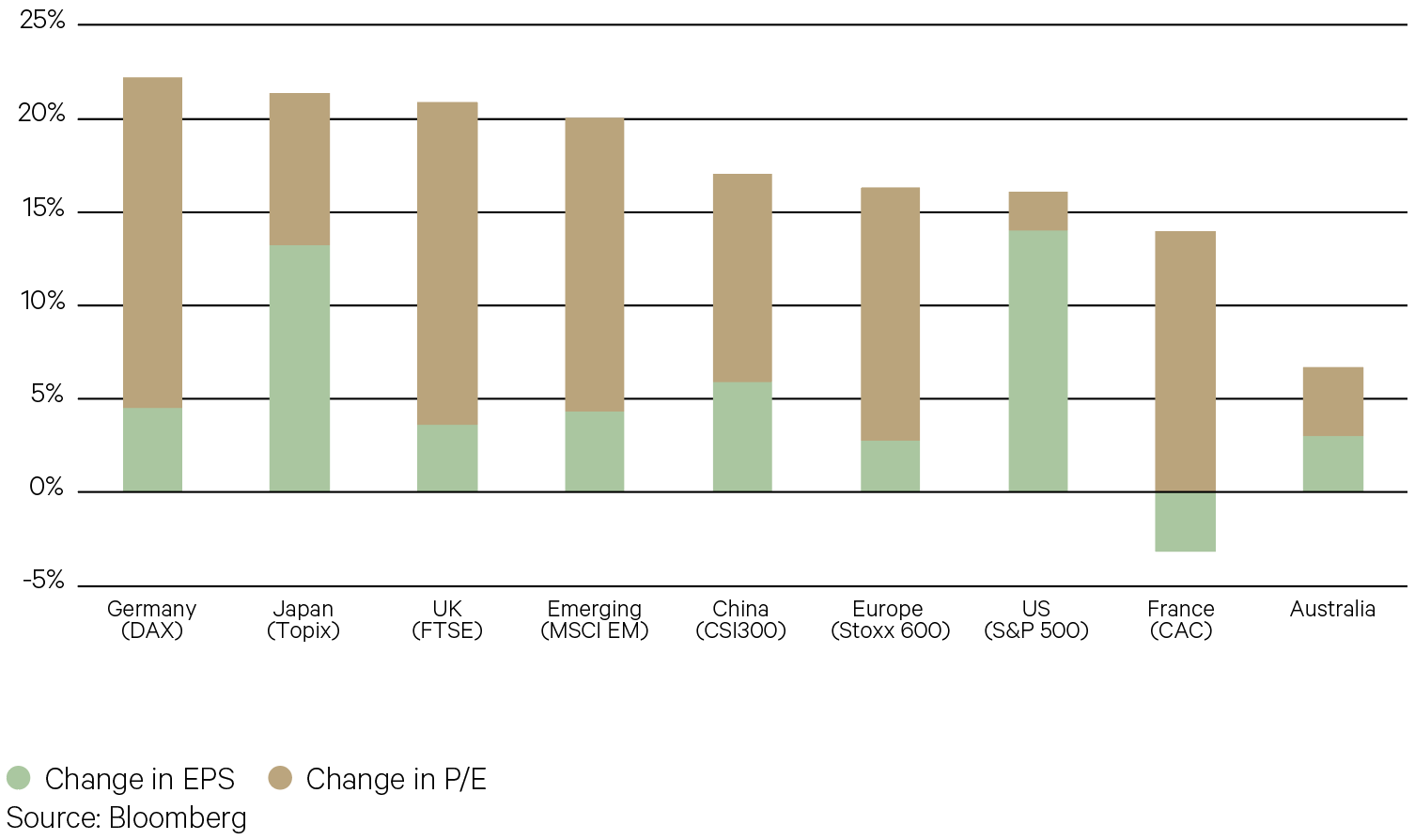

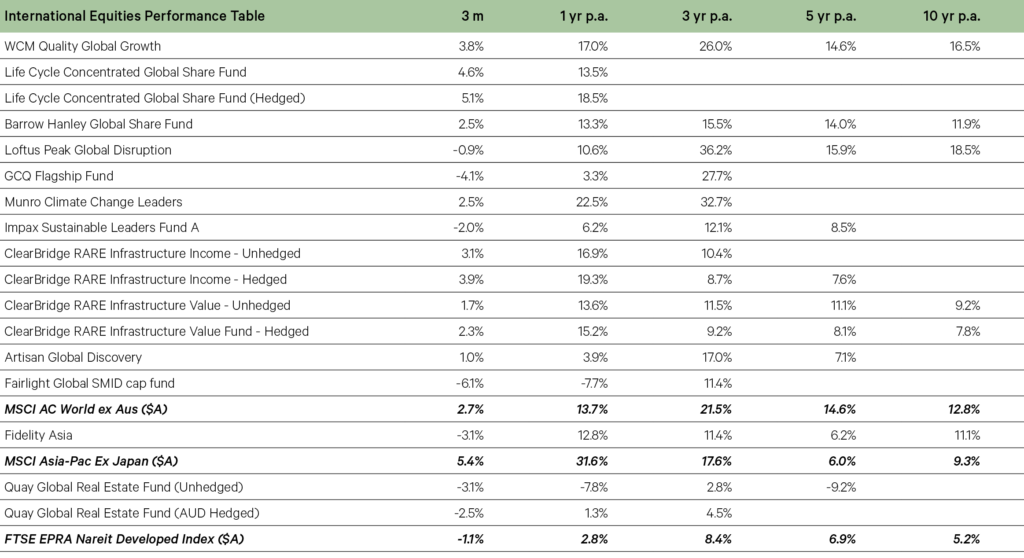

International Equities

Equity returns were strong across 2025, with a mix of earnings and P/E expansion driving returns through a volatile 12 month period. Among the leaders were Germany and Japan, while the US was a surprising laggard. While the US had superior earnings growth to most markets, valuation expansion was much more modest overall, as others reduced the valuation gap.

Chart 6: Earnings and P/Es expand in 2025

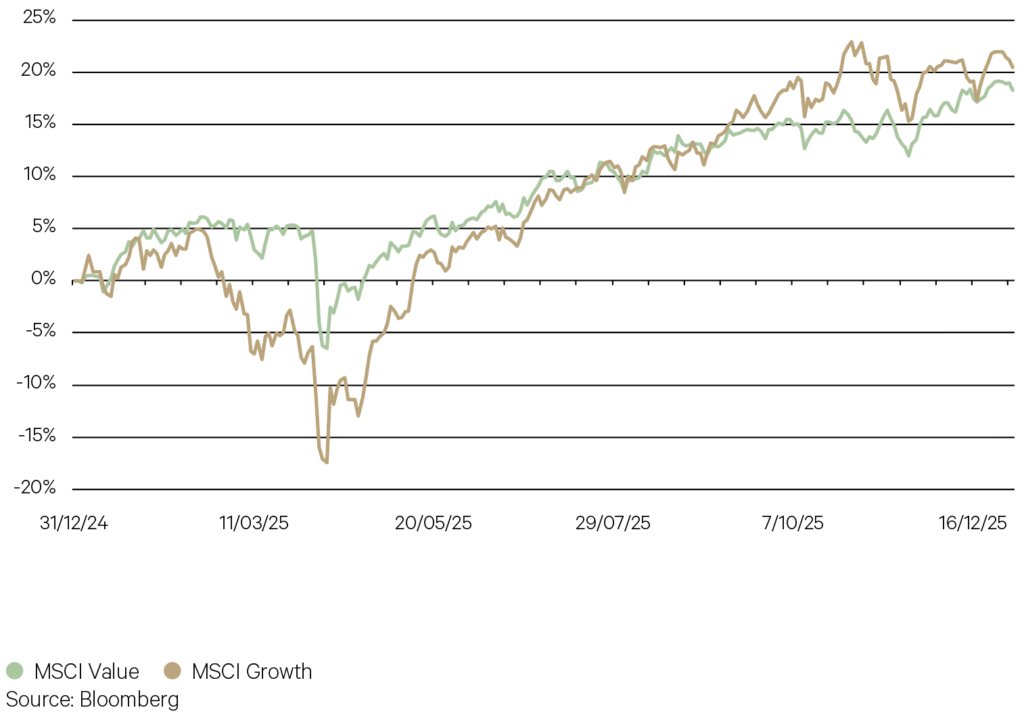

For the third year in a row, growth equities outperformed value equities, though the difference over the 12 months was marginal. Growth equities lagged in the early part of the year as investors became relatively more optimistic on Europe and concerns around AI were raised following the release of DeepSeek. While all markets suffered a drawdown following Liberation Day, technology shares again led the sharp recovery over the following months before tapering towards the end of the year.

Chart 7: Growth slightly outpaces value in 2025

Key points

-

Global equities closed out the year on a positive note, with gains of 2.9% for developed markets and 4.3% for emerging markets for the December quarter. While the post-Liberation Day recovery continued, the gains occurred amidst another pick up in volatility, particularly across October and November.

-

A six week government shutdown in the US added to an uncertain environment across October to mid-November, creating a data vacuum that made it challenging for investors to get a read on the US economy.

-

This also clouded monetary policy decisions, though the Fed followed its September rate cut with a further 25bp reduction at the central bank’s October meeting. Despite cutting rates for a third successive meeting in December, a more hawkish tone was again adopted by the Fed with mixed signals on inflation, the labour market and the broader economy.

-

Over the quarter, returns were more mixed across the large technology names, as several criticisms of the key stocks underpinning the AI thematic came into sharper focus, including the increased use of debt to fund the enormous capex of the hyperscalers, the high number of ‘c ircular deals’ being made and the ultimate returns that will be generated by this investment. Alphabet stood out as a relative winner in the quarter on the back of its launch of its Gemini 3 AI model.

-

Elsewhere, a supportive fiscal and monetary policy environment led to strong outperformance of Japanese equities in the quarter, extending the trend over much of 2025. With a further spike in US-driven volatility, European equities also slightly outperformed, while value equities edged out growth.

-

Life Cycle had a solid quarter, with outperformance driven by a mix of stocks of sectors, such as Steel Dynamics (+22%) and Delta Airlines (+22%), both among the portfolio’s largest weights.

-

Funds with more of a value or defensive orientation, such as Barrow Hanley and Clearbridge Infrastructure, again delivered more steady and consistent performance across the quarter, a feature across 2025.

-

Among funds that experienced a more challenging quarter included GCQ and Fairlight. Both of these strategies have been impacted by the decline in stocks that are perceived to be at risk from disruption from new or existing competitors from deploying artificial intelligence. This has been driven by a P/E derating of these companies rather than an observable decline in earnings.

-

After leading the broader market’s returns in the prior quarter, funds with a growth bias had more variable returns in the December quarter amidst a fragmentation in key AI-driven stocks. The softer performance of Loftus Peak and WCM primarily occurred during the pick up in volatility in November.

-

-

Fixed Income

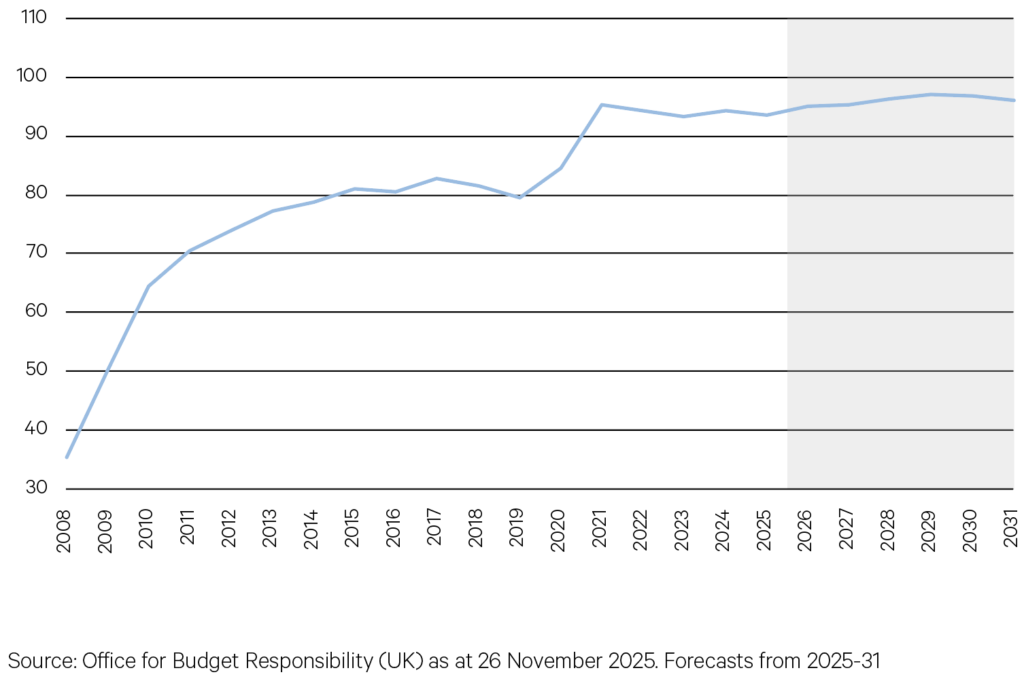

Most advanced economies have scaled back the extraordinary spending undertaken during the pandemic, but their deficits and debt burdens have continued to rise. In contrast, the UK continued to run persistently large deficits amid rising interest rates, low growth, an ageing population, and geopolitical and trade tensions. Facing pressure to meet its own fiscal rules, the government announced broad tax measures in the Spring Budget aimed at containing the growing debt burden. Markets welcomed the announcement, helping avert a potential debt crisis, though it weighed on medium term growth expectations.

Chart 8: UK public sector debt to GDP (%)

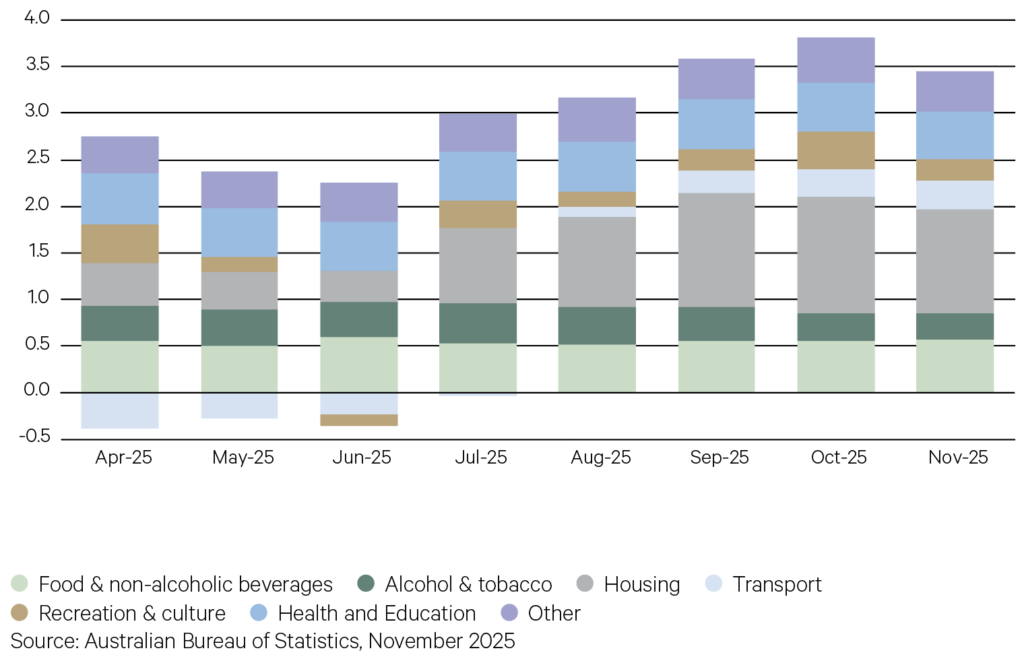

The next move from the RBA now appears more likely to be a hike, as inflation has proved more persistent than expected. October CPI surprised to the upside at 3.8%, well above the central bank’s 2–3% target range. Price pressures were broad based across the CPI basket, with housing costs contributing significantly. Although November data showed some easing to 3.4%, winding back pricing for a hike in the first half of 2026, the RBA’s cutting cycle appears to be over.

Chart 9: CPI groups contribution to annual change (%)

Key points

-

Global fiscal and monetary settings came under scrutiny in the December quarter, with yields adjusting to shifting expectations. The US yield curve steepened as short term rates fell, with two year yields dropping 18 bps on rising expectations of near term cuts. Australian yields rose across the maturity spectrum, with three-year yields up over 50bps and ten-year yields up 44bps. Credit spreads widened temporarily before retracing toward historical lows.

-

Weakness in the US labour market prompted the Fed to deliver an additional 50bps of cuts during the quarter, even as inflation remained firmly above target. Tensions between the central bank and President Trump intensified as Chair Powell’s term approaches its end, and dissent within the FOMC is growing as the path for policy became less certain. A record six-week government shutdown delayed economic data, leaving central banks navigating in the dark.

-

The Bank of Japan raised rates by 25 bps to 0.75%, the highest level in three decades. Inflation, especially in staple food categories, has been running above target for more than three years. A newly elected Prime Minister with a stimulatory fiscal agenda may complicate the BOJ’s tightening efforts, putting further upward pressure on Japanese yields.

-

Concerns over auto lender bankruptcies in the US pushed global credit spreads wider early in the quarter, creating a headwind for credit managers. High prices and limited relative value opportunities remain a challenge for managers looking to generate alpha. Domestic focused strategies underperformed their targets, although attractive running yields helped cushion the effect.

-

Low credit durations supported liquidity funds, which broadly outperformed credit funds over the quarter. Quality assets and high carry kept returns healthy despite some spread volatility in the period.

-

Falling US short-term yields benefited interest rate-sensitive funds, despite rising yields domestically. PIMCO’s tactical curve positioning and emphasis on higher quality assets enabled the fund to outperform its benchmark over the quarter.

-

-

Alternatives

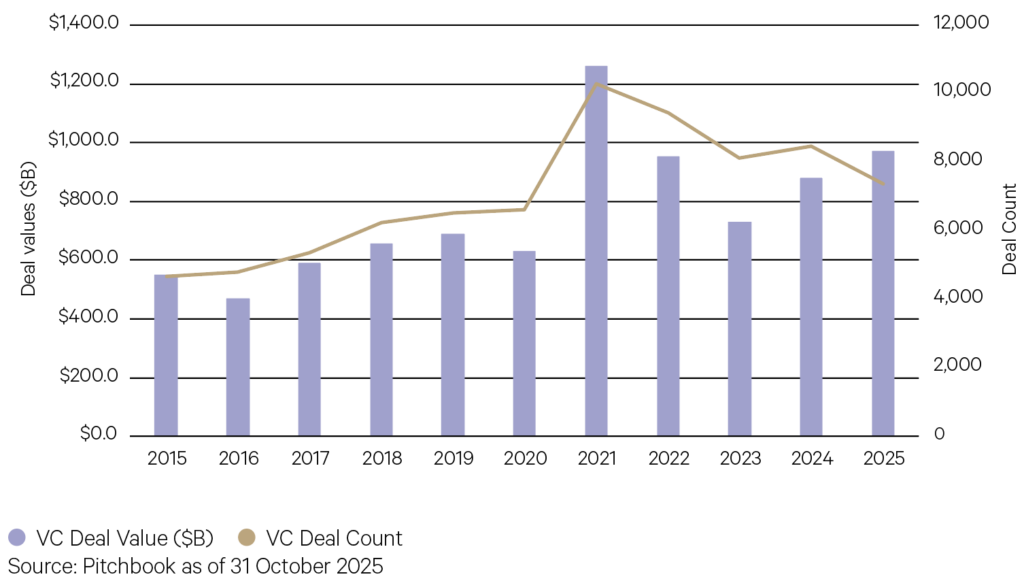

Private equity (PE) dealmaking conditions are steadily improving. The combination of rate cuts, elevated levels of dry powder and clarity around tariff implications has allowed sponsors to deploy increased levels of capital. Pitchbook report that by October 2025, there were 7,370 deals announced or completed within the US PE ecosystem, amounting to a total value of US$969.8 billion. This is the highest deal value recorded since the peak in 2021. The number of deals suggests another robust year ahead, which could exceed 2024’s activity, once Q4 is included.

Chart 10: US private equity deal activity

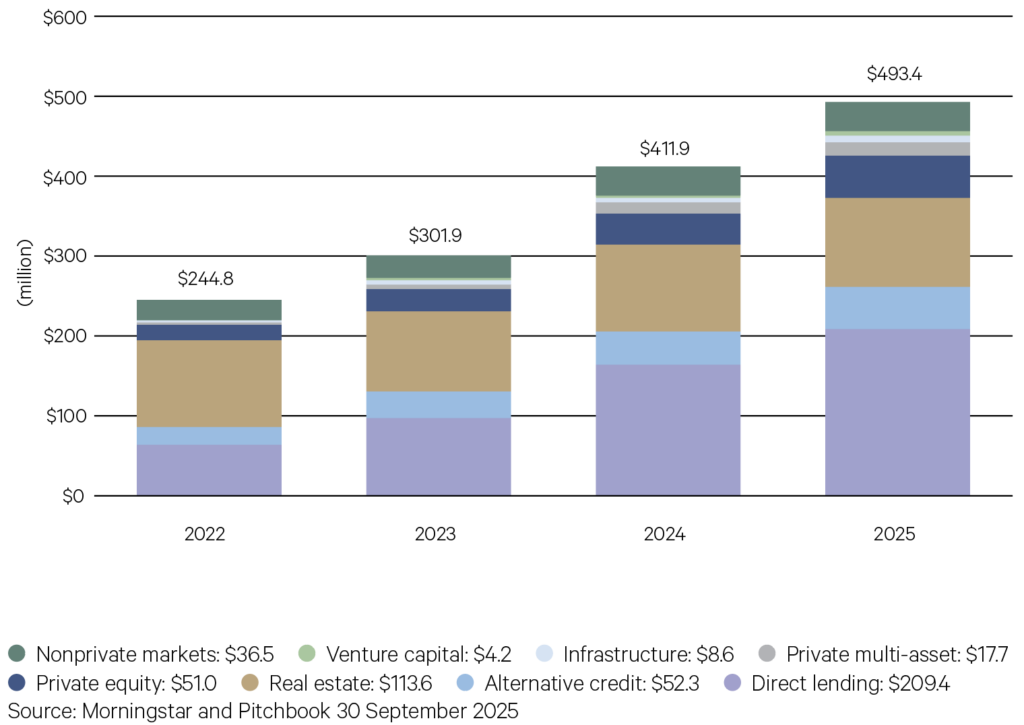

The semiliquid fund market has become one of the most rapidly expanding sectors within private markets. In the twelve months leading up to 30 September 2025, US$51 billion in net cashflow was allocated to evergreen investment funds, raising total assets under management for these funds to US$493 billion—more than twice the US$244 billion recorded in 2022.

While monthly fund flows have fluctuated across various strategies, Direct Lending continues to be the principal contributor, accounting for 42% of evergreen assets under management (AUM). Real Estate follows at 23%, with Alternative Credit and Private Equity representing 11% and 10%, respectively. During the same period, the number of new evergreen funds saw substantial growth, rising from 278 to 505.

Chart 11: Evergreen assets under management ($B) by strategy

Key points

Venture Capital

-

StepStone Private Venture and Growth Fund (SPRING) added +9.4% for the three months ending November 2025. Performance of the fund has continued to be driven by unrealised gains from the mark-up of companies that have recently completed new rounds of financing. One of the main value drivers during the period was AI company xAI. xAI closed an upsized US$20 billion Series E funding round to accelerate AI infrastructure build-out, product development, and research, exceeding its original US$15 billion target. Cursor, an AI coding startup, recently raised US$2.3 billion, lifting its valuation to US$29.3 billion, following a Series C round in June 2025 at US$9.9 billion.

Hedge Funds

-

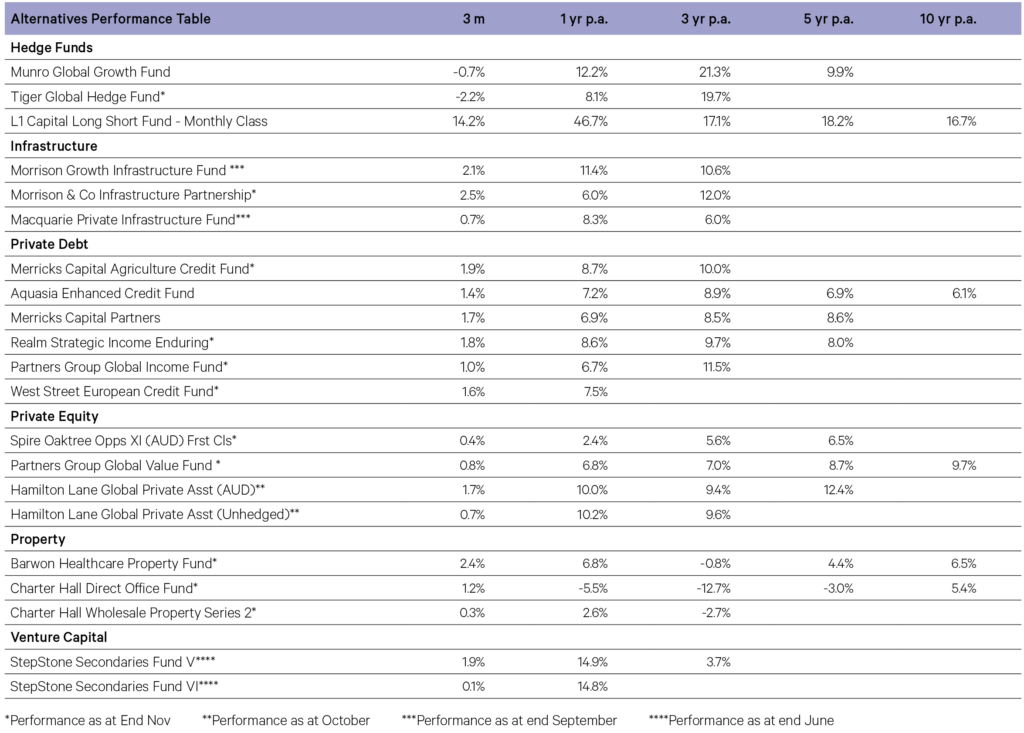

L1 Capital Long Short returned +14.0% (Daily class) for the three months ending December 2025. Broad- based gains were generated across numerous positions. The fund continued to benefit from tailwinds across its gold equities exposures, particularly in the mid-cap space where the fund is positioned. Key contributors across the period included long positions in Mineral Resources, Flight Centre, and Light & Wonder.

-

Equity long short manager Munro Global Growth returned -0.7% for the three months ending December 2025. The fund’s long positions contributed to performance over the quarter, whilst short positions, hedging and currency detracted from performance. Key contributors across the quarter included TSMC, Alphabet and Ciena. Conversely, positions in Oracle, Rheinmetall and Coreweave detracted.

Infrastructure

-

The Macquarie Private Infrastructure fund returned +0.7% over the September quarter. The fund benefitted from positive performance across the majority of underlying investments, in particular strong performance from the fund’s co-investment positions, namely Diamond Infrastructure Solutions and Vocus. Detracting from returns was the Australian airports and unfavourable foreign exchange movements. Notable asset contributors included Aligned Data Centers, Diamond Infrastructure Solutions, the Port of Newcastle, and Vocus.

Private Equity

-

Partners Group Global Value Fund added +0.8% for the three months ending November 2025. During the reporting period, incremental positive revaluations contributed to overall portfolio growth. Key drivers of value included Forterro, which represents the portfolio’s second largest direct investment. Its valuation rose as a result of sustained earnings growth. Additional notable performers within the direct investments segment were United States Infrastructure Corporation (USIC) and FairJourney Biologics, both of which demonstrated strong results over the period.

-

Hamilton Lane Private Assets Fund (Unhedged) returned +3.4% for the three months ending November 2025. Direct equity co-investments drove performance over the period, with OpenAI’s valuation rising to circa $500 billion due to an employee secondary sale.

Private Debt

-

West Street European Private Credit Fund returned 1.6% for the three months ending November 2025. Underlying loan income performed strongly across the period, with the fund invested predominantly in first lien loans that are floating rate and directly originated. The portfolio currently comprises exposure to eleven sub-sectors over ten countries. Several significant deals were completed during the period including positions in Bloom Fresh, Softway Medical and Septeo.

-

Partners Group Global Income Fund returned 1.0% for the three months ending November 2025, driven mainly by interest income, with the IT and Industrial sectors leading performance. The fund participated in new syndicated credit deals with a U.S. software provider and a medicine manufacturer, while also adding direct credit investments in a German construction planner and a U.S. engineering services firm.

-

Merricks Partners added +1.7% for the three months ending November 2025. Portfolio liquidity improved due to successful refinancing and asset sales. The fund received full repayment for a mixed-use construction loan in Adelaide’s CBD and an Auckland hotel development facility. The pipeline remains strong, with notable opportunities in agriculture, build-to-rent, resources, and specialised infrastructure.

-